The gold price suffered some substantial losses during the past year. This is why some market participants declare that Gold is Dead.

1. Historical gold bull market

For millennia, the place of gold and silver has been to serve as stores of value. They protect wealth better than any other investment. Look what happened in the 1970s, when we came off of the gold standard and allowed private ownership of gold. Investors, the rich, and middle class and working class alike piled into the metals. At the beginning of the 1970s, gold was at $35 per ounce. Ten years later, the price stood at $870 per ounce. This is a percentage gain of 2,485 percent. In contrast, during the same time the Dow Jones Industrial Average increased from 809 to 839 points. This represents a total gain of 3.7 percent; not per year, but for the whole decade.

2. Gold Demand

Demand for investment gold is very strong. Last year, the U.S. Mint ceased production of the one-tenth ounce American Gold Eagle because of high demand. This was a sign of record buying, but what is more interesting was a recent World Gold Council report that focuses the demand worldwide. Highlights from the report include continued strong demand in jewelry, particularly in India.

3. The Role of Mining

With the devastating selloff that began in gold in October 2012, the sector is now being avoided like the plague. However, these same miners could support gold and silver prices. Looking to production cost for gold as an indicator, which relies on several factors and varies globally, a ball park average to produce one ounce of gold is about $1,100. The all-in costs of production vary by miner, but with gold around $1300, cost is a major issue.

4. Stocks vs. Gold

The U.S. recovery and global commerce seem to be ramping up, which is an issue for the metals, no doubt. There have been both fundamental and technical reasons for gold’s selloff in the last years. A large driver of the move in gold prices was that major money moved from the metals and into equities. Keep in mind that if this fragile economic rebound falls off track, people will be looking for safe havens. On the other hand, growth isn’t necessarily bad for the metals, as it could lead to some much desired inflation, which always helps metals.

5. Gold is Fungible

In economics, fungibility is the property of a good or a commodity whose individual units are essentially interchangeable and each of whose parts is indistinguishable from another part.

For example, gold is fungible since a specified amount of pure gold is equivalent to that same amount of pure gold, whether in the form of coins, ingots, or in other states. Other fungible commodities include sweet crude oil, company shares, bonds, other precious metals, and currencies.

Fungibility refers only to the equivalence and indistinguishability of each unit of a commodity with other units of the same commodity, and not to the exchange of one commodity for another.

In only a few years, digital currency bitcoin has emerged from the shadows to become something debated by politicians and pondered by economists. Now it is blockchain, the technology that makes bitcoin possible, that is having its moment in the sun: the UK government’s Chief Scientist Sir Mark Walport laid out a possible role for it in delivering public services.

What is the blockchain? In essence it is just a digital ledger – a means to record events that have taken place – but its design provides considerable advantages over other ways of recording transactions. The details of every transaction is stored cryptographically on the blockchain, a stream of linked data available online. The entire blockchain is decentralised, with all those using it creating copies of the blockchain record. This one-version-but-many-copies approach removes the need for a centralised authority, such as a bank or legal body, which also provides protection from a single central point of failure. The blockchain is open and public, and practically impossible to alter a record once the block representing the transaction has been added.

The advantage of decentralisation

This removal of central authorities is seen as a holy grail by some. Using bitcoin in global transactions provides security at low cost, and banks are among those investigating how blockchain or distributed ledgers might replace their monolithic and increasingly dated hardware and software systems. But there has been little implementation of blockchain outside its use in cryptocurrencies like bitcoin.

Some companies have proposed using distributed ledgers as part of their supply chain. Everledger is a firm that records the properties and ownership of diamonds to reduce criminal use or fraud. Provenance is another company doing the same for those wishing to prove the authenticity or fairtrade credentials of their products to customers.

Blockchain provides new technical solutions to situations where trust and authenticity are important. But as with any technology there are positives and negatives – for example, bitcoin’s pseudo-anonymity suits its use by criminals. But in truth almost all crime takes place in the real world with real money: banks we trust pay fines for money laundering, and allegations of unauthorised payments have risen in various sports. Perhaps this most obvious dark side is not the one we should be concerned with.

Debate around blockchain is plentiful, but practical uses are few and far between. O’Reilly, CC BY-NC

Bitcoin’s founders share a distrust of central government’s role in manipulating the value of currencies, and the increasing willingness to use digital technology to interfere in the lives of their citizens, for example through mass surveillance. Nevertheless, governments have legitimate concerns and are democratically accountable.

Bitcoin on the other hand (although not the blockchain underlying it) is governed by a small group of developers and increasingly operated by a concentrated group of bitcoin miners who process the transactions’ computation in exchange for free bitcoin. While the ledger may be distributed, control of it is not. One established bitcoin developer has recently sold his bitcoin, calling it a “failed experiment”. This may be the death of bitcoin, or it may be the start of the revolution devouring its own children.

Put to practical use

Is the blockchain just a solution looking for a problem? Walport’s report attempted to describe how blockchain might become a solution, and how that could be encouraged and managed. Asked to join the report’s advisory panel, I argued that distributed ledgers could be the moment where the internet moves beyond news, entertainment and shopping and starts to do some heavy lifting.

Distributed online ledgers that spread the transactional costs across many points on the network could lead to a revolution in how the economy and society works. Previously, the industrial revolution and the railway and transport revolutions left institutions of society and government essentially intact. Blockchain challenges our existing mindset of how society is organised, and provides the bones of an alternative – for example one with many fewer layers of government and bureaucracy, and less control lying in commercial organisations.

The report recommends among other things that the government should use distributed ledgers to challenge the status quo, and work with new governance structures not against them by enhancing accountability at a local level, while reducing forms of centralised control. This fits a small government agenda espoused by some.

The exploration of distributed ledgers is likely to continue, regardless of any concerns about bitcoin’s success or failure or its potential use by criminals. What’s needed is to move the debate beyond techies, financiers and privacy advocates where it has stalled. The potential of blockchain to change society and how it is run should be a central theme of discussion: distributed ledgers could offer the sort of internet we want, controlled or distributed, centrally administered or community led. This debate should not just be the preserve of a small group of developers or those organisations already dominating the internet.

As essayist William Gibson pointed out: “The future is already here, it’s just unevenly distributed.” We need to find the ways and means to decide how better to distribute the benefits in today’s digitally-enhanced world.

The Biden administration is likely celebrating a better-than-expected jobs report, which showed surging employment and wages. However, for millions of working Americans, being employed doesn’t guarantee a living income.

As scholars interested in the well-being of workers, we believe that the economy runs better when people aren’t forced to choose between paying rent, buying food or getting medicine. Yet too many are compelled to do just that.

Determining just how many workers struggle to make ends meet is a complicated task. A worker’s minimum survival budget can vary considerably based on where the person lives and how many people are in the family.

Take Rochester, New York. It has a cost of living that’s closest to the national average across 509 U.S. metropolitan areas, according to the City Cost of Living Index compiled by the research firm AdvisorSmith.

But in San Francisco, which AdvisorSmith data indicate is the U.S. city with the highest cost of living, affording just the basics costs $47,587, mainly due to significantly higher taxes and rents.

Of course, costs add up quickly for households with more than one person. Two adults in Rochester need over $48,000 a year, while a single parent with one child needs more than $63,000. In San Francisco, a single parent would need to earn $101,000 a year just to scrape by.

So that’s what it takes to survive in today’s America. About $30,000 a year for a single person without dependents in the average city – a little less in some cities, and much, much more for families and anyone who lives in a major city like San Francisco or New York.

But we estimate that at least 27 million U.S. workers don’t earn enough to hit that very low threshold of $30,000, based on the latest occupation wage data from the Bureau of Labor Statistics, a government agency, from May 2020. We believe this is a conservative estimate and that the number of people with jobs who earn less than what’s necessary to afford the necessities of life is likely much higher.

Low-income occupations encompass a wide range of jobs, from bus drivers to cleaners to administrative assistants. However, the majority of those 27 million workers are concentrated in two industries: retail trade and leisure and hospitality. These two industries are among America’s largest employers and pay the lowest average wages.

For example, the median salary for cashiers was $28,850 in early 2020, with 2.5 million of the nation’s 5 million cashiers earning less than that. Or take retail sales. There, 75% of workers – about 1.8 million – were earning less than $27,080 a year.

It’s the same story for leisure and hospitality, the industry that took the hardest hit from the COVID-19 pandemic, hemorrhaging 6 million jobs in April 2020 as much of the U.S. economy shut down. At the time, close to a million waiters and waitresses were earning less than the median income of $23,740.

Of course, millions of those jobs have returned, and wages have been surging this year – though only slightly more than inflation. But that doesn’t change the basic math that roughly 1 in 6 workers is making less than what’s necessary for an adult with no kids to survive.

To us, these figures should cause policymakers to redefine who counts among the “working poor.” A 2021 Bureau of Labor Statistics report estimated that in 2019 about 6.3 million workers earned less than the poverty rate.

But this situation drastically understates the scope of the working poor because the federal poverty line is unrealistically low – only $12,880 for an individual. The official poverty line was created to determine eligibility for Medicaid and other government benefits that support low-income people, not to indicate how much a person needs to actually get by.

Writer James Truslow Adams coined the phrase “The American Dream” in 1931 to describe a society in which he hoped anyone could attain the “fullest stature of which they are innately capable.” That depended on having a good job that paid a living wage.

Unfortunately, for many millions of hard-working Americans, the “better and richer and fuller” life Adams wrote about remains just a dream.

This is the blog post that shows you how to be wealthy enough to retire in ten years.

Here at Mr. Money Mustache, we talk about all sorts of fancy stuff like investment fundamentals, lifestyle changes that save money, entrepreneurial ideas that help you make money, and philosophy that allows you to make these changes a positive thing instead of a sacrifice.

In addition, the Internet presents us with retirement calculators, competing opinions from a million financial advisors and financial doomsayers, unpredictable inflation, and a wide distribution of income and spending patterns between readers.

Because of this torrent of information, people tend to become overwhelmed and say things like,“Yeah, good for you Mr. Money Mustache, but how can I possibly know when I’ll have enough to retire myself, with a completely different lifestyle?”

Well, I have a surprise for you. It turns out that when it boils right down to it, your time to reach retirement depends on only one factor:

Your savings rate, as a percentage of your take-home pay

If you want to break it down just a bit further, your savings rate is determined entirely by these two things:

How much you take home each year

How much you can live on

While the numbers themselves are quite intuitive and easy to figure out, the relationship between these two numbers is a bit surprising.

If you are spending 100% (or more) of your income, you will never be prepared to retire, unless someone else is doing the saving for you (wealthy parents, social security, pension fund, etc.). So your work career will be Infinite.

If you are spending 0% of your income (you live for free somehow), and can maintain this after retirement, you can retire right now. So your working career can be Zero.

In between, there are some very interesting considerations. As soon as you start saving and investing your money, it starts earning money all by itself. Then the earnings on those earnings start earning their own money. It can quickly become a runaway exponential snowball of income.

As soon as this income is enough to pay for your living expenses, while leaving enough of the gains invested each year to keep up with inflation, you are ready to retire.

If you drew this “savings rate” story into a graph, it would not be a straight line, it would be nice curved exponential graph, like this:

Working years vs. Savings Rate (screenshot from networthify.com)

If you save a reasonable percentage of your take-home pay, like 50%, and live on the remaining 50%, you’ll be Ready to Rock (aka “financially independent”) in a reasonable number of years – about 16 according to this chart and a more detailed spreadsheet* I just made for myself to re-create the equation that generated the graph.

So let’s take the graph above and make it even simpler. I’ll make some conservative assumptions for you, and you can just focus on saving the biggest percentage of your take-home pay that you can. The table below will tell you a nice ballpark figure of how many years it will take you to become financially independent.

Assumptions:

You can earn 5% investment returns after inflation during your saving years

You’ll live off of the “4% safe withdrawal rate” after retirement, with some flexibility in your spending during recessions.

You want your ‘Stash to last forever, you’ll only be touching the gains, since this income may be sustaining you for seventy years or so. Just think of this assumption as a nice generous Safety Margin.

Here’s how many years you will have to work for a range of possible savings rates, starting from a net worth of zero:

It’s quite amazing, especially at the less Mustachian end of the spectrum. A middle-class family with a 50k take-home pay who saves 10% of their income ($5k) is actually better than average these days. But unfortunately, “better than average” is still pretty bad, since they are on track for having to work for 51 years.

But simply cutting cable TV and a few lattes would instantly boost their savings to 15%, allowing them to retire 8 years earlier!! Are cable TV and Starbucks worth having two income earners each work an extra eight years for???

it increases the amount of money you have left over to save each month

and it permanently decreases the amount you’ll need every month for the rest of your life

So your lifetime passive income goes up due to having a larger investment nest egg, and it more easily meets your needs, because you’ve developed more skill at living efficiently and thus you need less.

If want to retire within 10 years, the formula is right there in front of you – simply live on 35% of your take-home pay**, which is approximately what I did without even realizing it during my own younger years. The only reason Mustachians will remain a rare breed, is because this article will never appear in USA Today. (Or if it does, people will be too busy complaining about how it can’t be done, rather than figuring out how to do it)

So keep reading, since this blog is all about making financial independence happen!

Never one to let a bandwagon pass by, Greg Medcraft, the Chairman of the Australian Securities and Investments Commission (ASIC), has enthusiastically hopped onto the Blockchain wagon. Mr Medcraft has seen the light and recently proclaimed

“Blockchain is an important technology development that has the potential to change fundamentally the world’s capital markets.”

This is a hugely extravagant claim for what is a basic, if very elegant, piece of computer code. And Mr Medcraft is not alone. None other than Arthur Levitt, the esteemed ex-Chairman of the Securities and Exchange Commission (SEC), has also been converted. And banks, such as Commbank, have eagerly embraced this “next big thing”.

It’s time for someone to critically examine this particular king’s new clothes.

First, what Blockchain is not!

Blockchain is not about so-called cryptocurrencies, such as Bitcoin. Sure, the original Blockchain was the technology underlying Bitcoin but the debate on whether such unregulated currencies have a role in international finance is independent of the Blockchain concept. Blockchain has long since broken the shackles of Bitcoin and is ready to fly on its own.

Nor are the majority of the technologies underlying Blockchain particularly innovative. Concepts such as strong cryptography go back to the work of Diffie and Hellman in the mid 1970s. Hashing, or compressing a piece of information into a short key that is hard to tamper with, was developed for the US National Security Agency (NSA) in the early 2000s and a similar concept has been used in the transmission of financial messages since the 1970s. Even the underlying technical problem of implementing distributed consensus has been solved since the 1980s.

What is unique about Blockchain is how data representing financial transactions is stored. Unlike conventional databases, data is not held in a single place, but as a so-called “distributed ledger” where data is copied and replicated in many computers which, to quote Mr Medcraft, are not “controlled or owned by any single entity”.

Blockchain is the free-market’s Holy Grail. But like that golden chalice, the purported benefits of Blockchain are elusive.

In an op-ed piece Mr Medcraft presented the arguments of the Blockchain spruikers. His assertions are however debatable.

First, the Holy Grail, “Blockchain automates trust and eliminates the need for ‘trusted’ intermediaries”.

Sounds noble but trusted intermediaries, such as stock exchanges and high value payments systems such as SWIFT, are widely used precisely because they are trusted and have been proven to be so for many years. Their track record of technology excellence and stability far exceeds that of the banks and firms vying to replace them. These intermediaries are trusted because they work but they are single, focused and importantly well-regulated entities.

The proponents of Blockchain confuse ownership of a technology with its operations.

Organisations, such as SWIFT and settlement agencies, already operate a “distributed trust” model. They are owned by their members and operated by a separate organisation that is highly transparent as to its policies, rules and operations. The multiple members (owners) do not have to keep a copy of every transaction to trust each other – all they need to do is, individually and collectively, ensure that the independent entity is operating within the agreed rules. It is a form of distributed trust that is efficient and proven to work.

Nor is a distributed trust model completely immune from corruption. For example, the mechanism for assigning credit ratings to securities prior to the GFC was a classical model of distributed trust in that separate and distinct firms (S&P, Moody’s and Fitch) were permitted to assign credit ratings independently. As the official commission into the global financial crisis noted:

“the credit rating agencies abysmally failed in their central mission to provide quality ratings on securities for the benefit of investors.”

The agencies had been corrupted by the incentives provided by external parties, the large investment banks that created the securities, who played one agency off against another to gain advantage.

Another example of distributed trust, which broke down spectacularly, was the recent FX benchmark manipulation scandal. There is no central authority in the global Forex market, yet rampant manipulation of the market went undetected for years. Unfortunately, the Blockchain model does not take into account systemic pressures that affect all of the parties in a particular market.

The second claim made by Blockchain supporters, such as Mr Medcraft, is that of superior efficiency and speed. The speed argument is pure nonsense. The Blockchain mechanism has been set up deliberately to be hard to break. Even its proponents admit this means it is resource intensive and expensive. How can it be faster to interrogate multiple sources of data spread across multiple networks and computers than to retrieve data from one secure and trusted source? Luckily in the real world, the laws of physics and queuing theory still apply.

With an evangelical glint in his eye, Mr Medcraft argued that “when investors now buy and sell securities they generally rely on settlement and registration that takes several days to settle and even longer with cross-border deals. Blockchain can automate this whole process”. Of course he should know better – and he probably does when not intoxicated by the technology.

Sure it takes too long to settle securities today but that is not because settlement notes are being sent by carrier pigeon. It is because, in order to settle real securities (as opposed to artificial Bitcoins) with real money, the exchange of information has to be standardised. Names and codes for securities, counter-parties and currencies all have to be agreed before the exchange will work. This is not a technical problem but one of hard work, analysis and communication that takes time. The fairy dust of Blockchain will never speed up this convoluted process.

One of the many fanciful claims made by spruikers of Blockchain is that the technology will result in massive cost savings. This thinking confuses systems with infrastructure. Blockchain is an infrastructure and has nothing to do with how the data it holds is processed. In order to gain the efficiencies so longed for by Blockchain acolytes, not only do the standards mentioned above have to be developed and agreed but more importantly the computer systems that process the information have to be built. This involves enormous software development costs – far outweighing the costs of the underlying data storage technology.

Blockchain is like the mythical unicorn that appears to give its free-market adherents a vision of a perfect world where economic agents can interact directly with one another freely and without friction. In the real world, building robust financial technology is hard and panaceas, such as Blockchain, thankfully come and go at regular intervals.

Blockchain is an elegant solution to a very specific problem, albeit one that protects the identities of potential drug runners, tax dodgers and money launderers (who incidentally ASIC should be trying to unmask). Its inherent performance limitations means that the technology does not have a meaningful part to play in the trillion dollar, million transactions per day world of real finance.

Now that my blog has gotten some traction among my friends, I have been getting questions like this more often:

“Nick, I just saved up $1,000 and I want to know where I should invest it to get the best return.”

Immediately I think about going into full financial adviser mode to discuss asset allocation, ask about their risk preferences, and understand their goals, but the truth is: their investment returns won’t matter…for now.

With small amounts of money, the total return over the course of a year will be trivial. It would be far better for an individual to focus on saving more money (or growing their income) than worrying about what return they will get in the short run.

For example, let’s say you save up $1,000 and put it into an ETF with an expectation of getting a 10% annual return ($100). You could spend your entire annual return in 1 night going out with friends. Dinner + drinks + transportation and it’s gone.

Now compare this with your future self that has $2 million in a retirement account. A 5% decline in your account value, which is not unreasonable in some years, will result in a $100,000 loss! You couldn’t save that in a year unless you had a very high income or an amazing savings rate.

Therefore, savings have a larger impact on the poor and investments have a larger impact on the rich.

To walk you through my thinking further let’s simulate a 40 year investment life cycle. Let’s assume you make $50,000 a year and save 15% annually (i.e. you save $7,500 each year for 40 years). Additionally, we will assume that you get a 5% annual return on your money with a 9% standard deviation.

This should represent a diverse set of assets (i.e. not as risky as the S&P 500, but not as safe as U.S. bonds). You can imagine the simulation as follows:

In year 1 you save $7,500 and get no investment return on it. In year 2 you get some investment return (random but averages 5%) on the original $7,500 you saved and you save another $7,500. In year 3 you get another random return on the money you had at the end of year 2, and you save another $7,500. This continues onward for 40 years.

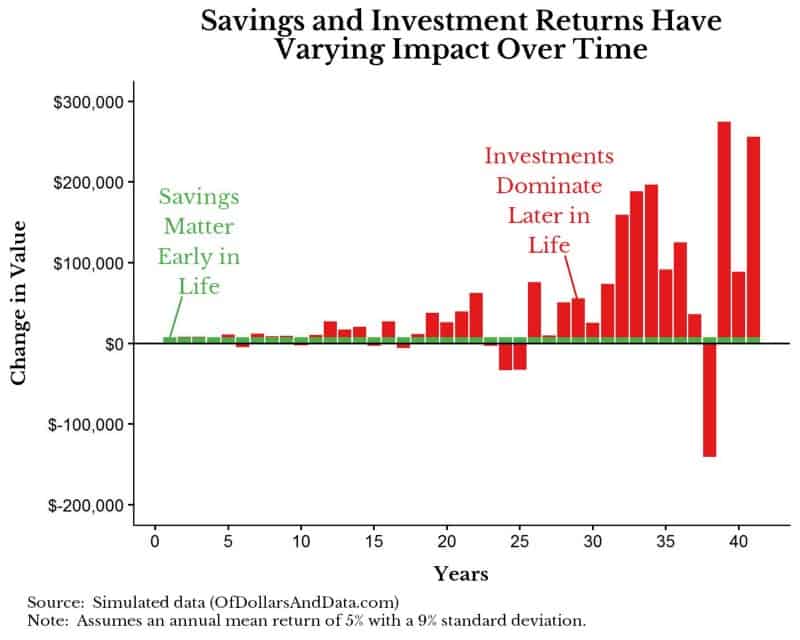

If we were to plot 1 random simulation and show how much was saved in each year (green bar) versus how much was gained/loss from investments in each year (red bar) it could look something like this:

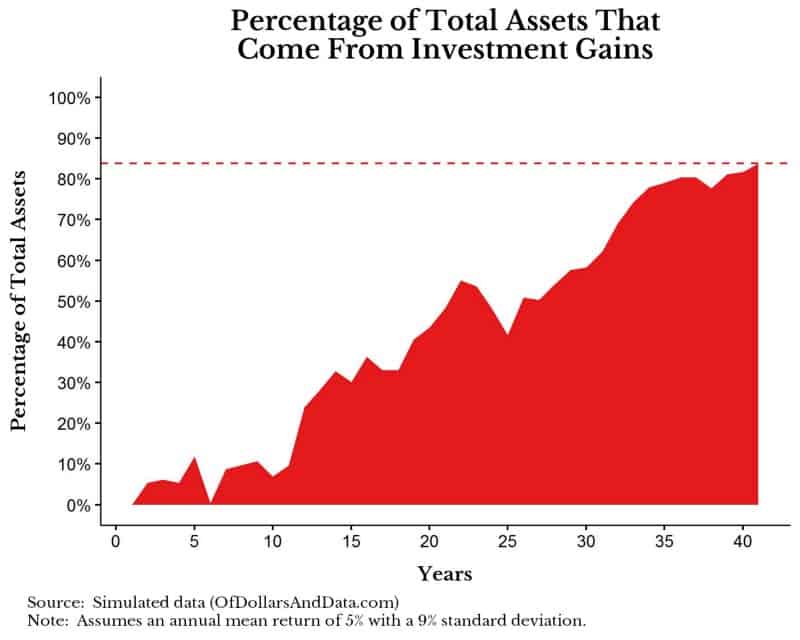

As you can see, the green bars are constant over time since you always save $7,500, but the red bars fluctuate as they represent your random investment returns. Additionally, early in your investment life cycle savings are much larger than investment returns as you would have very little assets. However, as you gain more assets, your gain (or loss) from these assets has a much larger impact on your finances. In particular, by the end of this simulation you would have saved $300,000 ($7,500 * 40 years), but you would have gained ~$1.6 million from investments. This $1.6 million represents 84% of the total assets in year 40 with the $300,000 saved representing the other 16%. If we were to visualize what percentage of your total assets come from investment gains over your life cycle it would look like this (note: the dotted line represents the 84% ending value I discussed above):

As you can see, early on savings are completely building your wealth, however, somewhere near the middle of the life cycle, investment gains become more important.

Regardless of the math and theory behind all of this, the relevant question is:

Should YOU be focusing more on saving or investing?

To answer this, I would ask you to consider the following:

Which is Greater?

Your Total Assets * Your Expected Annual Return

or

Your Expected Annual Savings

If Total Assets * Expected Annual Return > Expected Savings this means your investments are earning you more than you are saving, so you should focus on your investments. However, if you can feasible save more than your assets can earn you in a year, focus on saving.

Practically speaking, if you have $100,000 in assets with an expected return of 5% each year, this means you would expect your investments to earn $5,000 annually (or $100,000 * 0.05). Additionally, if you expect to save $7,500 a year, which is greater than the expected $5,000 from investments, you should focus on saving more money.

Note that this is a spectrum, so it does not imply that you can ignore your investments or your savings rate! However, this should illustrate how important each one is to your financial picture.

Savings is For the Rich Too

Despite the dichotomy I have tried to create between saving and investment income in this post, the truth is that saving is far more important. The ability to save money is highly correlated with financial success because it allows you to live on less and have more disposable income for investing.

You should also consider reading arguably the best personal finance blog post on the internet: Mr. Money Mustache’s Shocking Simple Math Behind Early Retirement. This one post summarizes the entire philosophy behind his blog and it completely revolutionized how I think about saving money.

Regardless of how much you are saving now, you can always change this in the future, so stay positive and get to saving. Thank you for reading!

Digital cryptocurrencies like Bitcoin may have failed to unseat their more traditional rivals, but the technology that underpins Bitcoin may yet bring about a revolution in finance and other industries. This technology is called the “[blockchain](https://en.wikipedia.org/wiki/Block_chain_(database)”.

The blockchain acts as a public database or ledger, and is the technology that stores the details of every exchange of bitcoins. What makes it particularly clever is that it is designed to stop the same bitcoin being spent twice, without the need for a third party (like a bank).

The promise of the blockchain

Even from the early days of Bitcoin, it was believed that the blockchain could be used for much more than recording Bitcoin transactions. What the blockchain does is record a set of details that include a time, a cryptographic signature linking back to the sender and some data that can represent almost anything. In the case of Bitcoin, it is the number of bitcoins being sent but it could be a digital cryptographic signature, called a “hash”, of any electronic document.

One of the earliest demonstrations of the potential of using the blockchain in this way was “proof of existence”, a website that allows a user to upload any document and have its signature recorded for ever on the Bitcoin blockchain.

What this does is prove that the person who uploaded the document had that specific document in their possession at a specific time. It can also be used to prove that the document had not been altered in any way from that time.

The blockchain realised

Proof of existence was intended as a demonstration of the potential of the blockchain technology. Startup Stampery has turned this service into a business that allows other companies to “digitally stamp” any of their electronic documents or emails in order to prove ownership and integrity.

This week the US Securities and Exchange Commission (SEC) approved the use of the blockchain as a share ownership register for online retailer Overstock.com.

Overstock plans to use alternative trading system technology provided by T0.com, to enable people to buy and sell these shares. The attraction of this system is that it provides instant settlement as opposed to the traditional three day settlement for traditional company stock.

T0’s implementation of its share register uses an extension of the Bitcoin blockchain called “Colored Coin” that was originally seen as adding a “smart contract” functionality to Bitcoin. One scenario where this could be used would be where someone was sending Bitcoins for the purchase of a house for example, and the currency would only be released if the contracts for the sale went through.

The risks and challenges of the blockchain

Whilst Overstock’s SEC filing does highlight the advantages of having a public ledger that is theoretically secure, it also stresses the risks. One of those is the fact that Overstock has chosen to make the information stored on the the blockchain ledger accessible by anyone, so investors may have concerns about the privacy of their holdings.

However, the main risk is one that is a general issue with all blockchain applications, including Bitcoin. This is the fact it is still not known exactly how secure the system is and whether it has any flaws that could be exploited by hackers.

One potential issue around the use of the blockchain is the fact that there are now a large number of different implementations, all based on different technological approaches. IBM, JP Morgan, Intel and a group of other companies have just launced the “Open Ledger Project”. Open Ledger does not use the Bitcoin blockchain but implements a different scheme that is more suited to companies wanting to restrict access to the blockchain ledger.

There is no doubt that the ideas behind the blockchain are clever ones and were critical to enabling a digital currency like Bitcoin to operate with many of the same properties as cash does in the physical world. When the technology is used for other applications, though, it is not absolutely clear that it actually does anything that can’t be achieved with other, more conventional technology.

The social issues are harder than the technological ones

It is not the technology that is stopping shares from being settled instantly. It is regulators and the issues they are dealing with in terms of this type of settlement are social and legal ones, not technical.

In the hype that surrounds companies that are working on blockchain products, the real challenges facing the actual use of these products are often glossed over, with the main objective being to get rid of third parties but without necessarily replacing all of the positive things those third parties may actually have been doing.

It is inevitable that blockchain technology will become a mainstream technology. The level of interest being shown in this technology demonstrates its potential for enabling the development of applications that will bring new approaches to old business problems. It is the social, legal and financial challenges that these changes will surface that may prove a much harder problem to solve.

Is Gold Dead? by Joseph Brown Gold’s performance has been less than stellar over the last year. This has caused many to take their losses and look elsewhere to invest their money. Because of the extreme bearish sentiment surround gold lately, it’s important to keep looking at the numbers to determine whether or not gold […]

Source: https://schiffgold.com/peters-podcast/peter-schiff-central-banks-have-created-the-mother-of-all-bubbles/ BY SCHIFFGOLD The Federal Reserve and other central banks around the world have pumped trillions of dollars into the global economy and depressed interest rates to artificially low levels to blow up the mother of all bubbles. In his podcast, Peter Schiff explained how the recent acquisition of Afterpay by Square reveals the extent […]

Retirement. The Nobel Laureate William Sharpe called it the “nastiest, hardest problem in finance.” And it is. Between deciding how much to save and spend throughout your life, you also have to make guesses about the future.

What will inflation be? How long will I live? What kind of returns will assets provide? And the list goes on.

Despite this complicated process, the financial aspect of retirement planning boils down to three things:

How Much You Save Before Retirement. This is a function of the number of years you decide to work, your income, and your savings.

Asset Allocation. This is a function of how you invest your savings and how much risk you want to take.

How Much You Spend in Retirement. This is a function of your total savings and your future spending, inflation, asset returns, and lifespan.

This might seem daunting, but, if you make just a few simplifying assumptions, you can eliminate most of these choices. For example, you have no control over future asset returns and inflation and limited control over your lifespan. So, if we assume those are out of our hands, then retirement comes down to your savings rate and asset allocation. That’s it.

But, even these two choices are very different. Your savings rate is constantly in flux, being impacted by financial decisions small and large throughout your life.

You can stay in or you can eat out. You can take transit or you take Uber. You can buy or you can rent. All of these choices, and more, will have varying degrees of impact on your retirement success.

However, your asset allocation (i.e. how much risk you take) is one decision that you make that will have the greatest impact on your finances for the least amount of effort.

Because all of those thousands of other financial decisions that you will make across decades will require far more time and energy than deciding what you invest in. Because once you are invested, the compounding should take care of itself.

This is why asset allocation is by far the easiest retirement choice you can make. Let me illustrate this with a simulation. To start, we need to assume the following:

Before Retirement

You work and save money for 40 years (i.e. assume you start saving at 25 and retire at 65).

Your annual income starts at $50,000 and grows with inflation.

You save X% (this will vary) of your income each month and re-invest it in some portfolio.

Your saved money goes into a portfolio consisting of some mix of U.S. Stocks and Bonds (this will vary).

In Retirement

You live for 25 years (i.e. assume you retire at 65 and die at 90).

Your spending is identical to what is was when you were working (constant in real dollars). So if you saved 10% of your income each year, this implies you lived off of 90% of your income. In retirement you would be spending 90% of your final income (indexed to inflation) each year.

Your nest egg is invested in whichever portfolio you invested in before retirement (this will vary).

If we were to start this simulation in 1926 and go through every possible 65 year period (i.e. 40 working years + 25 retirement years) and finish in 2018, we would have 28 different retirement simulations we could test (thanks to Michael Batnick for the idea).

Of course this is simplified, but it will illustrate my main point. First I will walk through an example of one simulation and then present the full results.

Example Walkthrough

Let’s say you started working in 1926 with an income of $50,000 (yes this was a lot of money then, but the starting income is arbitrary for this). By the time you retired in 1966, your real income was identical, but your nominal income would have grown to $89,000 due to inflation.

If you saved 10% a year over this time period, you would have saved a total of ~$240,000. If you had invested in:

100% Bonds you would have $382,000 when you started retirement.

60/40 Stock/Bond you would have $1.6 million when you started retirement.

100% Stocks you would have $3.7 million when you started retirement.

In your first year of retirement you would have spent $80,000. This represents 90% of your final income (i.e. 100% – 10% savings rate). With such spending, your portfolio would run out of money in 5 years with 100% Bonds, in less than 20 years with 60/40 Stock/Bond, and would not run out in 25 years with 100% Stocks.

This example shows the power of asset allocation to have a dramatic impact your chance of financial success in retirement. That one decision made near the beginning of your working life (and stuck to throughout) can have an impact equal to your savings rate with far less effort.

Full Results

Now, let’s do the same simulation for all 28 periods we have available. Below is a chart of the portfolio values at the start of retirement (for the 100% Bond, 60/40 Stock Bond, and 100% Stock portfolios) based on the year you started retirement for each simulation. Note that the leftmost points (i.e. retire in 1966) were covered in the example above:

As you can see, the asset allocation decision can make a large impact on your final portfolio value. The spread you see between the 100% Stock portfolio and the 100% Bond portfolio shrinks over time because of how those assets performed over the years.

The main takeaway is that stocks completely dominated bonds for most of the twentieth century. For example, bonds did quite poorly from the 1940s-1970s, but started to do much better in the 1980s-1990s:

These disparities in returns will also show up in the simulations when looking at the number of years until you run out of money. The plot below has color/shape for each portfolio and the number of years until that portfolio ran out of money based on the retirement start year. If a particular point is at the top of the chart (i.e. 25 years) that means that simulation did not run out of money.

For example, as I highlighted in the “Example Walkthrough” above, if you started retirement in 1966, your portfolio would run out of money in 5 years with 100% Bonds, in less than 20 years with 60/40 Stock/Bond, and would not run out in 25 years with 100% Stocks. This plot is just expanded to show if you retired in 1967, 1968, and so on:

But, we can take this a step further by varying the savings rate over time (from 5% to 20%) and watching how that affects the number of years until the portfolios run out of money:

As you can see, your savings rate will make a big difference in whether you run out of money in retirement, but so does your asset allocation. With a savings rate as low as 13%, the 60/40 portfolio never runs out of money in any of the simulations. Compare this to the 100% Bond portfolio which still runs out of money in some cases with a 20% savings rate!

However, moving your savings rate upward is no easy task. It requires decreased spending or increased income, both things that are not necessarily easy to do. On the flip side, it is also not necessarily easy to bear more risk in your portfolio (i.e. going from 100% Bonds to a 60/40 portfolio), but as Corey Hoffstein so famously repeats:

Risk cannot be destroyed, only transformed.

So, by taking less risk now (i.e. 100% Bonds) you actually take more risk later (i.e. running out of money in retirement). So the question is: Do you want to work your butt off to increase your savings rate, or would you rather take the easy way out and take a little more short-term risk?

The Hardest Choice in Retirement

Despite all of the discussion of the financial choices you need to make for retirement, it’s actually the non-financial aspects of retirement that are the hardest to figure out.

As I have written before, the most important decision you can make in your retirement is how you are going to spend your time, not your money. Many people end up retired and lose their sense of purpose despite having sufficient financial resources.

Though this may seem unrelated, this is also my biggest problem with universal basic income (including sovereign wealth funds). These systems provide money, but they don’t provide any sense of fulfillment for those that receive that money. With the recent increase in deaths of despair in the U.S., figuring out how to give people income and meaning may be one of the most important problems we can try to solve in society.

Though I don’t have an easy answer for how to help you find meaning in your life, I recommend that you create something and give back to a community. Also consider reading How to Retire Happy, Wild, and Free, a retirement book that can help anyone tackle the issue of meaning before and during retirement. It’s the best retirement book I have ever read and it has zero discussion of money.

Lastly, for all of those that have been following along, you may have noticed that my most recent posts have far more data and far fewer stories. I am going back to my roots and hope you stay along for the ride. As always, thank you for reading!

{kind=link}

{kind=link}