Back in July I found myself up in the far north of Maine looking out at the Atlantic Ocean. I was a guest of one A. Noonan Moose.

Mr. Moose owns the beach house with this lovely view where we were guests and it is a far more impressive place than my little shack. The first time I met him was when I showed up on his doorstep to spend a few days.

See, he actually didn’t invite me. Mr. 1500 Days did.

“I’ll be up there with my family,” he said. “Come join us.”

“Thanks,” I said. “But perhaps we should ask Mr. Moose?”

“No worries. I did. He says it’s fine.”

“Mmmm. All the same, I’d like to hear it from Mr. Moose himself.”

This was not the first time Mr. 1500 had invited me to this Maine retreat he doesn’t actually own. But it was the first time I could get confirmation that Mr. Moose was onboard with the idea.

Mr. 1500 does this. He has done it to us when we were staying at my in-laws’ beach house. This is how I met Physician on FIRE, a great blogger and who is now a great friend. So, I’m not complaining.

Just pointing out, if you have a beach house or access to one and you know Mr. 1500 he’s gonna visit and invite some friends. Fortunately, you’ll like his friends.

Anyway, when I arrived Mr. Moose and Mr. 1500 were boiling the water for the unsuspecting lobsters that were our delicious dinner that evening. I felt welcome immediately and Mr. Moose and his lovely wife and I hit it off just fine. Seeing Mr. 1500 wasn’t too bad either.

A couple of days in, Mr. Moose started telling me about WARM, his retirement strategy. As he went on about how he holds almost no stocks (Stocks are essential for a portfolio’s long-term survival!) and mostly cash (I hate holding cash!) alarm bells were clanging in my head.

But I kept quiet and listened respectfully. I was, after all, a guest and enjoying his splendid hospitality. But inside my objections were raging and my eyes were rolling.

As I left, he handed me a few pages. “This,” he said “is an article I wrote about WARM in case you might be interested.” I politely took it with thanks and, sure I’d never glance at it, tossed it on my desk when I got home.

But a few days later I noticed it sitting there and I did pick it up. I started reading. The prose was clear and the ideas well presented. All those alarm bells? He had thought about and addressed them.

To be clear, this is not an approach I’d use or recommend to the readers of this blog. At least not most of them.

Since I began this blog in 2011, with rare minor corrections, the stock market has done nothing but go up. Anyone who has followed my advice has done nothing but make money.

But anyone who has actually read my advice knows I am always warning that the stock market is a very volatile beast and it provides a gut wrenching ride. “There is a Major market crash coming!!!” screams the title of the first post in my Stock Series. Over and over I say: Expect the market to periodically drop. Sometimes hard. This is normal. A part of the process.

And, for the last eight years, the market does nothing but go up. Where’s the big drop you need to prove your point when you need it?

Someday that will change. Those of you who lived thru 2008-9 with major money invested know what it is like and you know if you can grit your teeth, ignore it, not panic and ride it out. Or not. But unless you’ve lived thru it, it is impossible to describe just how ugly it can be.

If those last few lines have you nervous, well good. It is easy, probably way too easy, to sit here basking in warm glow of relentless year-over-year market gains and think: Sure. No problem. I can weather the storms if they come.

(No, no, no, no!!!! Not “if” — When! When, dammit, when I tell you!! When!!)

Unless you are absolutely certain you can watch your net worth get cut in half with no end in sight and shrug your shoulders, ignore the panic and go about your day… Now is the time to reconsider.

Know thyself. Decide now that selling during a market plunge is simply not an option. If you can’t, if you are thinking dealing with such a trauma is more than you ever want to face (and who can blame you?), you’ll need another plan.

Because my advice here only works for the long-term if you stay the course. Panic and sell when the storm comes and you would have been better off in cash. Which leads us nicely to Mr. Moose and his WARM approach…

How to Sleep Soundly while Stock Markets Crash

by A. Noonan Moose

Retirement advisors must hate me. They call regularly, but they’re never hired.

Why not?

Ever since I retired in 2008, I’ve been executing my own plan for the future. I don’t need to hire experts because my approach is so simple, so boring, and so reliable that I can easily handle everything myself.

Best of all, my retirement plan is powered by something that’s largely within my control (household spending) rather than by something that’s beyond my control entirely (stock market returns).

If stocks were powering my retirement, I wouldn’t always sleep so well. But through any market turmoil I snooze away just fine.

Here’s why.

To implement my simple, boring, and reliable retirement plan you need to know only three numbers:

your age

your annual household spending

your net worth

Like I said, it’s a simple plan. Here’s an example:

John Dough is 50 years old and so is his wife Jane;

their “burn rate” annual household spending averages $40,000 per year; and

their net worth is $2 million.

Are the Doughs in solid enough shape to retire at age 50?

Yes, they are.

How do I know?

Because their net worth is enough to cover 100 percent of their spending needs for the next 50 years. The math is so easy a third grader could do it: $2,000,000 net worth / $40,000 burn rate = 50 years.

But how can I know whether 50 years worth of spending will be enough?

Thus, as long as the Doughs’ adapt reasonably to inflation (more on this below) the odds are very high that their money will outlast their lives.

THE WASTING ASSET RETIREMENT MODEL (WARM)

My simple approach to retirement treats a nest egg like a “wasting asset.”

A wasting asset is an asset that has a limited lifespan and thus loses value over time. Eventually, the asset’s worth drops to zero (or slightly above zero if the item has scrap value).

Your refrigerator is an example of a wasting asset. You buy it new for $1,000 or so. After that its resell value declines steadily until it stops working whereupon you haul it to the junkyard.

Our nest eggs can be treated like wasting assets because we ourselves are wasting assets. Inevitably, human bodies decline just like refrigerators do (our remains might avoid the junkyard, but not the bone yard). When we depart, our wealth is worth nothing to us because we can’t possibly access the money and of course we’re too dead to care.

The WARM method for retirement planning can be presented as a simple chart (see below). If you know your annual burn rate and the years you’ll be retired, the chart shows how big a nest egg you need. If you know your annual burn rate and net worth, the chart shows how long your money will last if you treat it like a wasting asset.

Wasting Asset Retirement Models

Annual Burn Rates of $20k-$100k and Retirements of 35-65 Years

35

40

45

50

55

60

65

$20,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

$1,300,000

$25,000

$875,000

$1,000,000

$1,125,000

$1,250,000

$1,375,000

$1,500,000

$1,625,000

$30,000

$1,050,000

$1,200,000

$1,350,000

$1,500,000

$1,650,000

$1,800,000

$1,950,000

$35,000

$1,225,000

$1,400,000

$1,575,000

$1,750,000

$1,925,000

$2,100,000

$2,275,000

$40,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

$2,200,000

$2,400,000

$2,600,000

$45,000

$1,575,000

$1,800,000

$2,025,000

$2,250,000

$2,475,000

$2,700,000

$2,925,000

$50,000

$1,750,000

$2,000,000

$2,250,000

$2,500,000

$2,750,000

$3,000,000

$3,250,000

$55,000

$1,925,000

$2,200,000

$2,475,000

$2,750,000

$3,025,000

$3,300,000

$3,575,000

$60,000

$2,100,000

$2,400,000

$2,700,000

$3,000,000

$3,300,000

$3,600,000

$3,900,000

$65,000

$2,275,000

$2,600,000

$2,925,000

$3,250,000

$3,575,000

$3,900,000

$4,225,000

$70,000

$2,450,000

$2,800,000

$3,150,000

$3,500,000

$3,850,000

$4,200,000

$4,550,000

$75,000

$2,625,000

$3,000,000

$3,375,000

$3,750,000

$4,125,000

$4,500,000

$4,875,000

$80,000

$2,800,000

$3,200,000

$3,600,000

$4,000,000

$4,400,000

$4,800,000

$5,200,000

$85,000

$2,975,000

$3,400,000

$3,825,000

$4,250,000

$4,675,000

$5,100,000

$5,525,000

$90,000

$3,150,000

$3,600,000

$4,050,000

$4,500,000

$4,950,000

$5,400,000

$5,850,000

$95,000

$3,325,000

$3,800,000

$4,275,000

$4,750,000

$5,225,000

$5,700,000

$6,175,000

$100,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

$5,500,000

$6,000,000

$6,500,000

You’ll notice this chart says nothing about investment returns. That’s because WARM distinguishes between: (1) your accumulative years, when you buy stocks to grow wealth; and (2) your post-accumulative years, when you avoid stocks to preserve wealth. Once your nest egg grows large enough to fund your desired term of retirement (see chart above), you transition your portfolio to safer assets.

In our household, for example, our nest egg has grown large enough to last us both past age 100 as long as we adapt reasonably to inflation (more on this below). Accordingly, we can afford to maintain a conservative asset allocation: 6.51 percent in stocks, 27.94 percent in real estate, and 65.55 percent in money markets/bonds.

Most professional advisors would deride our asset allocation as unduly timid, but our response to them is this: if we already have enough assets to both reach age 100, why should we expose ourselves to unnecessary risk? We’re frugal, not materialistic. We harbor no ambitions to suddenly become big spenders. Any gains we achieved from stocks would be entirely superfluous to our need and any big losses might send us scurrying back to the workforce. We therefore follow a retirement plan that avoids market turbulence, which is something we can’t control, and leverages our ability to manage household spending, which is something we do very well.

In other words, with this conservative approach to retirement, we sleep both safe and WARM.

WARM FAQS

What happens to you if inflation rears its ugly head?

If inflation grows, it won’t happen overnight. We’ll have enough advance warning to cut our discretionary spending. Our current lifestyle reflects many luxuries. Relatively painless cuts of 25 percent or more are well within reach. If absolutely necessary, we can also invest in greater risks that offer the prospect of larger returns.

But then again, if inflation grows we might just stick with our existing plan. Such a response is possible because WARM includes two baked-in hedges against rising prices.

First, WARM†ignores the money we’ll receive from social security. Retired workers currently average $16,220 in social security benefits per year and our household contains two retired workers. By law, social security benefits increase each year in lockstep with the Consumer Price Index. Sure, a glut of baby boomers is straining the system’s finances and this may reduce future benefits. But reduced benefits are not the same as zero benefits. Social Security will continue to exist in some form or other. And its steady income stream will offset inflation.

Second, WARM assumes that our annual expenses will remain level until we die. In reality, our spending will drop off long before we do. The Employee Benefit Research Institute reports:

“Household expenses steadily decline with age. With the age 65 expenditure as a benchmark, household expenditure falls by 19 percent by age 75, 34 percent by age 85, and 52 percent by age 95.”

Expenditure Patterns of Older Americans, 2001-2009, S. Banerjee (EBRI Issue Brief, 02/2012). Why the big declines? Simple answer: although oldsters spend more on medical care as they age, they also spend much less on travel and entertainment. Accordingly, inflation in later life is offset by lower living costs.

What about your longevity risk?

We believe we’ve adequately accounted for longevity risk by accumulating enough assets to get us both past age 100. In any event, if future medical advances dramatically extend current lifespans we can always reduce our burn rate and, if absolutely necessary, increase our exposure to stocks.

What about leaving a legacy for the next generation?

We have no children and we don’t believe in dynastic transfers of wealth to our nearest relatives. Our attitudes about inheritance are informed by our experience. People who expect big windfalls tend to coast, thus denying themselves the fulfillment that comes from productive pursuits. So instead of crushing the work ethics of our nieces and nephews, our estate plan funds several deserving charities that we’ve supported for decades. Our legacy will help many people instead of just a few lucky heirs.

By the way, please feel free to disagree with our estate plan. We know it’s not for everyone. But if you want to enrich your relatives, you need to gauge how much portfolio risk to undertake in order to reach that goal. Fair warning: rides in the stock market sometimes get rocky.

What are the tax implications of WARM?

Current federal policies, especially in the setting of interest rates, favor debtors over savers. As a result, our cash holdings haven’t produced much income each year, we end up in the 10 or 15 percent federal tax bracket. But our low brackets have produced some helpful side benefits. For instance, Obamacare premium tax credits regularly subsidize our health insurance costs. Moreover, the tax code exempts us from paying taxes on capital gains and qualified dividends. For a full list of the many tax benefits we’ve enjoyed in early retirement, click here.

How does WARM compare to the Four Percent Rule?

The Four Percent Rule is a well-known formula for funding retirements that last as long as 30 years, which is the outer reach of traditional financial plans (quit at 65, die at 95). Under this rule, new retirees withdraw 4 percent of their nest egg to fund first year expenses and then in each successive year they adjust that dollar amount upwards for inflation. See New Math for Retirees and the 4% Withdrawal Rate, T. Bernard (New York Times, 05/18/2015).

Importantly for risk avoiders, the Four Percent Rule assumes that the retiree’s portfolio is split evenly between stocks and bonds. In contrast, a WARM retiree’s portfolio can afford to have a much smaller position in stocks (in the case of our household, less than seven percent).

WARM retirees have to pay for their ability to sleep soundly through market gyrations there’s no such thing as a free lunch. The best way to explore the necessary trade-offs is to review this chart.

4% Withdrawal Rule vs. WARM for a 30 Year Retirement

Burn Rate

4% Rule Nest Egg

WARM Nest Egg

Percent increase

$20,000

$500,000

$600,000

20.00%

$25,000

$625,000

$750,000

20.00%

$30,000

$750,000

$900,000

20.00%

$35,000

$875,000

$1,050,000

20.00%

$40,000

$1,000,000

$1,200,000

20.00%

$45,000

$1,125,000

$1,350,000

20.00%

$50,000

$1,250,000

$1,500,000

20.00%

$55,000

$1,375,000

$1,650,000

20.00%

$60,000

$1,500,000

$1,800,000

20.00%

$65,000

$1,625,000

$1,950,000

20.00%

$70,000

$1,750,000

$2,100,000

20.00%

$75,000

$1,875,000

$2,250,000

20.00%

$80,000

$2,000,000

$2,400,000

20.00%

$85,000

$2,125,000

$2,550,000

20.00%

$90,000

$2,250,000

$2,700,000

20.00%

$95,000

$2,375,000

$2,850,000

20.00%

$100,000

$2,500,000

$3,000,000

20.00%

As the chart reveals, retirees who follow the Four Percent Rule can convert to a WARM retirement in three different ways.

First, they can switch to WARM by amassing a 20 percent larger nest egg. This means lingering longer in the workforce or extending their exposure to the stock market.

Second, four percenters can reach WARM by cutting expenses. For example, retirees with burn rates of $40,000 need a $1 million nest egg to fund a 30-year retirement under the Four Percent Rule (see chart above). If, however, these retirees reduce their spending to $35,000, a similar-sized nest egg funds a switch to WARM. (Those who enjoy frugal living will likely prefer spending cuts to longer stays in the workforce.)

Third, to reach WARM retirees can combine larger nest eggs with lower†burn rates in whatever mix they find most palatable.

*†† *†† *

To sum up:

WARM elevates expense management (which you can control) over portfolio performance (which you can’t control). In the process, WARM lowers the risk of outliving your money, removes the need for expert advisors, and cuts income taxes. The price you pay for all this tranquility is: (1) a slightly larger nest egg; (2) a slightly lower burn rate; or (3) a thoughtful mix of each. https://95948dd14fec2e0c7cb1288eac8fbbf1.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

So what do you think of WARM? Is it something you would consider or is it too conservative for your tastes?

***********************************************

As he indicates in the last line above, Mr. Moose has promised to tune in and respond to your questions, concerns and challenges in the comments below.

As for me, I’ll stick with the approach I describe here on the blog and in The Simple Path to Wealth. But then, I know I’ll stay the course when the storms arrive. But the question you have to ask yourself, and that only you can answer, is: Will you?

Addendum:The Mad Fientist interviews Michael Kitces, who is one of the great researchers on the 4% rule and retirement strategy. An important and fascinating conversation.**********************************************

A while back I had a blast with Brad & Jon on their podcast Choose FI. So we did another:

NewRetirement offers cool tools to help guide you in answering the question: Do I have enough money to retire? And getting started is free. Sign up and you will be offered two paths into their retirement planner. I was also on their podcast and you can check that out here:Video version, Podcast version.

Credit Cards are like chain saws. Incredibly useful. Incredibly dangerous. Resolve to pay in full each month and never carry a balance. Do that and they can be great tools. Here are some of the very best for travel hacking, cash back and small business rewards.

Personal Capital is a free tool to manage and evaluate your investments. With great visuals you can track your net worth, asset allocation, and portfolio performance, including costs. At a glance you’ll see what’s working and what you might want to change. Here’s my full review.

Betterment is my recommendation for hands-off investors who prefer a DIFM (Do It For Me) approach. It is also a great tool for reaching short-term savings goals. Here is my Betterment Review

Republic Wireless is my $20 a month phone plan. My wife is also on the $20 plan and our daughter who uses more data is on the $25 plan. Monthly total for three phones and plans: $65. We all travel widely and we can talk to each other from wherever we are and for however long we please. My RW Review tells you how.

These are companies I have personally vetted and recommend.

YNAB and Tuft & Needle both support this site with paid ads. If you click on those ads it shows them the ads are working for them and that support will continue.

Personal Capital, Betterment and Republic Wireless are affiliate partners of this site. Should you click though to their site from this one and chose to do business with them, this blog will earn a small commission.

Vanguard is not an advertiser or affiliate but, Vanguard if you are listening, we’d love to have you!

Simple is good. Simple is easier. Simple is more profitable.

What I’m going to share with you in these next couple of articles is the soul of simplicity. With it you’ll learn all you need to know to produce better investment results than 80% of the professionals and active amateurs out there. It will take almost none of your time and you can focus on all the other things that make your life rich and beautiful.

How can this be? Isn’t investing complicated? Don’t I need professionals to guide me?

No and no.

Since the days of Babylon people have been coming up with investments, mostly to sell to other people. There is a strong financial incentive to make these investments complex and mysterious.

Babylon

But the simple truth is the more complex an investment the less likely it is to be profitable. Index Funds out perform Actively Managed Funds in large part simply because Actively Managed Funds require expense active managers. Not only are they prone to making investing mistakes, their fees are a continual performance drag on the portfolio.

But they are very profitable for the companies that run them and as such are heavily promoted. Of course, those profits come from your pocket. So do the promotion costs.

Not only do you not need complex investments for success, they actually work against you. At best they are costly. At worst, they are a cesspool of swindlers. Not worth your time. We can do better.

Here’s all we are going to need: Three considerations and three tools.

The Three Considerations.

You’ll want to consider:

In what stage of your investing life are you: The Wealth Building Stage or the Wealth Preservation Stage? Or, mostly likely, a blend of the two.

What level of risk do you find acceptable?

Is your investment horizon long-term or short-term?

As you’ve surely noticed, these three are closely linked. Your level of risk will vary with your investment horizon. Both will tilt the direction of your investing stage. All three will be linked to your current employment and future plans. Only you can make these decisions, but let me offer a couple of guiding thoughts.

Safety is a bit of an illusion.

There is no risk free investment. Don’t let anyone tell you differently. If you bury your cash in the back yard and dig it up 20 years from now, you’ll still have the same amount of money. But even modest inflation levels will have drastically reduced its spending power.

If you invest to protect yourself from inflation, deflation might rob you. Or the other way around.

Your stage is not necessarily linked to your age.

You might be planning to retire early. You might be worried about your job. You might be taking a sabbatical. You might be returning to the workforce after several years of retirement. Your life stages may well shift several times over the course of your life. Your investments can easily shift with them.

If you don’t yet have yours, start building it now. Be relentless. Life is uncertain. The job you have and love today can disappear tomorrow. Nothing money can buy is more important than your fiscal freedom. In this modern world of ours no tool is more important.

Don’t be too quick to think short-term.

Most of us are, or should be, long-term investors. The typical investment advisor’s rule of thumb is: subtract your age from 100 (or 120). The result is the percent of your portfolio that should be in stocks. A 60-year-old should, by this calculation, have 40% in conservative, wealth preserving bonds. Nonsense.

Here’s the problem. Even modest inflation destroys the value of bonds over time and bonds can’t offer the compensating growth potential of stocks.

If you are just starting out at age 20 you are looking at perhaps 80 years of investing. Maybe even a century if life expectancies continue to expand. Even at 60 and in good health you could easily be looking at another 30 years. That’s long-term in my book.

Or maybe you have a younger spouse. Or maybe you want to leave some money to your kids, grand kids or even to a charity. All will have their own long-term horizons.

Once you’ve sorted thru your three considerations you are ready to build your portfolio and you’ll need only these three tools to do it. See, I promised this would be simple.

1. Stocks. VTSAX (Vanguard Total Stock Market Index Fund) You’ve already met this fund in earlier posts of this series. It is an index fund that invests in stocks. Stocks, over time, provide the best returns and with VTSAX, the lowest effort and cost. This is our core wealth building tool and our hedge against inflation. But, as we’ve discussed, stocks are a wild ride along the way and you gotta be tough.

2. Bonds.VBTLX (Vanguard Total Bond Market Index Fund) Bonds provide income, tend to smooth out the rough ride of stocks and are a deflation hedge. Deflation is what the Fed is currently fighting so hard and it is what pulled the US into the Great Depression. Very scary. The downside for bonds is that during times of inflation and/or rising interest rates they get hammered.

3. Cash. Cash is always good to have in hand. You never want to have to sell your investments to meet emergencies.

Cash is also king during times of deflation. The more prices drop, the more your cash can buy. But idle cash doesn’t have much earning potential and when prices rise (inflation) its value steadily erodes. https://63d5933afa7f32dd13ea0e993bc120e1.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

We tend to keep ours here: VMMXX This is a Money Market Fund and time was they offered higher yields than banks. These days, with interest rates near zero, not so much. Now we also keep some in our local bank. If you prefer, an on-line bank like ING works fine too.

So that’s it. Three simple tools. Two Index Mutual Funds and a money market and/or bank account. A wealth builder, an inflation hedge, a deflation hedge and cash for daily needs and emergencies. Low cost, effective, diversified and simple.

You can fine tune the investments in each to meet the needs of your own personal considerations. Want a smoother ride? Willing to accept a lower long term return and slower wealth accumulation? Just increase the percent in VBTLX.

Next time we’ll talk about a couple of specific strategies and portfolios to get you started.

Meanwhile, a brief note on….

You will have noticed Vanguard is the company that operates all of these funds. It is the only investment company I recommend, and the only one you need (or should) deal with. Vanguard’s unique structure means that its interests and yours are the same. Vanguard the company is owned by the Vanguard funds. In other words, by us, the fund shareholders. This is unique among investment companies.

Awhile back a commentator on Reddit, referring to one of my posts, said: “This really just looks like a commercial for Vanguard.” I can see his point, although I wish he’d made it directly on here.

I am a huge Vanguard fan, but I am not on their payroll and I have no financial interest in the company other than owning the funds I describe.

You might find an index fund in another investment company that is a bit cheaper. They create some as “loss leaders.” But you can’t trust these other companies long-term. Their interests are not your interests. Their interests lie in making money for their owners.

If you play with snakes, to quote Dave Ramsey, you’ll eventually get bitten.

Story goes that back in 1929 Joseph Kennedy was getting his shoes shined and the shoeshine boy began offering him stock tips. Kennedy promptly returned to his office and sold all his shares. The market crashed and the cash he was sitting on suddenly became the most valuable thing you could own in the new deflationary age of cheap assets.

While I am honored by the accolade the fourth runner-up, and a book I happened to be re-reading at the time, is more deserving of the win:

This short, 158 page book by George S. Clason first published in 1926 and then again several times during the depression, is easy to dismiss. The stories, parables really, in it are charming and quick to read. Indeed my only criticism is that too many breeze through it without the needed reflection to absorb its profound lessons.

For example…

The Five Laws of Gold

The First Law

Gold cometh gladly and in increasing quantity to any man who will put by not less than one-tenth of his earnings to create an estate for his future and that of his family.

I wonder how many read that and miss the “not less than” part. In later stories in the book, he more commonly tells of people who “put by” 30%. My own book has occasionally come under attack for suggesting 50%. Maybe Clason was just smarter than I and figured he’d scare off fewer people by easing them in with 10%.

The Second Law

Gold laboreth diligently and contentedly for the wise owner who finds for it profitable employment, multiplying even as the flocks of the field.

But it is up to you to find that employment for it.

The Third Law

Gold clingeth to the protection of the cautious owner who invests it under the advice of men wise in its handling.

This might sound like advice to run to a financial advisor. It is not. It means don’t be careless with your money and don’t invest on the tips of your friends. Or your shoeshine boy.

The Fourth Law

Gold slippeth away from the man who invests it in business or purposes with which he is not familiar or which are not approved by those skilled in its keep.

This is why you can find many people who have sworn off the stock market. They invested on a hot tip that seemed to be working for others and lost. They didn’t take the time to understand what the market really is and how it really works before sending their gold to work there. https://36bffded68cff00c260315862efa6d01.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

The Fifth Law

Gold flees the man who would force it to impossible earnings or who followeth the advice of tricksters and schemers or who trusts it to his own inexperience and romantic desires in investments.

This one seems pretty clear.

One very interesting thing, maybe because I get so many asking about buying gold as an investment, never once does the book suggest holding gold for its own sake.

Today’s FOMO investments

As you read through those five laws of gold, do all those recent “investments” that seem to be making everyone millionaires overnight come to mind? Me too.

And for all those racked with FOMO who have been asking my opinion of them, perhaps even looking for my blessing, I refer you now to these five laws.

But what, you may ask, about those who have become millionaires with these investments? Even if they are few, doesn’t that mean it is possible? Worth a shot?

Gold Dust

A couple of months ago, I shared with you my sad tale of Mariah International. It cost me a cool $50,000, at a time when that was real money.

It was a very tough loss, hard on my wealth and my ego. But it was not the worst possible outcome. In that post I also shared with you this:

“It could have worked. And if it had, I very likely would have myopically seen it as the result of my astute investing prowess and totally missed how much a role luck would have played.

“That last, of course, would have lured me into being even more confident and aggressive on the next one. And that hubris mostly leads to tears.”

Casinos typically pay out upwards of 90% of the bets placed in winnings. Ever wonder why? The obvious answers are…

If people walking in saw no one winning, they’d be less likely to play themselves.

The house wants people around the roulette wheel and crap table pumped and excited, and those slots showering out coins and flashing lights.

It creates excitement and dreams of possibilities. It encourages reckless behavior.

That seemingly small 10% or less take makes for huge and sustainable profits.

The Federal Debt has is skyrocketed to over 28 Trillion Dollars with no end in sight.

The Debt will very likely be over 30 trillion by year’s end. To put that in perspective, five years ago, in 2016, it was under 20 trillion. Ten years ago it was ~14 trillion.

On the other hand…

We are beginning to roar out of covid with a huge pent-up demand that should see the economy surge.

The Fed Chairman, Jerome Powell, just predicted a growth rate of over 6% for 2021.

All the money the Fed is pumping into the system drives up the price of stocks, as well as all those houses and staples.

Owning stock means owning a tangible part of a business. These underlying businesses provide an inflation hedge.

So to answer all those who have asked me in recent months, is this time different? Is this the time to sell and wait it out? To try to time the market and “dance in and out” as Warren Buffett once said (meaning it was the road to losses)? In short:

As I have said from the beginning, the market is unpredictable. Timing it, even when – maybe especially when – what it must do next feels so obvious, is impossible.

I’m tempted to belabor this point, but if you have read this blog and/or The Simple Path to Wealth you’ve already heard it. If you haven’t, I invite you to do so now.

So what should you do?

If and when the crash comes, now is the time to be absolutely sure you are prepared to do…

If you are in the Accumulation Stage and are aggressively adding to your stock investments from the cash flow of your earned income, a market crash is a blessing. Your dollars buy more shares at lower prices.

If you are in the Preservation Stage and living on your investments, your allocation in bonds serves to smooth the ride. During market run ups, as your allocation tips to a greater percentage of stocks, you are rebalancing your allocation by selling those off at high prices to increase your percent of bonds. When stocks plummet, your bonds are your “dry powder” which allow you to pick up those now cheap stocks as you rebalance again.

The market may be crashing as you read this. It might crash next week. Or next month. Or later this year. Or years from now. But as the very first post in my Stock Series is titled…

And another after that. They are a natural part of the process. No one can predict them. As long as you don’t panic and sell, they don’t matter. But make no mistake, they can be terrifying.

Now is the time to make sure your Asset Allocation is such that you can tolerate the storm. If you wait until the storm is upon us, it is too late. Review and, if you feel the need, adjust now while the seas are calm and then…

Tie yourself to the Mast

What you should not do.

In these times of a seemingly endless rise in the markets, don’t fall prey to the temptation to become more aggressive in your holdings. Stay faithful to the allocation you chose when market crashes might have seemed more likely.

And, when the crash does finally come, don’t panic and sell. Stay the course. Resolve now that, for you, during a market crash:

Selling is not an option.

If you have any doubts about your ability to do this, do not follow my investing path. There is no shame in this, and here is an alternative to consider…

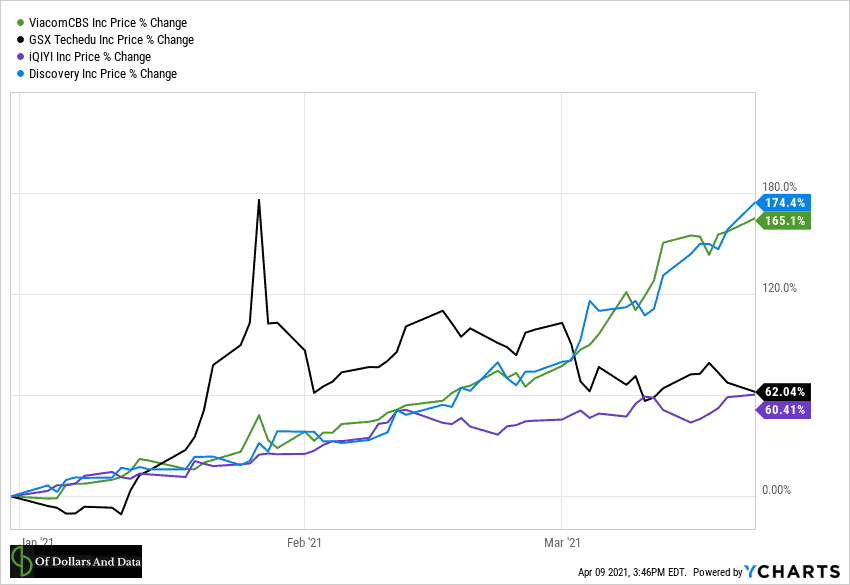

The biggest story in finance over the past few weeks concerns Bill Hwang, the founder of Archegos Capital, who lost a record $20 billion in the span of two days. How did he do it? Leverage and lots of it.

Hwang had levered up about 5x through an assortment of swaps contracts on a handful of individual stocks. The payoffs on these swaps were relatively simple: If Hwang’s stocks were up on the day, his banking partners paid him cash, and if they were down on the day, he paid them cash. From the beginning of 2021 through mid March, this strategy worked wonders for Hwang. Below is a chart illustrating the performance of some of his major holdings over this time period:https://tpc.googlesyndication.com/safeframe/1-0-38/html/container.html

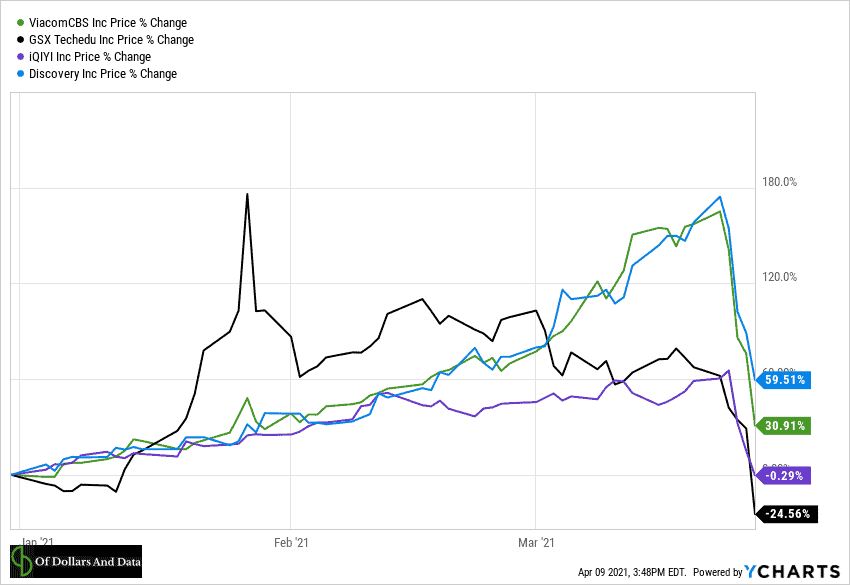

But, then this happened over the course of the next few days:

After experiencing such a severe decline across his portfolio, Hwang had to come up with significant amounts of cash to pay his banking partners. Unfortunately, he didn’t have it. As a result, some of his banks took swift action and began liquidating his positions, causing further losses. As the liquidations mounted, Archegos entered a death spiral. Within two days, Hwang’s fund had lost $20 billion.https://tpc.googlesyndication.com/safeframe/1-0-38/html/container.html

While it would be easy for me to write a post criticizing Hwang for using too much leverage, that idea isn’t particularly interesting to me nor particularly helpful to you. Not only have I written about this topic before, but individual investors like you and I aren’t allowed to borrow at these levels anyways. Warning against the use of 5x leverage would be like warning against the dangers of getting injured while playing in the NFL. It is a risk, but not one that 99.9% of people have to worry about.

But what is intriguing about this story is what it illustrates about how we think about wealth. Based on what I’ve read, Hwang now holds the record for the fastest loss of wealth in history. Mark Zuckerberg once lost $16 billion in a single day after Facebook shares plunged by 19% in July 2018, but that was an unrealized loss (on paper only). Since Zuckerberg didn’t sell his shares and Facebook’s share price is now 50% higher than it was before the decline, the loss doesn’t really count.

But I don’t think Hwang’s loss of $20 billion counts either. Because if Hwang had tried to get out of his positions in the days before they crashed, I doubt he would have been left with $20 billion (or anywhere near that) anyways. You can say the same thing about ultra-billionaires who have most of their wealth in one (or a few) assets.

For example, Elon Musk currently owns over $100 billion worth of Tesla stock. If he decided to liquidate all of it, how much of that $100 billion do you think he could actually realize? I have no clue, but I doubt he gets away with more than $50 billion of it. In the process of selling his shares, Tesla’s stock price would go into free fall. Not only would there not be enough buyers to support the price, but once investors found out that Musk was selling, many of them would lose confidence in the stock as well. Of course, Musk would never do such a ridiculous thing, but it illustrates how large sums of wealth are illusionary in the first place.https://tpc.googlesyndication.com/safeframe/1-0-38/html/container.html

So when we talk about Bill Hwang’s $20 billion loss, we aren’t really talking about the destruction of 20 billion in realized dollars. It’s not like Hwang took $20 billion in cash and built a position up over time that eventually went up in flames. In fact, it’s the opposite. He took a small amount of money and grew it very quickly by using increasing amounts of leverage. This wealth never really existed anywhere besides on paper.

“But isn’t most wealth on paper though?” Well, yes, but most people can realize that wealth. For example, if I decided to sell every asset I own tomorrow, I would be able to realize all of it at the market price without taking any significant haircut. Since I own small amounts of highly liquid assets, my choice to sell would have no material impact on the market price. This is probably true for 99.9% of people.

However, for those that have larger amounts of wealth, especially in illiquid assets, that’s when things become distorted. Yes their wealth can be measured on paper, but they don’t really know how much they have until they sell. History is filled with examples of ultra-rich individuals who learned this lesson the hard way.

This doesn’t mean that Hwang’s loss at Archegos is unimportant, but that it’s probably less extraordinary that it initially appeared. Because, in Hwang’s case, very little of substance was actually lost. It’s not like $20 billion of physical capital was destroyed or economic activity was reduced by $20 billion. No, his inflated assets were deflated and his true loss was much smaller.

It would be like if you owned an aircraft leasing company with 10 Boeing 747s listed on your balance sheet at $400 million a piece ($4 billion in total). However, after COVID-19 hit, you discovered two things: (1) your airplanes are now worth only $300 million a piece, and (2) you had miscounted and actually only own nine Boeing 747s after all. Now your listed assets are worth $2.7 billion ($300 million * 9 planes) down from $4 billion.

Did you just experience a $1.3 billion loss? No, you experienced a $900 million loss. Since one of your planes never existed in the first place, that additional $400 million was never really lost. This is kind of like what happened to Hwang and Archegos where the value of their individual positions were the equivalent of that extra, non-existent airplane.

Yes this analogy isn’t exactly correct, but it gets at the underlying idea. In some cases, wealth isn’t what it seems. We can see it. We can count it. We can write it down on a piece of paper. But as soon as we go to touch it, it disappears. Like a financial hologram. Like something that never truly existed.

While you may never experience any such thing during your lifetime, there will be people who you know who will. They will overvalue their assets. They will believe their home or business or other asset are worth more than they really are. They will make financial decisions based on this information too. But, one day, they may realize the uncomfortable truth—not all wealth is real.

Hever’s bold featured Images and bright, cheerful colors are ready to get to work for your business.

Hever is a fun and friendly free WordPress theme that works particularly well for creative and crafty businesses.

We also love it for weddings! Couples love its vibrancy and personality. As a WordPress wedding theme, Hever can be personalized with engagement photos and more, and adding pages for important information like menu options, accommodations, guest lists, and wishlist is intuitive and user-friendly.

Plus, it’s a responsive theme that displays your site perfectly on all desktop and mobile devices. Whether you’re a creative freelancer launching a career, a small business with a colorful brand, or a bride-to-be, Hever can do the job!

It’s our business to help you succeed online

We know starting from scratch can be daunting, so we included clear, step-by-step instructions and video tutorials to help you build an attractive website. If you’d like to skip right to a specific section, click on the relevant link:

You’ll be using the Customizer to configure your site’s look and feel. To access the Customizer, click on My Site in the top-left corner of the screen, look for the Personalize section in the sidebar, and click on Customize. (Going forward we’ll use the Customize → X format to point to a specific section within the Customizer.) Learn more about the Customizer here.

When you’re ready to exit the Customizer, click the X in the top-left corner. Whenever you make changes you’d like to keep, click on the blue Publish button, just to the right of the X button. Don’t worry, we’ll remind you to save your progress as you go. Let’s get started!

Setting up your Homepage

The demo site uses a static homepage. Follow these steps to achieve the same look:

Publish two pages and give them titles that are easy to remember, like “Home” and “News.” To publish a page, navigate to My Site → Pages → Add Page.

Next, go to Customize → Homepage Settings.

Select “A static page” and choose the two pages you published in Step #1 — “Home” and “News” — as your Homepage and Posts page, respectively.

You can give your site a more streamlined look by hiding the static homepage title. To do this, scroll down to the bottom, and check Hide Homepage Title.

Click the Publish button on top to save your changes.

Adding content to your Homepage

Hever fully supports the new WordPress Editor. You can choose any of the available blocks to create a wide range of content for your site. Here’s how we built the homepage on the demo site, block by block:

Adding Your Logo

If your business has a logo, you can display it in your site’s header. Here’s how:

Open My Site → Customize and click on the Site Identity section.

Click the Add logo button to open the Media Manager.

Upload a new image, or select one that’s already in your Media Library.

Click Set as logo and you’ll see your logo appear in the preview.

If your logo includes your site’s name or you prefer the header only to display your logo, you can hide the site title by unchecking the box next to Display Site Title.

Click the Publish button on top to save your changes.

Your logo will appear to the left of the site title on desktop computers, and above the Site Title on mobile devices. The maximum height of the logo image is 60px, while the width can be adjusted as needed.

Adding Site Navigation

It’s time to create a navigation menu to help your visitors find the information they’re looking for. The first step is to create a menu, following these instructions. Once you’ve created the menu, you can pick where you want it to go.

Head to Customize → Menu.

Select the Menu Locations panel.

Assign the menu you’ve just created to the Primary Location.

Click the Publish button on top to save your changes.

With Hever, you have the option to display links to your social media accounts in the header, right below the main site navigation. To do that, you’ll first need to set up a Social Links Menu. Once you’ve done that:

Head to Customize → Menu.

Select the Menu Locations panel.

Assign the menu you’ve created to the Social Menu Location.

Click the Publish button on top to save your changes.

You can download Hever to use on your self-hosted site using the link below. It is a child theme of Varia, so you will also need to download a copy of the WordPress.com version of that theme, available here.

While there are several ways visitors to your site can follow your WordPress.com blog, you also have the ability to create a Follow Blog button that can be added to external websites. This button will allow people who click on it to receive e-mail notifications whenever you publish a new post on your WordPress.com site.

If you’re looking to add it to an external website that supports JavaScript embeds, then you’ll start by visiting our Follow Button Generator.

In the Generator, you will need to enter the URL of the WordPress blog for which you’d like to create the button. Next, choose whether you’d like to show your current follower count next to the button, and whether you’d like to show your blog’s name in the button text. Also, choose the default language for the button.

This is how the button looks, with and without your follower count:

Once you complete the form, click the Generate button to get the embed code. Copy all the text from the code box, and paste anywhere that supports JavaScript embeds to add the Follow button!

The follow button is a small button that you can add to any site, that will allow WordPress.com users to easily follow the specified WordPress.com or Jetpack enabled blog.

Note: In order to generate the code for your Jetpack enabled blog, you must have the JSON API module activated on it.

Use the options below to generate the code for your WordPress.com Follow Button. You can use the generated code snippet to embed the Follow button anywhere you’d like to on the web.

Jetpack is one of the most popular plugins for WordPress and it includes a variety of tools to help you improve and grow your website. However, as Jetpack offers so many features, it can be hard to gain a good understanding of what it offers and whether it is a good choice for your new WordPress website.

The purpose of this Jetpack Guide is to de-mystify Jetpack and to introduce you to some of its best modules. By the end of this article, you will know whether Jetpack would make a good addition to your new website or blog. And you will have a good understanding of which modules to activate.

What is Jetpack?

Jetpack claims to be the ‘ultimate toolkit for WordPress’. This free plugin includes a suite of modules that can enhance your website in many ways. Some of this functionality covers improving your WordPress site security, increasing traffic and helping you customize your site’s design. As Jetpack was created by Automattic, the same team that runs WordPress.com, by installing this plugin you can gain access to some of the features that websites hosted on this service enjoy.

The main appeal of Jetpack is that it provides all the features and functionalities required to run a successful WordPress website in just one package. So instead of having to research, install and set up multiple tools, all you need is Jetpack’s one plugin. Site stats, state of the art security services, traffic generation tools, and design customization functionality are just some of the advanced features provided by Jetpack.

While the core Jetpack plugin and the majority of its modules are free, there are some advanced optional premium tools available. However, the free version provides more than enough tools to get started with.

How to Install Jetpack on Your WordPress Website

Before you can activate any of the Jetpack modules you will need to install the core plugin on your WordPress website.

Log in as admin on your site. Then within your WordPress dashboard, select ‘Plugins > Add New’ from the menu bar.

Type ‘Jetpack’ into the plugin search bar. Once the Jetpack has been retrieved, click on ‘Install Now > Activate’.

You will now be asked to connect your website with WordPress.com. Here you can create a new account with WordPress.com. Or if you are already signed up with WordPress.com you can add your website to your existing account.

Once you have registered, WordPress.com will ask you which Jetpack plan you would like to opt for. For now, simply select the ‘Free’ plan.

You will now be returned to your WordPress dashboard, where you will see that a ‘Jetpack Menu’ has been added to your site’s menu bar.

Activate Jetpack’s Recommended Features

Once your plugin is installed the first thing Jetpack encourages you to do is bulk ‘Activate’ their recommended features. Most of these features are in fact turned on by default when you install the plugin and can be de-activated if you so choose.

But before you choose to activate all these recommended tools, or turn them off, let’s find out what each of these Jetpack modules offers. And how they can help improve your WordPress website…

Sharing

In your WordPress menu select ‘Jetpack > Settings’. This is where you can find and activate, or deactivate, the numerous Jetpack modules.

Select the ‘Sharing’ tab. You will now see two different ‘Sharing modules’ that Jetpack recommends activating.

Publicize Connections

‘Publicize Connections’ allows you to automatically publish blog posts to your social media channels. To add this feature to your WordPress website, click on the ‘Activate’ button under ‘Publicize Connections‘. Then select ‘ Connect Your Social Media Accounts’. You will now be taken to your WordPress.com account, where you must connect and authorize any social media networks you would like to automatically publish your blog posts to.

Once set up, articles will be automatically displayed on your social media networks each time you click to ‘publish’ an article on your site. You can also add a custom message to be sent out with each post.

Activate Publicize Connections if you would like a quick and easy way to publish your posts on social media and get your content shared. Upgrading to Jetpack’s paid plans will also allow you to reshare, as well as schedule, your blog posts for social media publishing.

To set up this feature, select the ‘Activate’ button under ‘Sharing Buttons’, then select ‘Configure Your Sharing Buttons’. Within the WordPress.com dashboard, you can choose which social media buttons you would like displayed, alter the look of the text and icons, and decide where you would like the buttons placed.

Sharing Buttons is another great social media Jetpack module and a must have for those looking to get their content shared.

Subscriptions

‘Subscriptions’ has been created to make it easy for visitors to subscribe to your content, and for you to collect users emails. Under ‘Jetpack > Settings’, select the ‘Discussion’ tab to find the ‘Subscriptions’ module.

By activating ‘Subscriptions’ on your website, visitors have the option of subscribing to your blog. They can also follow individual article’s discussions. WordPress.com stores the collected emails and visitors are automatically notified via email of new comments or blog posts published on your site.

This is an extremely effective way of collecting leads and keeping in contact with your audience. By sending emails to keep your audience informed of what is happening on your blog, they are more likely to return and become regular readers.

Gravatar Hovercards

A gravatar hovercard is the card that is displayed when you hover over a person’s gravatar. This displays information about the person, including their full name, a blurb about them, and a link to their full profile.

Using gravatars, and their hovercards, is an effective way to help foster an interactive community on your WordPress website. Visitors get to know each other by recognizing each other’s gravatars and reading up on each other. This creates a bond between your readers, and a feeling of familiarity with each other and your blog.

To activate Gravatar Hovercards, select the ‘Discussion’ tab. Under ‘Comments’, activate ‘Enable pop-up business cards over commenter’s Gravatars’.

Contact Form

Jetpack’s ‘Contact Form’ module enables you to add attractive contact forms to any page, post, or widget, of your WordPress website. Forms can be customized, enabling you to edit the fields displayed, alter the email address, or change the subject settings. The appearance can also be tailored to suit your site’s design using CSS, and existing forms can be re-edited.

To add a contact form to your website simply open the specific page or post where you would like a form displayed. Above the editor, click on the ‘Add Contact Form’ icon. A pop-up will appear where you can configure the form. Then publish the page and your contact form will go live.

For each contact form response you receive you will be sent a notification email. And responses will be stored in the ‘Feedback’ section of your WordPress dashboard. So if you are looking for a simple, yet clean and sleek contact form, then make use of this easy to use Jetpack module.

Photon

Site speed is an important factor for all websites. Large images particularly can greatly slow your website down. Photon is an especially useful Jetpack module that helps deal with this problem.

Photon is an image acceleration and editing service. It works by serving images to your audience directly from the WordPress.com cloud. This means less load on your host and a much faster image delivery for your site visitors.

To activate Photon, simply switch to the ‘Writing’ tab on the ‘Jetpack Settings’ page. Scroll down the page to ‘Media’ and then activate the button next to ‘Speed up images and photos’. Photon is another must have Jetpack module, especially for websites that are image heavy.

Carousel

Carousel adds a fun and stylish dimension to your images and makes it easy for your visitors to view individual pictures. If you decide to use the Carousel feature, all images that are currently displayed in WordPress galleries on your posts and pages will be showcased in a full-screen carousel option.

To activate ‘Carousel’ on your WordPress website, click on the ‘Writing’ tab and scroll down to ‘Images’. Then turn on the button next to ‘Display images and galleries in a gorgeous, full-screen browsing experience’.

Here you can also select whether to show metadata in your carousel, as well as set a black or white background to complement your images. Carousel is a great choice if you already display WordPress galleries on your website, and are looking to improve the delivery of your images.

Tiled Galleries

Tiled Galleries allows you to display your image galleries in three distinct styles. You can choose from rectangular tiles, a square mosaic, or a circular grid. All three options provide an interesting and eye catching way to showcase your image galleries.

To set up Tiled Galleries, you first need the ‘Photon’ module that we have previously discussed to be activated. Then, when you create a new gallery, under ‘Gallery Settings’, select one of the three tiles options.

If you want you can make all of your image galleries tiled by default. In your WordPress dashboard menu select ‘Settings > Media’. Scroll down the page and under ‘Image Gallery Carousel’ tick to activate ‘Tiled Galleries’.

Tiled Galleries is another way to give your site an edge by displaying your images in stunning layouts. Activate this module if you want your photos and pictures to impress.

Related Posts

Displaying related posts underneath an article is an effective way to keep your audience on site. Showing visitors further information on a topic of interest will encourage them to click through to other pages to continue their reading.

The ‘Related Posts’ module scans and analyzes the posts on your website, and then displays related and contextualized articles at the bottom of each page. This tool differs from other related posts plugins as it processes and serves data from the WordPress.com cloud. This means that there is no additional load on your server.

To activate ‘Related Posts’, select the ‘Traffic’ tab. Then under ‘Related Posts’ activate the button next to ‘Show related content after posts’. Three related posts will now be displayed under each article, complete with thumb nail image and title. Jetpack also gives the option of adding a ‘Related’ header. This helps to show a distinct separation from the end of your post and the related suggestions.

Displaying related posts can dramatically increase your page views. So if your WordPress website has a thriving blog, then ‘Related Posts’ is a module well worth activating. The longer readers stay on your site and engage with your content, the more likely they are to return to read more at some point in the future.

Single Sign On

‘Single Sign On’ can be activated under ‘WordPress.com log in’. This is found in the Jetpack Settings ‘Security’ section. Once you have turned on this feature you will be able to log onto your site via WordPress.com. For extra security, you can activate the ‘WordPress.com Two Step Authentication’.

The ‘Single Sign On’ module is again another useful Jetpack tool. Not only does it help speed up and secure the login process, it also takes the stress out of remembering yet another password.

Brute Force Attack Protection

The security feature ‘Jetpack Protect’ is used to protect your WordPress website against brute force attacks. This module starts working automatically once you have connected your site to WordPress.com. It can also be found under ‘Security > Brute Force Attack Protection’.

Jetpack Protect works by blocking all suspicious looking login activity. You can view the number of thwarted attacks on your website by selecting ‘Jetpack > Dashboard’ from your WordPress menu. Jetpack also gives you the option of whitelisting your IP address, if you have made too many failed login attempts to your website.

This Jetpack module provides a necessary first line of defense for your site and will help protect your site from numerous malicious sign-in attempts.

Spelling, Style, and Grammar

Looking and sounding professional is crucial for websites representing businesses and career bloggers. So making sure the spelling and grammar is correct throughout your content should be a top priority.

Jetpack’s ‘Spelling, Style and Grammar’ module can be found under the ‘Writing’ tab. Activating this feature will enable Jetpack’s Proofreading technology to automatically check your writing in the Visual Editor. You can also configure the proofreading features, keeping the editing in line with your style of writing.

Activating this proofreading tool will ensure that your content is well written, and mistakes will be kept to a minimum. Ultimately, this will result in your visitors considering your blog to be a reputable source.

Site Stats

The ‘Site Stats’ tool tracks your site’s metrics and reports them in an easy to read overview. Find out how many visits your site gets, top posts and pages, the number of subscribers and likes received, and much more.

‘Site Stats’ is immediately activated once you link your website to WordPress.com. The stats report can be found under the ‘Jetpack > Site Stats’ page, and advanced stats are displayed in your WordPress.com dashboard. This module is a great way to monitor your site’s performance and gain an insight into what content is appealing to your audience.

Apart from the initial ‘recommended’ features, Jetpack provides many other useful tools that can be activated as and when you need. These are not all available within your WordPress dashboard, so you will need to log in to your WordPress.com account to access the full range of Jetpack modules.

Once you have signed into WordPress.com, select the ‘My Sites’ tab. Then click on ‘Settings’ at the bottom of the side menu. Here you will find the full list of Jetpack features. However, which ones will make a real difference to your site’s performance? Let’s have a look at some other important Jetpack tools, that we haven’t yet mentioned, in more detail…

Mobile Theme

Using an old theme, or a theme that hasn’t been updated for a while, means you run the risk of having an unresponsive website. As more and more people access websites on handheld devices, it becomes ever important to have a responsive site. If you are unsure of how your website looks on a smartphone or tablet then check it out for yourself. Ultimately, an unresponsive website will lead to high bounce rates, low search engine rankings, and a loss of returning visitors.

Jetpack’s ‘Mobile Theme’ module converts your current website into a mobile-friendly version. The mobile theme displays a clean and organized interface, using a one column layout to give your content more room when viewed on a small screen. This helps improve the user mobile experience and ensures site visitors can access your content. It is also extremely lightweight, keeping loading times fast.

To activate the ‘Mobile Theme’ module, within your WordPress.com dashboard, select ‘Settings > Writing’. Under ‘Theme Enhancements’ click on the button next to ‘Enable the Jetpack Mobile Theme’. Here there are a few other options you can choose from, giving you some control over how your theme is displayed on mobile devices.

Infinite Scroll

Also located under ‘Settings > Writing > Theme Enhancements’ is Jetpack’s ‘Infinite Scroll’ feature. If your WordPress website has a healthy blog, that spans numerous page, then this may be a useful tool for your website.

Infinite scroll enables your audience to quickly view unlimited amounts of information. As a visitor reads down the page, your blog will continuously display the next articles, without your audience ever having to load a page. This improves user engagement with your blog and helps increase time spent on site.

Monitor

If your website suffers from regular periods of downtime there can be serious consequences, including poor ranking in the search engines, and a loss of traffic. But unless you are on your site 24/7, it can be hard to keep track of just how often your website is offline.

Jetpack’s ‘Monitor’ tool monitors your website’s uptime. A WordPress.com server will check your website every 5 minutes and if your site has gone down you will be immediately emailed. A further email will be sent if your site is still down after an hour, and another email once your site is back up and running.

To turn on this module, log into your WordPress.com dashboard and select ‘Settings > Security’. Then simply activate ‘Monitor Your Site’s Uptime’. This is an effective way to track and consequently help fix your website’s downtime, improving your site’s performance.

High numbers of comments on your blog will promote discussion and create an engaged community on your site. The Jetpack ‘Comments’ module gives your visitors the ability to leave comments on your blog using their WordPress.com, Facebook, Twitter, or Google Plus accounts.

To turn on ‘Comments, within your WordPress.com dashboard select ‘Settings > Discussion’. Then select ‘ Allow readers to leave comments…’ By activating this feature, it suddenly becomes extremely easy for your audience to log in and share their thoughts on the article they have just read.

Sitemaps

Turning on ‘Sitemaps’ will help your website rank in Google, and other search engines. Sitemaps are files, that Jetpack will generate, which list each post and page that should be indexed by the search engines.

Within your WordPress.com dashboard, select Settings > Traffic’. Scroll down to ‘Sitemaps’ and activate ‘ Generate XML Sitemaps’. Jetpack will now automatically generate the sitemaps necessary.

Jetpack can produce two sitemaps, one for all search engines, and one specifically for Google News. However, publishers must be pre-approved for Google News before Google will issue a News site map. If you want to apply to get your posts listed on Google News, check out the Google News Guidelines.

An added extra from Jetpack is a variety of free and premium themes that are available through WordPress.com. Jetpack offers over 150 free professional built-for-purpose and multi-purpose themes. And an additional 200+ premium themes are included if you upgrade to Jetpack’s ‘Professional Plan’.

These beautiful themes cater for a range of website needs, and can all be previewed and installed via your WordPress.com dashboard. If you are looking for a new design for your website, Jetpack may well have the perfect theme for you.

The WordPress.com App

Another handy addition to the Jetpack suite of modules is the WordPress.com app. This app enables you to manage all your sites, from any one of your devices, and from any corner of the globe. Post from any location, check your site’s stats, connect with readers, and tinker with your Jetpack module settings, all from within the WordPress app.

The desktop app is available for Mac OS X (10.9+) and Windows (7+). Or download the mobile app on your IOS or Andriod. This useful app is ideal for those on the go. And will make it even easier to manage the many Jetpack tools used on your WordPress website.

Jetpack’s Premium Features

Jetpack offers three different premium plans, all providing advanced features and functionalities for your WordPress website. Here are just some of the extras they offer…

Daily and Real Time Off-Site Backups

Unlimited Backup Archive and Storage Space

Automated Restores

Easy Site Migration

Daily Malware Scanning

SEO Tools

Unlimited Premium Themes

Priority Support

Jetpack’s premium plans cater for all needs, from the humble blogger and small online store, to larger businesses and global corporations. If you are looking to fit out your WordPress website with the full range of tools it needs to be truly successful, then a Jetpack premium plan may be a good option for you.

Final Thoughts

As you can see Jetpack has a lot to offer. Hopefully you have discovered a few modules that will benefit your WordPress website. If in doubt, initially activate Jetpack’s recommended features. Then take your time activating new tools, and deactivating the ones you don’t need, as you see fit.

Which modules do you think you will activate? Please share your thoughts in the comments below… The following two tabs change content below.

Megan is a freelance writer who loves all things WordPress. She currently lives in Brighton with her partner and two small children. When she isn’t online she likes walking by the sea, coffee and traveling anywhere and everywhere.

We know monetization is important for many site owners. We encourage and support, with some restrictions, the many methods of monetizing the hard work you put into your blogs and sites. You will find many of these options available at My Site → Tools → Earn. Read on to find out how you can turn your website into a source of income.

Comparing Payments Options on WordPress.com

Click the image to view in full size

Selling Physical and Digital Products

With the WordPress.com Business and eCommerce plans you can sell anything directly through your website with the free WooCommerce plugin. The plugin (with additional extensions) lets you sell products, handle shipping, collect taxes, and more. You can find more information on the WooCommerce website.

Pay with PayPal

Pay with PayPal allows you to accept credit and debit card payments on your WordPress.com and Jetpack-enabled sites. Whether you’re selling a physical or digital item, collecting payment for a service, or asking followers to show their appreciation financially, you can add a Pay with PayPal button to your site in a few clicks. The feature is available on Premium and Business plans on WordPress.com and on Jetpack Security and Jetpack Complete plans for your self-hosted site. Learn more about Pay with PayPal.

Payments

Payments let you collect recurring revenue from your site visitors and it can be used for anything from memberships and subscriptions to ongoing donations in support of your website. When a visitor signs up, you’ll start receiving regular payments from them — either monthly or yearly — creating predictable earnings for your blog or website. Provide subscriber-specific content with the Premium Content Block in the editor. Learn more about Payments and the Premium Content Block.

With the Premium Content Block, create monthly or yearly subscription options to share select content with those who pay for it – text, images, videos, or any other type of content. Only subscribers paying you monthly or a yearly fee will be able to see the content. Offer different subscription levels and customize the premium content available at each level. Click here to learn more.

Both the Payments and Premium Content blocks allow you to create subscriptions or memberships on your website. Learn all about creating a paid membership site with WordPress.com from our special tutorial site with more information and step-by-step information to get going.

If you’re just getting started, we recommend watching this video on what memberships are and how to add them to your website: https://www.youtube.com/embed/U2dViWZegQ8?version=3&rel=1&showsearch=0&showinfo=1&iv_load_policy=1&fs=1&hl=en&autohide=2&wmode=transparent

With any WordPress.com paid plan, you can solicit donations or tips from your readers using the Donations block.

You can also use Payments to accept ongoing credit card payments for recurring donations, tips, and support of your creative work.

Advertising

If you’d like to make money on your WordPress.com site with advertisements, WordAds is the official WordPress.com advertising program available for site owners. The program features ads from external ad networks such as Google, Facebook, AOL, and more. Learn more about WordAds.

Who is eligible for WordAds?

Users upgrading to the WordPress.com Premium, Business, or eCommerce plans have automatic access to the WordAds program and can set up advertising on their sites immediately.

Only sites with a custom or mapped domain can apply.

Advertising through third-party ad networks like Google AdSense, OpenX, Lijit, BuySellAds, and Vibrant Media, or selling advertising space on your site, is only permitted on sites that have the WordPress.com Business and eCommerce Plans. Sites on the WordPress.com Premium plan can use WordAds, Affiliate Linking, or Sponsored posts to generate advertising revenue, while the WordPress.com Personal and Free plans can use Affiliate Linking, or Sponsored posts.

Affiliate Linking

You can add affiliate links to your WordPress.com content as long as the primary purpose of your blog is to create original content, and as long as the code for the ad is supported.

When blogging about books you’re reading, music you love, clothes that strike your fancy, gadgets you’re drooling over, or whatever interests you and your readers, feel free to post relevant affiliate links using either text or images.

There are a few restrictions on what affiliate programs are allowed. We do not allow affiliate links for gambling, get-rich-quick schemes, multi-level marketing programs, disreputable merchants, pornography, malware, or phishing-type scams. We also do not allow sites that exist primarily to drive traffic to affiliate links.

You can publish sponsored posts on WordPress.com. We define a sponsored post as any content that promotes a specific product or service, which you were encouraged to post by the company or individual who makes/sells/provides it. Including this type of content on your site typically results in some kind of compensation for you in the form of payment, freebies, etc.

We do not allow sites where the vast majority of content is sponsored content. Sponsored posts also may not include any content that violates our Terms of Service.

Set up your online store in the morning. Celebrate your first sale in the afternoon.

Most of us want the freedom to make something meaningful, and to share what we’ve made with the right people.

If you’ve already invested in a blog on your own website, you’ve been in the business of strengthening relationships since your first post. Now that you’ve found a loyal audience, the natural next step is to start exploring how to monetize your site. If you know what your audience needs and you have an idea for how to help give it to them online, you’re already halfway there.

Whether you’re newly committed to turning your passion project into more of a moneymaker, or you’re just trying to earn some extra income on the side, setting up an online store will make it that much easier for your audience to support you. Here are some suggestions for getting started with a WordPress eCommerce website, and how to get to your first sale quickly and affordably.

Start small

Running an online store is ambitious, but starting a business can also be just that: a start.

Take it from someone who tried WordPress for the first time more than ten years ago, then dedicated himself to helping others get their start with WordPress. Before becoming our WooCommerce Payments Lead, Brent Shepherd built his own company, Prospress, which he founded to help new store owners prosper with WordPress. Brent now has more than a decade of eCommerce experience, and he still describes first installing WordPress in 2009 as “love at first site.”

A WordPress eCommerce plan provides all the essential functionality you’ll need at an affordable price point, especially if you’re new to eCommerce or online sales. “You can sign-up with just an email and a credit card,” Brent says, “and be selling online even if you don’t know what a server is, or a domain name.”

Whether you’re selling a service or a pillow with a corgi in a hat, a site that takes care of each transaction for you is going to make your first sale that much easier.

Celebrate your progress

I love reasonable goals. I’m fond of moonshot goals, too, when I’m feeling particularly inspired! But when I’m trying to make practical, everyday progress, nothing is more motivating than having a clear sense of what I want to achieve and a deadline that’s within reach. The easier it is to know that I’ve made progress, the better.

I come up with all of my goals while looking at a calendar. Ultimately I choose a dollar figure for how much money I’d like to make each month, but focusing on the immediate next step is always more useful than fantasizing about the end of the road. If you made $0 from online sales last month, even one sale this month is real progress.

If you can plan out how you’ll make your first sale, you’ll be able to apply those lessons and experiences to the second and the third. “Emailing friends-and-family is a great way to do that,” Brent says. You can also share an announcement post on social media with a link to your first product page. “I’ve seen stores selling all manner of products succeed,” Brent says, “from monthly subscription boxes containing dog toys for power chewers, to gourmet ice-cream!”

The Pay with PayPal block from WordPress.com