Posted October 5, 2021 by Nick Maggiulli

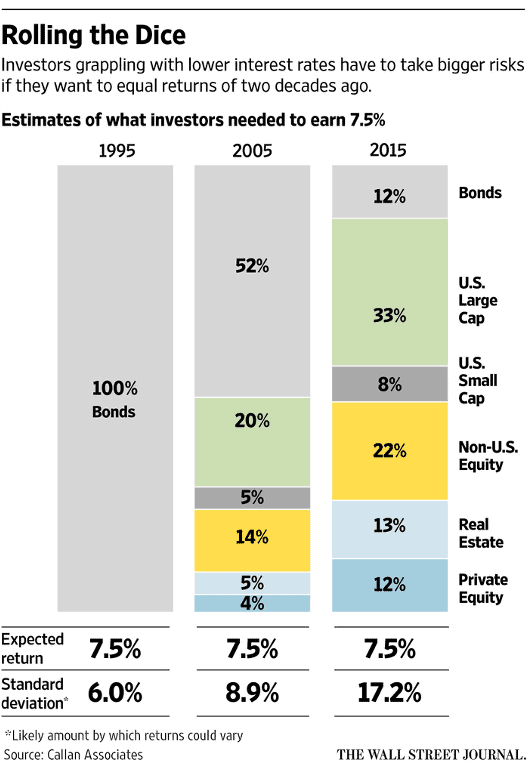

Corey Hoffstein recently brought the following chart to my attention which shows the required allocation to earn a 7.5% expected return in 1995, 2005, and 2015:

As you can see, the days of decent returns for low risk are far behind us. Investors can no longer rely solely on fixed income to generate a portfolio with good returns. Instead they have had to increase their exposure to equities and alternatives to make up the gap. The end result is a portfolio that has nearly 90% less bond exposure than one from two decades prior (controlling for the same level of expected return).

The common takeaway from this shift in allocations is that investors are craving more risk today than in the past. However, I don’t think this theory is accurate. Yes, some investors (mostly younger ones) have been actively seeking more risk in their portfolios, but this doesn’t imply that all investors are seeking more risk as well.

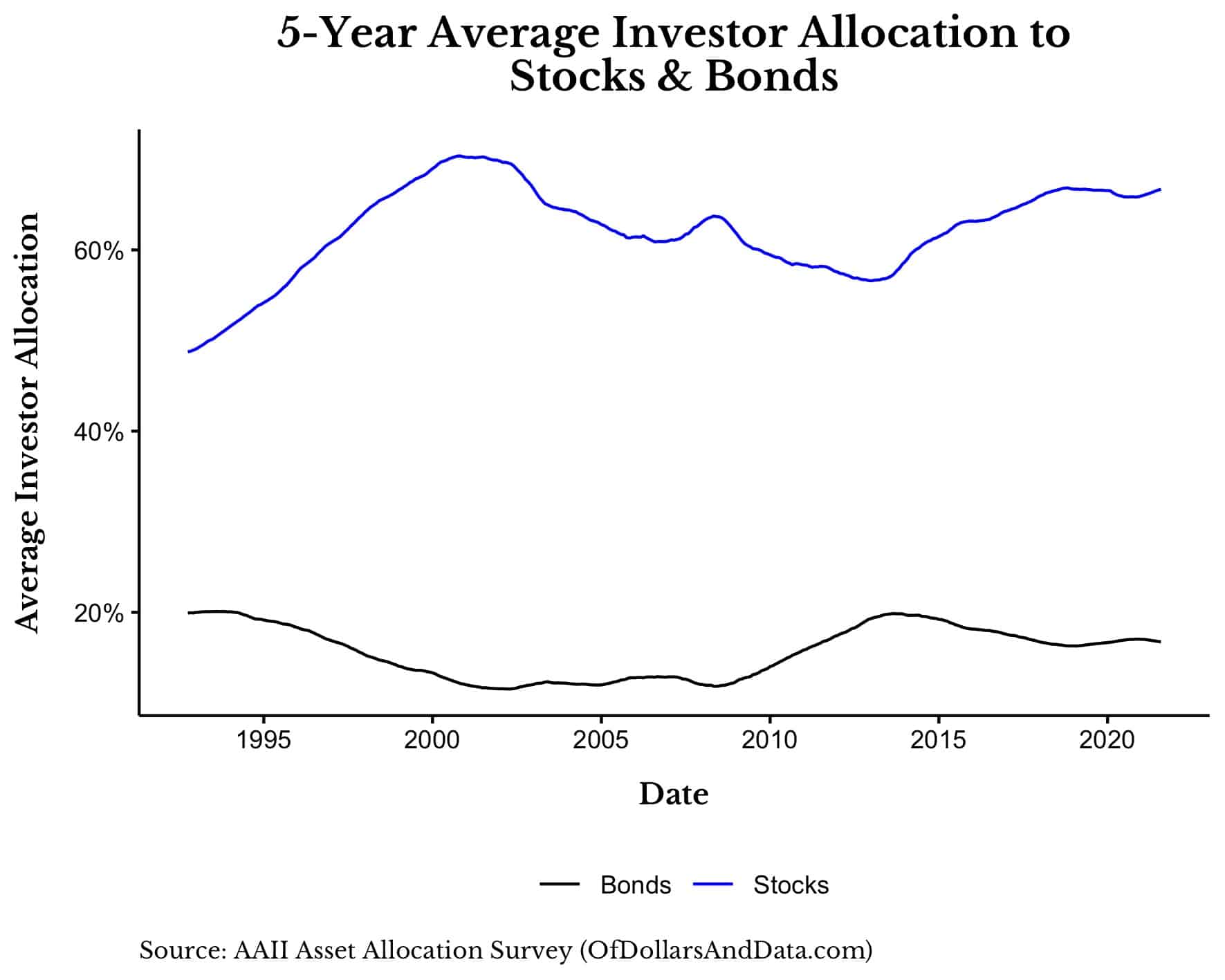

If we look at the average investor allocation to stocks (from the AAII asset allocation survey) we can see that while allocations to stocks are higher than normal, they are still below the record levels reached during the DotCom Bubble. The chart below illustrates this by plotting the 5-year moving average of investor allocations to both stocks and bonds over time:

But this data alone doesn’t tell the full story. Because even if we observed that the average investor allocation to stocks was at record highs, it wouldn’t necessarily imply that investors were craving more risk. In fact, I’d argue that any change in aggregate allocations over the last few decades has little to do with changing risk appetites and everything to do with lower bond yields. Why?

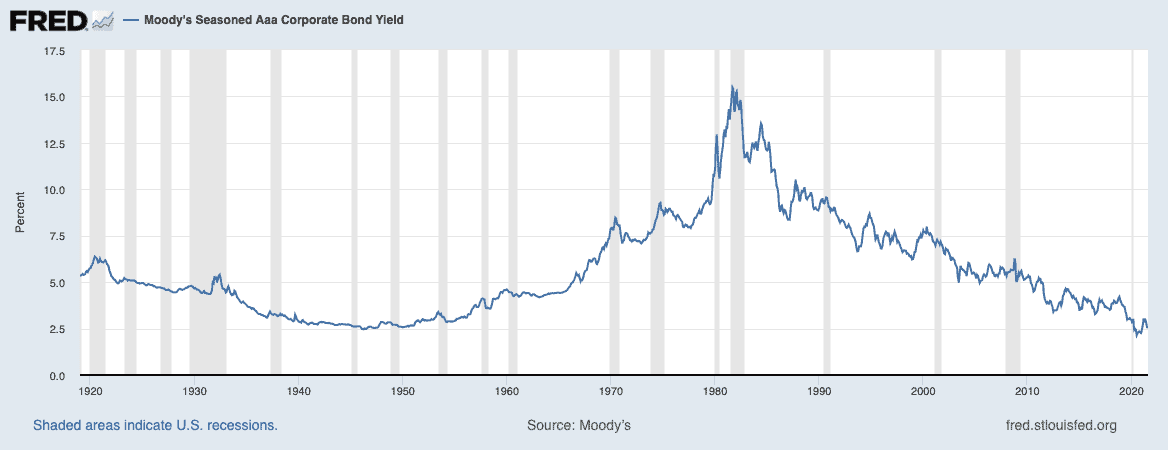

Because investors today don’t have it as easy as the ones from decades prior. Though you may believe otherwise, earning 7.5% a year on your bonds is not normal. As ValueStockGeek wisely pointed out, bond yields from 1980-2000 were truly exceptional in the context of history:

You might see this chart and say, “Well that makes sense cause inflation was generally much higher in the past.”

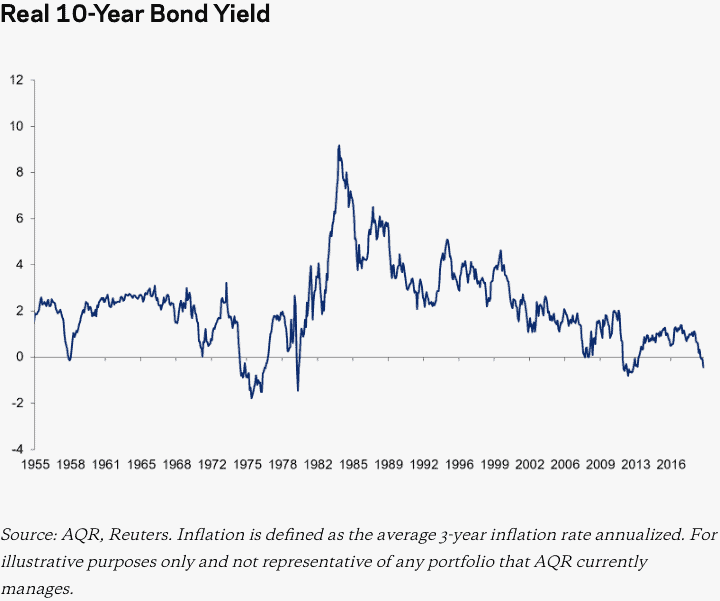

That is true, but even after we adjust for inflation, we can see that real bond yields were abnormally high from 1980-2000:

It is this peculiar period of higher yields that investors became accustomed to and which current investor behavior is being compared to. But this comparison isn’t really fair.

It’s not fair because investors from 1980-2000 could have earned decently high returns while taking on very little risk. Investors today can’t do the same thing. Of course, life isn’t fair, but there really is no other period in American history where U.S. stock and bond returns were so incredible.

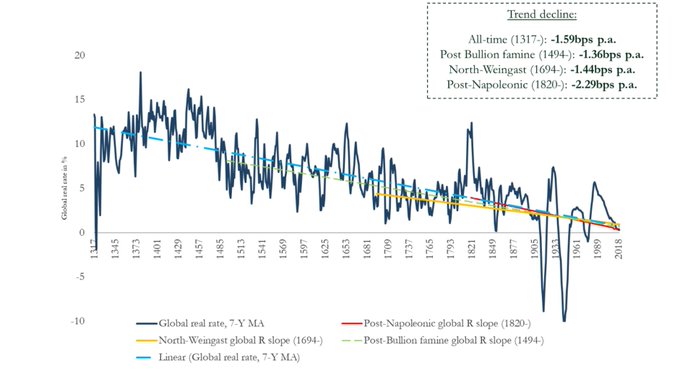

This is why 1980-2000 will likely go down as the most favorable 20-year period in U.S. investment history. However, we haven’t changed our collective narrative to reflect this yet. We are still acting like this period was “normal” though, in retrospect, it clearly wasn’t. Because, if you look over the last six centuries, interest rates across the globe have been on a slow downward trajectory:

And, as you can see, 1980-2000 stands out in stark defiance of this trend. Does this imply that the low rates of today will remain low forever? I have no idea, but I wouldn’t bet on a return to 1980s-like yields anytime soon.

Unfortunately, I’m not sure how much of the investment community feels the same way. Just imagine how many institutions have set their assumed risk and rate of return based on performance data from 1980-2000. Just imagine how many backtests have been run that rely heavily on this atypical time period.

If you were a pension fund in 2005, you had no other choice but to do this. But what about pension funds today? I’m not so sure that relying heavily on this time period to project your future returns makes as much sense. Maybe I am less imaginative, but I can’t see a world where bonds, even 30-year bonds, are paying 7.5% annually.

As a result, what can investors really do? They have no choice but to take on more risk. And no, not because they crave it. People hate risk. People hate uncertainty. But what they like is reward. And if that means that they need to take on more risk to get the reward that they desire, they will probably do so.

So before we judge investors of today (and investors of tomorrow) let’s consider the incentives and the environment in which they are investing. When you do this, a lot more seemingly odd behavior starts to makes sense.

You see someone YOLOing their life savings into a crazy options position? Maybe they think this is their only way to get rich.

You see someone sitting in cash for years? Maybe they can’t stand the idea of losing their hard-earned money.

Though I have my own opinions on all of these issues, I still know that everyone makes choices based on their own personal experiences and beliefs. I am a hyper-rational, data-driven investor. To me, my investment approach seems undeniable. Just look at the evidence, right? How could you believe anything else?

But I also know that this isn’t completely right. People have different experiences that outweigh any sort of data or evidence. They know that historical averages don’t matter when you are on the unlucky side of history.

It’s good to keep this in mind sometimes. Maybe Morgan was right after all:

To each their own. No one is crazy.

Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 262. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data

Source: https://ofdollarsanddata.com/are-we-craving-risk-or-losing-reward loaded 05.10.2021

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}