How Do I Retire Early-or Ever? Is Quitting Corporate Life an Option?

How to Create an Internet Archive

Published 22.03.2021 by Schmitt Trading Ltd

Have you also wondered why you cannot find the information on the internet again although you remember the correct website?

In the early days of the internet, I learnt to use the browser bookmarks to memorize websites that contain important information for me.

I exported these browser bookmarks regularly and even included them in my memory backups.

Nevertheless, I noticed that many websites including official “big” websites regularly redesign their content structure.

Or even worse, they move to a new domain or a new subdomain with a different structure.

Sometimes, they seem to rename pages or delete complete archives.

At some point, I had enough and started creating my own internet archive.

This was the reason that – back in 2015 – I registered with WordPress.com and created radiofan79 in German language.

Meanwhile, I wrote over 700 blog posts:

In the blog posts, I only reblogged the information I found on the internet that I found interesting and worthy to remember and archive.

All personal content was structured in pages. In six years, I created more than 130 pages:

With this short report, I would like to encourage you to build your own and personal internet archive.

Start immediately to register with WordPress.com and start designing the way you like!

Let me know about your efforts and follow our site. I will in return follow your site and can see in my WordPress Reader which topics you published lately.

Give it a try!

The Biggest Lie in Personal Finance

Posted February 4, 2020 by Nick Maggiulli

Last week, Michael Batnick brought the following article to my attention:

{kind=link}

Yeah, it triggered me.

It triggered me because without even reading the article I know that these “5 rules” have little to do with how they retired at 35. How do I know this? Because all of these early retirement articles are the same. They all say things like, “Make it a goal”, “Track your expenses”, “Establish a system.” Blah. Blah. Blah.

But none of these things are the actual reason for how they retired early. Because the actual reason is either (1) earning a high income or (2) having an absurdly low level of spending, or both.

In the case of the blogger that wrote the article mentioned above, I don’t know his income history, but I do know that, “He lives full-time in his 30′ Airstream Classic.” It’s too bad that one of his five rules wasn’t “retire in a trailer.”

But seriously, his advice has little to nothing to do with how he retired early. The reason his advice misses the mark is simple:

All the expense tracking and goal setting in the world cannot make up for an insufficient balance.

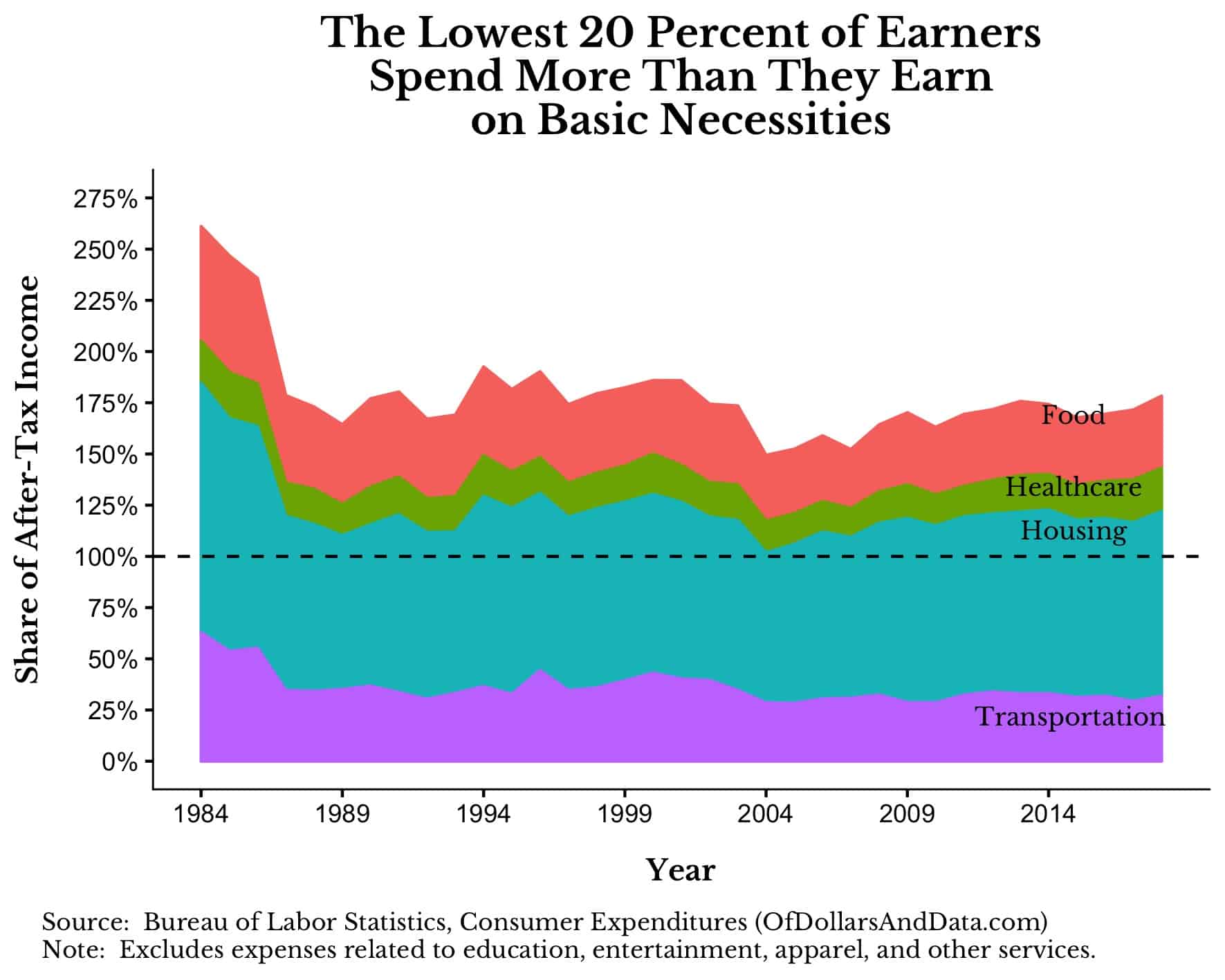

Don’t just take my word for it though. Consider what the Consumer Expenditure Survey from the Bureau of Labor Statistics has to say.

A Look at the Data

For example, if you look at the percentage of after-tax income that the poorest 20% of U.S. households spend on Food, Housing, Healthcare, and Transportation, it becomes quite clear that low income is the problem here:https://tpc.googlesyndication.com/safeframe/1-0-37/html/container.html

{kind=link}

Note that this doesn’t include any money for education, clothing, or any form of entertainment. Just the necessities swallow their entire paycheck and then some.

Considering that their annual after tax income is (on average) only $11,700, it’s likely that many of these individuals are younger and less experienced (i.e. students) than the typical American household. Because we don’t know the age or household size of these income cohorts, the comparisons are not necessarily apples-to-apples.

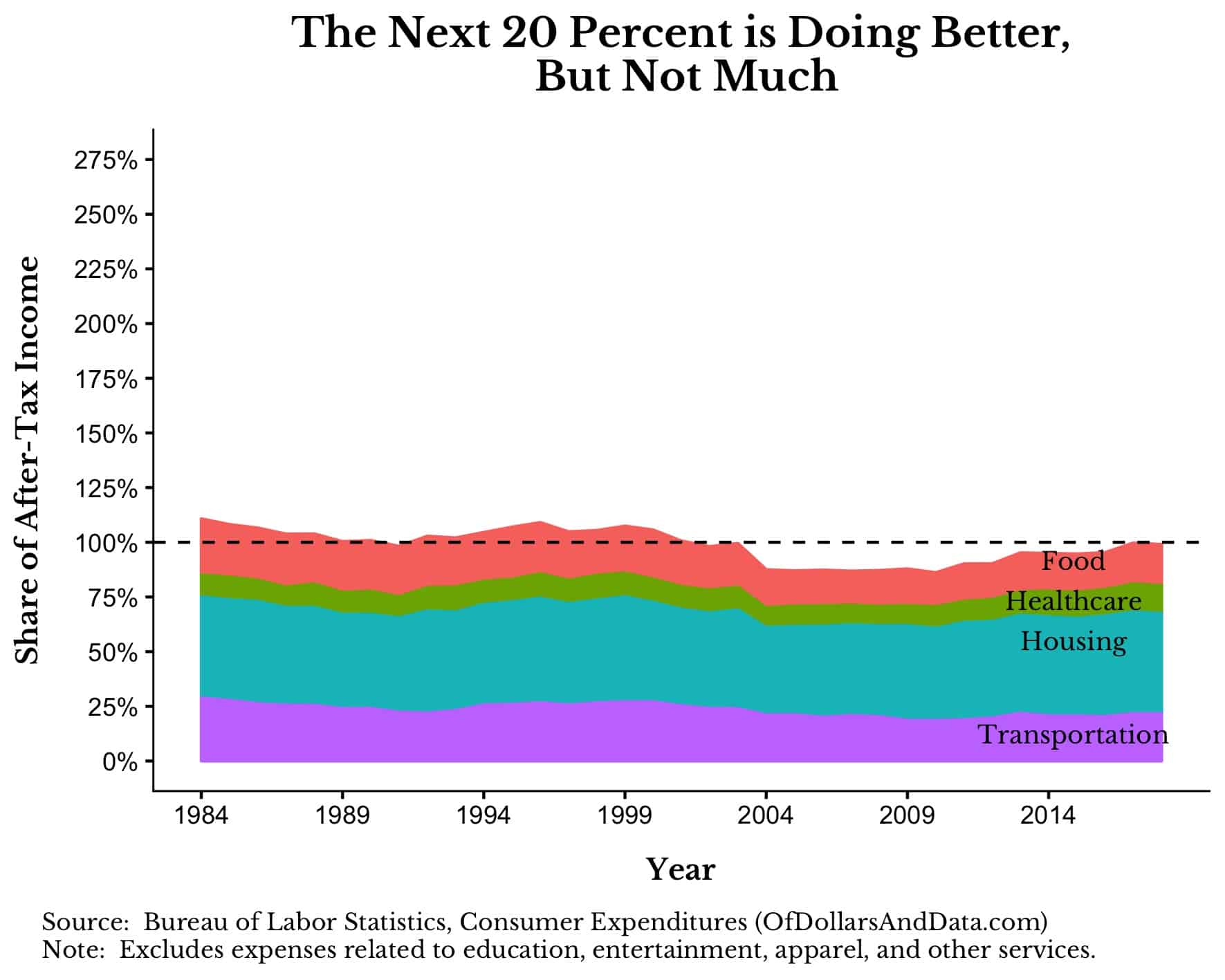

Despite this, the next 20% of U.S. households aren’t that much better off than the bottom 20%. For example, even though the next 20% of U.S. households has an annual after-tax income ~3x higher than the lowest 20% (at $31,200), they still spend most of their income on the necessities:

{kind=link}

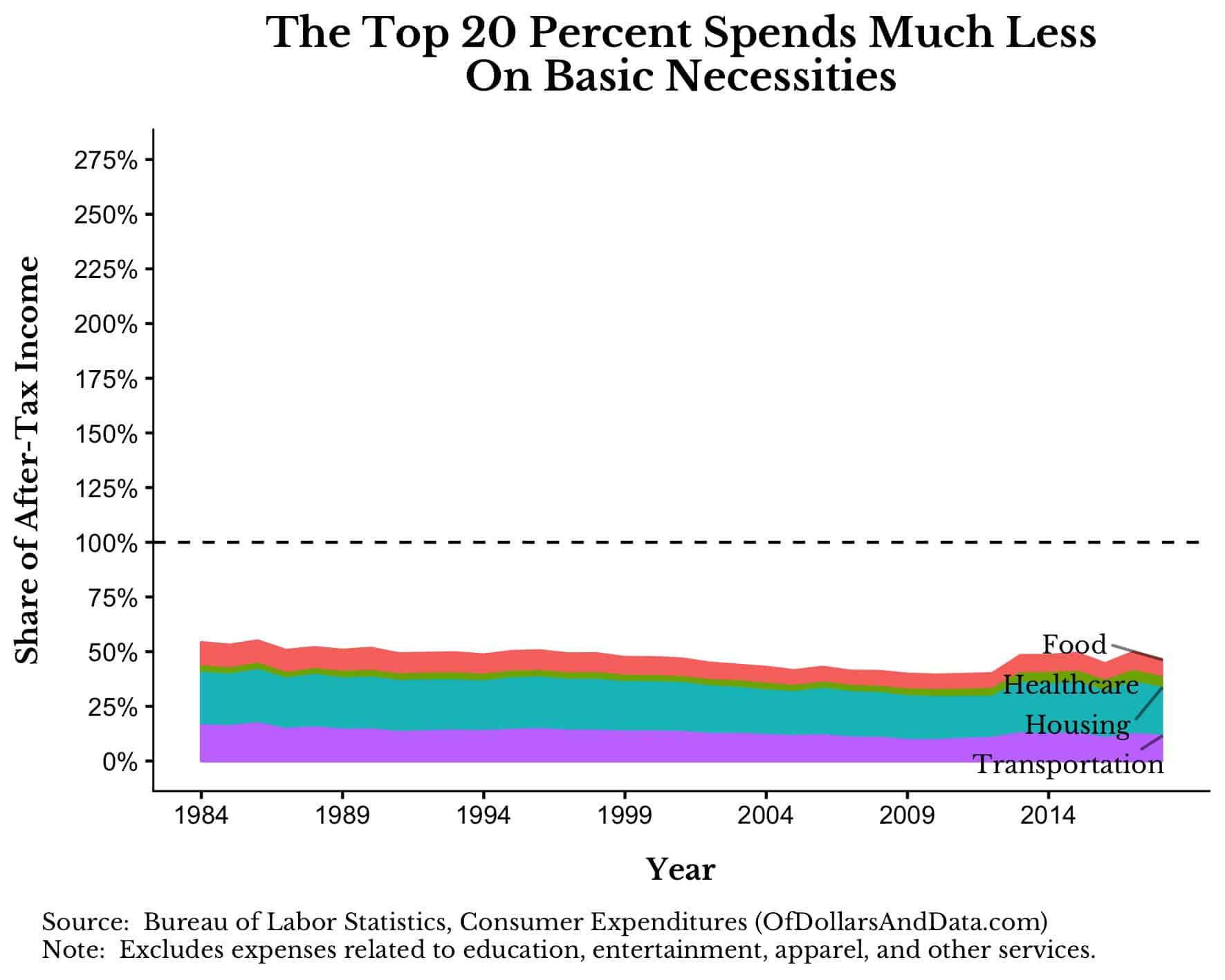

Meanwhile, the highest 20% of U.S. households, with an average income of $162,000, spend only about half of their take-home pay on the basics:

{kind=link}

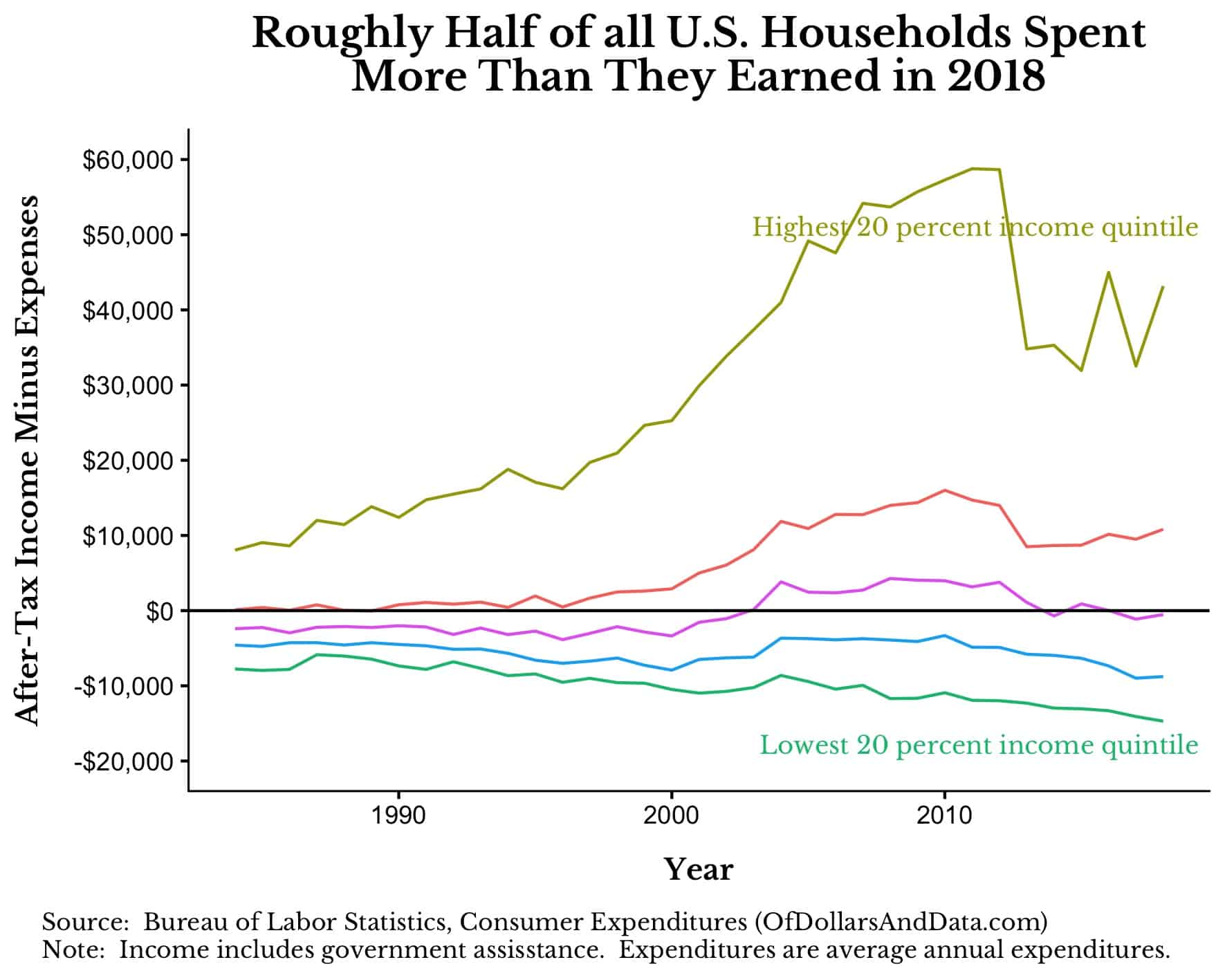

If we include expenses outside of the essentials, it looks like roughly half of all U.S. households spent more than they earned in 2018:

{kind=link}

This is an unfortunate reality, but one that more clearly demonstrates why so many U.S. households find it difficult to save money. They end up spending most of their pay on just the basics!

The Biggest Lie

After seeing data like this, it is hard for me to understand how any sort of expense tracking, goal setting, or “system” is going to fix it. Yes, some percentage of U.S. households don’t have the knowledge or habits or mindset to improve their financial situation.

You can probably think of a few people like this from your personal life. But, remember…n equals 1.

While there are lots of people who are in financial trouble because of their own actions, there are also lots of people with good financial habits who just don’t have sufficient income to improve their finances.

That’s why the biggest lie in personal finance is that you can be rich if you just cut your spending. And the financial media feeds this lie by telling you to stop spending $5 a day on coffee so that you can become a millionaire.

However, these same pundits conveniently forget to mention that this is only possible if you are earning 12% annualized returns (something that is far outside the norm of 8-10% a year).

Even if you could get 12% annualized returns, you would need to earn these returns while holding a 100% stock portfolio without panicking for decades. Easy in theory, but difficult in practice.

This is the same financial media who write stories about how people save money by living in a trailer, making their own dish soap, or reusing their dental floss. Yes, it’s that ridiculous. But what really gets me is how these examples are provided as “proof” of how cutting spending can make you rich.

Just think about how condescending this message is to the typical American family. The author of these posts might as well say, “See, you poor bastard. The reason you aren’t financially free is because you keep buying Tide Pods!”

But most of us can see the trick they are playing on us. We know that they are using exceptional cases and presenting them as some sort of validation of their lie. It’s run-of-the-mill financial pornography.

Despite this, many of us keep reading these articles. I think we keep reading because we want to believe that there is some “secret” to getting rich. But, as I have said before, “there are no secrets.”

Actually, the only “secret” that I know to get rich is to grow your income and invest in income-producing assets. Of course, that is far easier said than done.

The best way to grow your income is to increase your human capital and keep increasing it. Full stop.

And you don’t have to “learn to code” either. There are many other options. For example, I saw this tweet about someone who learned 10 advanced Excel formulas on YouTube and was able to increase her income by $20,000 in just a few nights of studying.

Not everyone can do every job (i.e. everyone can’t code, sell, empathize, etc.), but I believe most people can escape poverty if they put in the work.

Instead of trying to convince everyone that they can be rich, we should be trying to convince everyone that they can be not poor. Now that would be a start to undoing the biggest lie in personal finance.

Honest Early Retirement Articles

I didn’t know how to end this post, so I started to ask myself, “What if the financial media never distorted the truth in their articles?” If so, what would an honest early retirement article headline sound like? How about:

“Wanna retire at 27? Marry rich.”

Or maybe:

“Top Ramen, Is it Your New Retirement Strategy?”

And finally:

“Foregoing Procreation, Living Like a Hermit, and 4 Other Ways to Retire in Your 30s”

Special thanks to Ramp Capital for assisting with these honest retirement headlines and thank YOU for reading!

If you liked this post, consider signing up for my newsletter.

This is post 161 (but based on post #8). See analysis program 008 for the underlying code for these charts: https://github.com/nmaggiulli/of-dollars-and-data

Source: https://ofdollarsanddata.com/the-biggest-lie-in-personal-finance loaded 22.03.2021

Financial Freedom

Introduction to a Financially Savvy Dad

7 Simple Steps to Financial Freedom

The Benefits of Real Estate as an Investment

THE MINIMALIST WAY TO FINANCIAL FREEDOM

Evaluating Assets

Hello OGs,

In previous posts, we have talked a lot about strategies for revenue generation and expense reduction, which fall under the income statement. Today we are flipping over to the other side of the financial statements and begin to strategize around one of the levers that make up our balance sheet. Yes, you guessed it – Assets. Sometimes I feel like I am the only one that gets excited about financial statements. OMG, Guys, Am I weird?

For a thing to be called an asset, it must have three properties; ownership, resource, and economic value. So is the item yours, or do you have control over it? Can it create wealth for you? And can you sell it or exchange it for something of value? This is why a personal car is not an asset because all three questions do not hold true for a car.

Assets can are classified into three buckets; convertibility, physical existence, and usage. But for personal financial analysis, I will touch on just convertibility. Convertibility considers whether an asset is current or fixed. Current assets are assets that are cash or can be converted to cash within twelve months. To read more about the value of current assets click here.

Asset ranked by importance

Disclaimer: this is my preference, does not have to yours

Education

Education is considered an intangible asset, much like intellectual property for companies, in my opinion, this is one of the most valuable assets. I know Elon Musk says BSc. is of little value to him, and who am I to contradict Almighty Elon, but please be informed that the fastest way out of poverty is education – JFK. Pay to learn a new skill, go to school, listen to podcasts, read articles that shape your mind and inspire you to want more. The ROI (return on investment) for this investment is immeasurable as its value sips into the decision-making process of all your other investments opportunities.

Secondly, ensure that the people around you educate themselves too. “The cornerstone of democracy rests on the foundation of an educated electorate” – Thomas Jefferson. This infers that autocracy become the valid option when you are surrounded by illiterates. Since this is not a political piece, what I allude to, is that if you are the only educated person in your circle, they will naturally look to you for leadership and that $hit is draining (pardon my French), ensuring that the people in your circle are educated democratizes their need for just you, and gives you the leeway to focus on you.

Land and property

There is something about owning property that makes me feel connected to mother earth. I can not explain this feeling, but it is invigorating. When I bought my first land, I will find it on google map, zoom out, and say to myself “in this whole world that dot belonged to me”  . Aside from the rush that I describe owning a home cater to the most expensive of the three basic human needs, making it a critical hurdle to financial freedom. Where you rest your head at night must be secured. I am not saying you need to buy a house in downtown Toronto or Lagos where you work, but a starter house in a suburb where things are cheaper may be a good entry point into the real estate market. As your wealth grows, you can graduate or substitute your starter house for a bigger, better more urban house.

. Aside from the rush that I describe owning a home cater to the most expensive of the three basic human needs, making it a critical hurdle to financial freedom. Where you rest your head at night must be secured. I am not saying you need to buy a house in downtown Toronto or Lagos where you work, but a starter house in a suburb where things are cheaper may be a good entry point into the real estate market. As your wealth grows, you can graduate or substitute your starter house for a bigger, better more urban house.

Your Time and Energy

Your time and energy are intangible assets as it is expected that you exchange them for a job that pays or a business and side hustle that hopefully yields a return. Categorizing your time and energy as assets help you evaluate what you spend your time on and what you allow to sap your energy.

Investments

There are a plethora of opportunities to invest in, from shares, bonds, and treasury bills to real estate and start-up opportunities. The expertise to building an investment portfolio is a delicate art that people have died and killed for, but it is possible and important for financial freedom. So fear not my OGs in subsequent posts, we will dive into this investment ocean together.

Cash

Lastly, your cash is an asset that should be allocated and not spent, this mindset is critical to expense optimization.

Source: https://unshakenog.com/2021/02/13/evaluating-assets loaded 21.03.2021