Earlier this week I moderated a session at Inside ETFs called “How to capture outperformance and manage risk.”

Before tackling the challenges of outperformance, I wanted to ask everybody how they think about the amorphous concept of risk. The responses ran the gamut from “the chance of permanent loss of capital” to “the chance of running out of money” and everything in between. Risk is a gargantuan force that can’t be wrestled into one sentence or even a singular idea, but if you’ll allow me to channel my inner Charlie Munger via Tren Griffin for a moment- I think risk is best thought of through the prism of inversion; Risk is the opposite of risk-free. Risk-free however is a bit or a misnomer because risk rules everything around us.

Corey Hoffstein often talks about risk and the two ways it manifests in a portfolio-you can fail quickly and you can fail slowly.

The risk of failing slowly occurs, paradoxically, when an investor does everything they can to insulate themselves from it. What they fail to realize is that absent a high savings rate and a very high income, the avoidance of risk only delays the inevitable fact that risk is ever present. It is these investors who will fail slowly by over allocating into assets like cash and bonds. The stock market provides different risk characteristics and is a more fertile breeding ground for failure in the sense that it gives investors the ability to fail quickly and slowly.

In order to put some meat on this discussion, let’s go to the numbers. Take the risk averse investor who saved 15% of their salary for 40 years starting at age 25. Each year their salary grew with the pace of inflation, with the savings going into one-month treasury bills. At age 66, they turn on the 4% rule- withdrawing 4% of the final amount saved and increasing that each year with the pace of inflation. Their money remains invested in one-month treasury bills (all numbers are net of inflation).

Starting in 1926, saving for 40 years, and then drawing down for 25 years only gives us 28 scenarios to measure. However, I think this is a fair representation of what sort of trouble the risk averse investor will run into. The chart below shows that this person would have run out of money in each of the 28 scenarios. The first column shows the investor who saved 15% of their salary every year from 1926-1966, and then used the 4% rule. On average, the first month spending would be 13% of your final monthly income. This is not enough to sustain oneself in retirement as this pile of money would run out on average after 15 years.

These numbers were made possible by the great Nick Maggiulli

Not only does the risk averse investor run out of money, but this says nothing about the life they’d be able to live in retirement. The chart below shows how much an investor could have spent in their first month of retirement (after saving 15% for 40 years, and then turning on the 4% rule). The average amount withdrawn in the first month for t-bills is $1,750, or 13% of the average final monthly income. Had the investor gone the opposite direction and invested all of their money in the stock market, the average spending in the first month would be $6,000, or 52% of average final monthly income. As you can see in the chart below, stocks reward investors for the risk they took, and allowed for an average withdrawal in the first month that was four times larger than bonds.

The stock market usually pays investors who bear risk, but it doesn’t always. The idea that you can see your wealth cut in half, stay the course, and still not be compensated is an uncomfortable reality that investors should come to grips with. You can eat your vegetables and still die prematurely. Even in the United States, one of the best places to invest over the last hundred years, there have been markets that were rife with risk and absent reward. The chart below shows S&P 500 adjusted for dividends and inflation. The all-time highs are in black, everything else is in red.

Had your retirement started in the throes of the 1973 red for example, you would have run out of money after only 12 years. Had your retirement started any year later than 1974, you were in the clear.

This whole exercise is hypothetical, of course. It assumes that index funds were around before they actually were, that there were no transaction costs, no taxes, and perfect behavior.

The point of this is not to convince you to forego the long-term risk in bonds for the short-term risk in stocks. As I already said, both are risky in their own ways. But rather, I hope this crystallizes one of the most critical concepts in investing; Risk cannot be eliminated. It can be measured and to some extent it can be managed, but it can never be eradicated. If the possibility of failure didn’t exist, there would be no risk. And if there were no risk, there would be no reward. Anyone who tells you differently is ignorant or deliberately lying.

The investor’s job is to figure out what risk means to them, how much they can stomach, and if necessary make changes along the way until their true ability to tolerate it is properly calibrated.

The Biden administration is likely celebrating a better-than-expected jobs report, which showed surging employment and wages. However, for millions of working Americans, being employed doesn’t guarantee a living income.

As scholars interested in the well-being of workers, we believe that the economy runs better when people aren’t forced to choose between paying rent, buying food or getting medicine. Yet too many are compelled to do just that.

Determining just how many workers struggle to make ends meet is a complicated task. A worker’s minimum survival budget can vary considerably based on where the person lives and how many people are in the family.

Take Rochester, New York. It has a cost of living that’s closest to the national average across 509 U.S. metropolitan areas, according to the City Cost of Living Index compiled by the research firm AdvisorSmith.

But in San Francisco, which AdvisorSmith data indicate is the U.S. city with the highest cost of living, affording just the basics costs $47,587, mainly due to significantly higher taxes and rents.

Of course, costs add up quickly for households with more than one person. Two adults in Rochester need over $48,000 a year, while a single parent with one child needs more than $63,000. In San Francisco, a single parent would need to earn $101,000 a year just to scrape by.

So that’s what it takes to survive in today’s America. About $30,000 a year for a single person without dependents in the average city – a little less in some cities, and much, much more for families and anyone who lives in a major city like San Francisco or New York.

But we estimate that at least 27 million U.S. workers don’t earn enough to hit that very low threshold of $30,000, based on the latest occupation wage data from the Bureau of Labor Statistics, a government agency, from May 2020. We believe this is a conservative estimate and that the number of people with jobs who earn less than what’s necessary to afford the necessities of life is likely much higher.

Low-income occupations encompass a wide range of jobs, from bus drivers to cleaners to administrative assistants. However, the majority of those 27 million workers are concentrated in two industries: retail trade and leisure and hospitality. These two industries are among America’s largest employers and pay the lowest average wages.

For example, the median salary for cashiers was $28,850 in early 2020, with 2.5 million of the nation’s 5 million cashiers earning less than that. Or take retail sales. There, 75% of workers – about 1.8 million – were earning less than $27,080 a year.

It’s the same story for leisure and hospitality, the industry that took the hardest hit from the COVID-19 pandemic, hemorrhaging 6 million jobs in April 2020 as much of the U.S. economy shut down. At the time, close to a million waiters and waitresses were earning less than the median income of $23,740.

Of course, millions of those jobs have returned, and wages have been surging this year – though only slightly more than inflation. But that doesn’t change the basic math that roughly 1 in 6 workers is making less than what’s necessary for an adult with no kids to survive.

To us, these figures should cause policymakers to redefine who counts among the “working poor.” A 2021 Bureau of Labor Statistics report estimated that in 2019 about 6.3 million workers earned less than the poverty rate.

But this situation drastically understates the scope of the working poor because the federal poverty line is unrealistically low – only $12,880 for an individual. The official poverty line was created to determine eligibility for Medicaid and other government benefits that support low-income people, not to indicate how much a person needs to actually get by.

Writer James Truslow Adams coined the phrase “The American Dream” in 1931 to describe a society in which he hoped anyone could attain the “fullest stature of which they are innately capable.” That depended on having a good job that paid a living wage.

Unfortunately, for many millions of hard-working Americans, the “better and richer and fuller” life Adams wrote about remains just a dream.

This is the blog post that shows you how to be wealthy enough to retire in ten years.

Here at Mr. Money Mustache, we talk about all sorts of fancy stuff like investment fundamentals, lifestyle changes that save money, entrepreneurial ideas that help you make money, and philosophy that allows you to make these changes a positive thing instead of a sacrifice.

In addition, the Internet presents us with retirement calculators, competing opinions from a million financial advisors and financial doomsayers, unpredictable inflation, and a wide distribution of income and spending patterns between readers.

Because of this torrent of information, people tend to become overwhelmed and say things like,“Yeah, good for you Mr. Money Mustache, but how can I possibly know when I’ll have enough to retire myself, with a completely different lifestyle?”

Well, I have a surprise for you. It turns out that when it boils right down to it, your time to reach retirement depends on only one factor:

Your savings rate, as a percentage of your take-home pay

If you want to break it down just a bit further, your savings rate is determined entirely by these two things:

How much you take home each year

How much you can live on

While the numbers themselves are quite intuitive and easy to figure out, the relationship between these two numbers is a bit surprising.

If you are spending 100% (or more) of your income, you will never be prepared to retire, unless someone else is doing the saving for you (wealthy parents, social security, pension fund, etc.). So your work career will be Infinite.

If you are spending 0% of your income (you live for free somehow), and can maintain this after retirement, you can retire right now. So your working career can be Zero.

In between, there are some very interesting considerations. As soon as you start saving and investing your money, it starts earning money all by itself. Then the earnings on those earnings start earning their own money. It can quickly become a runaway exponential snowball of income.

As soon as this income is enough to pay for your living expenses, while leaving enough of the gains invested each year to keep up with inflation, you are ready to retire.

If you drew this “savings rate” story into a graph, it would not be a straight line, it would be nice curved exponential graph, like this:

Working years vs. Savings Rate (screenshot from networthify.com)

If you save a reasonable percentage of your take-home pay, like 50%, and live on the remaining 50%, you’ll be Ready to Rock (aka “financially independent”) in a reasonable number of years – about 16 according to this chart and a more detailed spreadsheet* I just made for myself to re-create the equation that generated the graph.

So let’s take the graph above and make it even simpler. I’ll make some conservative assumptions for you, and you can just focus on saving the biggest percentage of your take-home pay that you can. The table below will tell you a nice ballpark figure of how many years it will take you to become financially independent.

Assumptions:

You can earn 5% investment returns after inflation during your saving years

You’ll live off of the “4% safe withdrawal rate” after retirement, with some flexibility in your spending during recessions.

You want your ‘Stash to last forever, you’ll only be touching the gains, since this income may be sustaining you for seventy years or so. Just think of this assumption as a nice generous Safety Margin.

Here’s how many years you will have to work for a range of possible savings rates, starting from a net worth of zero:

It’s quite amazing, especially at the less Mustachian end of the spectrum. A middle-class family with a 50k take-home pay who saves 10% of their income ($5k) is actually better than average these days. But unfortunately, “better than average” is still pretty bad, since they are on track for having to work for 51 years.

But simply cutting cable TV and a few lattes would instantly boost their savings to 15%, allowing them to retire 8 years earlier!! Are cable TV and Starbucks worth having two income earners each work an extra eight years for???

it increases the amount of money you have left over to save each month

and it permanently decreases the amount you’ll need every month for the rest of your life

So your lifetime passive income goes up due to having a larger investment nest egg, and it more easily meets your needs, because you’ve developed more skill at living efficiently and thus you need less.

If want to retire within 10 years, the formula is right there in front of you – simply live on 35% of your take-home pay**, which is approximately what I did without even realizing it during my own younger years. The only reason Mustachians will remain a rare breed, is because this article will never appear in USA Today. (Or if it does, people will be too busy complaining about how it can’t be done, rather than figuring out how to do it)

So keep reading, since this blog is all about making financial independence happen!

Now that my blog has gotten some traction among my friends, I have been getting questions like this more often:

“Nick, I just saved up $1,000 and I want to know where I should invest it to get the best return.”

Immediately I think about going into full financial adviser mode to discuss asset allocation, ask about their risk preferences, and understand their goals, but the truth is: their investment returns won’t matter…for now.

With small amounts of money, the total return over the course of a year will be trivial. It would be far better for an individual to focus on saving more money (or growing their income) than worrying about what return they will get in the short run.

For example, let’s say you save up $1,000 and put it into an ETF with an expectation of getting a 10% annual return ($100). You could spend your entire annual return in 1 night going out with friends. Dinner + drinks + transportation and it’s gone.

Now compare this with your future self that has $2 million in a retirement account. A 5% decline in your account value, which is not unreasonable in some years, will result in a $100,000 loss! You couldn’t save that in a year unless you had a very high income or an amazing savings rate.

Therefore, savings have a larger impact on the poor and investments have a larger impact on the rich.

To walk you through my thinking further let’s simulate a 40 year investment life cycle. Let’s assume you make $50,000 a year and save 15% annually (i.e. you save $7,500 each year for 40 years). Additionally, we will assume that you get a 5% annual return on your money with a 9% standard deviation.

This should represent a diverse set of assets (i.e. not as risky as the S&P 500, but not as safe as U.S. bonds). You can imagine the simulation as follows:

In year 1 you save $7,500 and get no investment return on it. In year 2 you get some investment return (random but averages 5%) on the original $7,500 you saved and you save another $7,500. In year 3 you get another random return on the money you had at the end of year 2, and you save another $7,500. This continues onward for 40 years.

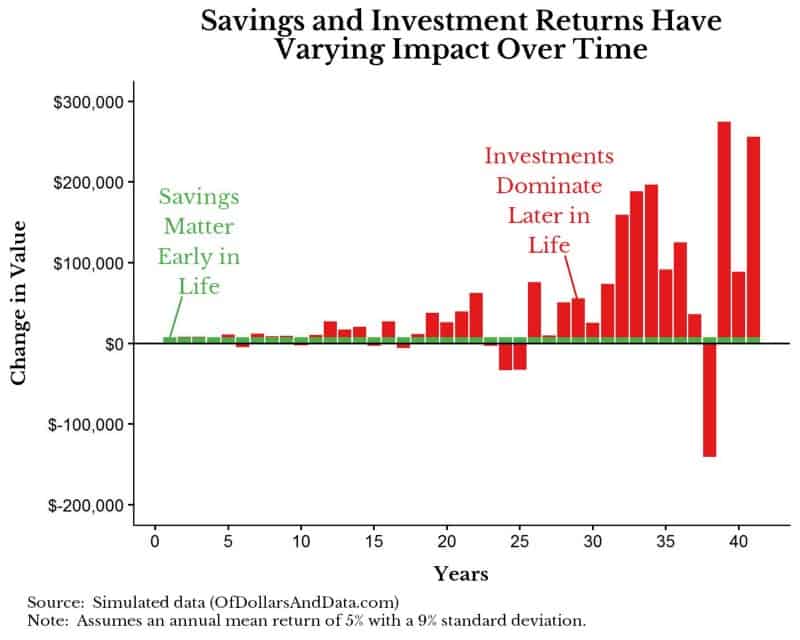

If we were to plot 1 random simulation and show how much was saved in each year (green bar) versus how much was gained/loss from investments in each year (red bar) it could look something like this:

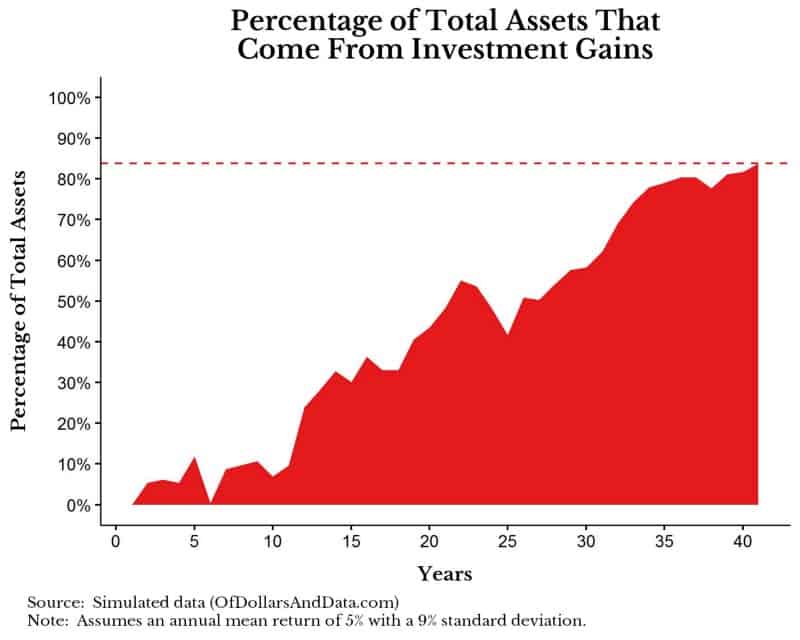

As you can see, the green bars are constant over time since you always save $7,500, but the red bars fluctuate as they represent your random investment returns. Additionally, early in your investment life cycle savings are much larger than investment returns as you would have very little assets. However, as you gain more assets, your gain (or loss) from these assets has a much larger impact on your finances. In particular, by the end of this simulation you would have saved $300,000 ($7,500 * 40 years), but you would have gained ~$1.6 million from investments. This $1.6 million represents 84% of the total assets in year 40 with the $300,000 saved representing the other 16%. If we were to visualize what percentage of your total assets come from investment gains over your life cycle it would look like this (note: the dotted line represents the 84% ending value I discussed above):

As you can see, early on savings are completely building your wealth, however, somewhere near the middle of the life cycle, investment gains become more important.

Regardless of the math and theory behind all of this, the relevant question is:

Should YOU be focusing more on saving or investing?

To answer this, I would ask you to consider the following:

Which is Greater?

Your Total Assets * Your Expected Annual Return

or

Your Expected Annual Savings

If Total Assets * Expected Annual Return > Expected Savings this means your investments are earning you more than you are saving, so you should focus on your investments. However, if you can feasible save more than your assets can earn you in a year, focus on saving.

Practically speaking, if you have $100,000 in assets with an expected return of 5% each year, this means you would expect your investments to earn $5,000 annually (or $100,000 * 0.05). Additionally, if you expect to save $7,500 a year, which is greater than the expected $5,000 from investments, you should focus on saving more money.

Note that this is a spectrum, so it does not imply that you can ignore your investments or your savings rate! However, this should illustrate how important each one is to your financial picture.

Savings is For the Rich Too

Despite the dichotomy I have tried to create between saving and investment income in this post, the truth is that saving is far more important. The ability to save money is highly correlated with financial success because it allows you to live on less and have more disposable income for investing.

You should also consider reading arguably the best personal finance blog post on the internet: Mr. Money Mustache’s Shocking Simple Math Behind Early Retirement. This one post summarizes the entire philosophy behind his blog and it completely revolutionized how I think about saving money.

Regardless of how much you are saving now, you can always change this in the future, so stay positive and get to saving. Thank you for reading!

Is Gold Dead? by Joseph Brown Gold’s performance has been less than stellar over the last year. This has caused many to take their losses and look elsewhere to invest their money. Because of the extreme bearish sentiment surround gold lately, it’s important to keep looking at the numbers to determine whether or not gold […]

Retirement. The Nobel Laureate William Sharpe called it the “nastiest, hardest problem in finance.” And it is. Between deciding how much to save and spend throughout your life, you also have to make guesses about the future.

What will inflation be? How long will I live? What kind of returns will assets provide? And the list goes on.

Despite this complicated process, the financial aspect of retirement planning boils down to three things:

How Much You Save Before Retirement. This is a function of the number of years you decide to work, your income, and your savings.

Asset Allocation. This is a function of how you invest your savings and how much risk you want to take.

How Much You Spend in Retirement. This is a function of your total savings and your future spending, inflation, asset returns, and lifespan.

This might seem daunting, but, if you make just a few simplifying assumptions, you can eliminate most of these choices. For example, you have no control over future asset returns and inflation and limited control over your lifespan. So, if we assume those are out of our hands, then retirement comes down to your savings rate and asset allocation. That’s it.

But, even these two choices are very different. Your savings rate is constantly in flux, being impacted by financial decisions small and large throughout your life.

You can stay in or you can eat out. You can take transit or you take Uber. You can buy or you can rent. All of these choices, and more, will have varying degrees of impact on your retirement success.

However, your asset allocation (i.e. how much risk you take) is one decision that you make that will have the greatest impact on your finances for the least amount of effort.

Because all of those thousands of other financial decisions that you will make across decades will require far more time and energy than deciding what you invest in. Because once you are invested, the compounding should take care of itself.

This is why asset allocation is by far the easiest retirement choice you can make. Let me illustrate this with a simulation. To start, we need to assume the following:

Before Retirement

You work and save money for 40 years (i.e. assume you start saving at 25 and retire at 65).

Your annual income starts at $50,000 and grows with inflation.

You save X% (this will vary) of your income each month and re-invest it in some portfolio.

Your saved money goes into a portfolio consisting of some mix of U.S. Stocks and Bonds (this will vary).

In Retirement

You live for 25 years (i.e. assume you retire at 65 and die at 90).

Your spending is identical to what is was when you were working (constant in real dollars). So if you saved 10% of your income each year, this implies you lived off of 90% of your income. In retirement you would be spending 90% of your final income (indexed to inflation) each year.

Your nest egg is invested in whichever portfolio you invested in before retirement (this will vary).

If we were to start this simulation in 1926 and go through every possible 65 year period (i.e. 40 working years + 25 retirement years) and finish in 2018, we would have 28 different retirement simulations we could test (thanks to Michael Batnick for the idea).

Of course this is simplified, but it will illustrate my main point. First I will walk through an example of one simulation and then present the full results.

Example Walkthrough

Let’s say you started working in 1926 with an income of $50,000 (yes this was a lot of money then, but the starting income is arbitrary for this). By the time you retired in 1966, your real income was identical, but your nominal income would have grown to $89,000 due to inflation.

If you saved 10% a year over this time period, you would have saved a total of ~$240,000. If you had invested in:

100% Bonds you would have $382,000 when you started retirement.

60/40 Stock/Bond you would have $1.6 million when you started retirement.

100% Stocks you would have $3.7 million when you started retirement.

In your first year of retirement you would have spent $80,000. This represents 90% of your final income (i.e. 100% – 10% savings rate). With such spending, your portfolio would run out of money in 5 years with 100% Bonds, in less than 20 years with 60/40 Stock/Bond, and would not run out in 25 years with 100% Stocks.

This example shows the power of asset allocation to have a dramatic impact your chance of financial success in retirement. That one decision made near the beginning of your working life (and stuck to throughout) can have an impact equal to your savings rate with far less effort.

Full Results

Now, let’s do the same simulation for all 28 periods we have available. Below is a chart of the portfolio values at the start of retirement (for the 100% Bond, 60/40 Stock Bond, and 100% Stock portfolios) based on the year you started retirement for each simulation. Note that the leftmost points (i.e. retire in 1966) were covered in the example above:

As you can see, the asset allocation decision can make a large impact on your final portfolio value. The spread you see between the 100% Stock portfolio and the 100% Bond portfolio shrinks over time because of how those assets performed over the years.

The main takeaway is that stocks completely dominated bonds for most of the twentieth century. For example, bonds did quite poorly from the 1940s-1970s, but started to do much better in the 1980s-1990s:

These disparities in returns will also show up in the simulations when looking at the number of years until you run out of money. The plot below has color/shape for each portfolio and the number of years until that portfolio ran out of money based on the retirement start year. If a particular point is at the top of the chart (i.e. 25 years) that means that simulation did not run out of money.

For example, as I highlighted in the “Example Walkthrough” above, if you started retirement in 1966, your portfolio would run out of money in 5 years with 100% Bonds, in less than 20 years with 60/40 Stock/Bond, and would not run out in 25 years with 100% Stocks. This plot is just expanded to show if you retired in 1967, 1968, and so on:

But, we can take this a step further by varying the savings rate over time (from 5% to 20%) and watching how that affects the number of years until the portfolios run out of money:

As you can see, your savings rate will make a big difference in whether you run out of money in retirement, but so does your asset allocation. With a savings rate as low as 13%, the 60/40 portfolio never runs out of money in any of the simulations. Compare this to the 100% Bond portfolio which still runs out of money in some cases with a 20% savings rate!

However, moving your savings rate upward is no easy task. It requires decreased spending or increased income, both things that are not necessarily easy to do. On the flip side, it is also not necessarily easy to bear more risk in your portfolio (i.e. going from 100% Bonds to a 60/40 portfolio), but as Corey Hoffstein so famously repeats:

Risk cannot be destroyed, only transformed.

So, by taking less risk now (i.e. 100% Bonds) you actually take more risk later (i.e. running out of money in retirement). So the question is: Do you want to work your butt off to increase your savings rate, or would you rather take the easy way out and take a little more short-term risk?

The Hardest Choice in Retirement

Despite all of the discussion of the financial choices you need to make for retirement, it’s actually the non-financial aspects of retirement that are the hardest to figure out.

As I have written before, the most important decision you can make in your retirement is how you are going to spend your time, not your money. Many people end up retired and lose their sense of purpose despite having sufficient financial resources.

Though this may seem unrelated, this is also my biggest problem with universal basic income (including sovereign wealth funds). These systems provide money, but they don’t provide any sense of fulfillment for those that receive that money. With the recent increase in deaths of despair in the U.S., figuring out how to give people income and meaning may be one of the most important problems we can try to solve in society.

Though I don’t have an easy answer for how to help you find meaning in your life, I recommend that you create something and give back to a community. Also consider reading How to Retire Happy, Wild, and Free, a retirement book that can help anyone tackle the issue of meaning before and during retirement. It’s the best retirement book I have ever read and it has zero discussion of money.

Lastly, for all of those that have been following along, you may have noticed that my most recent posts have far more data and far fewer stories. I am going back to my roots and hope you stay along for the ride. As always, thank you for reading!

Follow Me: The Wanderer retired from his engineering job at a major Silicon Valley semiconductor company at the age of 33. He now travels the world, seeking out knowledge from other wealthy people, so that he can teach people how to become Financially Independent themselves.

I’m honestly not sure why so many people have such a hard-on for crypto. At this point, we now personally know nearly all the major FIRE bloggers out there and of the ones that successfully reached FIRE, most got there by investing their money in index funds, with some doing it through rental real estate. Nobody got there by investing in crypto.

The biggest reason for this is that cryptocurrency is a speculative investment with no intrinsic value. Even if someone did make millions off Bitcoin, it would be completely unreproducible. “How did you become a millionaire?” “Oh, I bought into Bitcoin 5 years ago.” Great, so how does that help anyone now?

But that doesn’t stop people from pestering us in our inbox every goddamned day. What about crypto? Why aren’t you writing about crypto? Why don’t you own crypto yet?

After the thousandth email, I’m throwing in the towel. OK FINE, INTERNET. You win. You’ve worn me down, OK? I now own freaking crypto. Happy?

This article might sound like one of those oh-so-hilarious “joke” posts that FIRE bloggers love to post on April Fools, but a) it’s not April and b) I’m being serious. I actually do own crypto.

I just refuse to pay for it.

The problem with Bitcoin (or any crypto) is that nobody actually knows what it’s worth. Today it’s worth about $40,000 USD. A year ago it was worth about 50% more. And 5 years ago it was worth a couple hundred bucks. Nobody, not you, not me, and definitely not Elon Musk, knows how much one of these things is worth.

So in that way, Bitcoins are kind of like Beanie Babies. Would I pay money for Beanie Babies? Hell no. But if I could get a box of them for free, why not? It’s no skin off my back, and if some idiot wants to buy them off me later, great!

So that’s the principle of my crypto strategy. Own crypto, but get it for free. How did I do that? Well, keep reading to find out!

The Basics of Blockchain

Despite me coming out publicly against Bitcoin as an investment strategy, I’ve always found cryptocurrencies fascinating from a technical perspective. In my previous life, I was a computer engineer, and I studied cryptography in both undergrad and grad school. Here, using the power of math, I could make any message unreadable at will, and only give the power to unlock that message to whoever I decided. World War II was won by the Allies not because one side’s military was stronger than the other, but because mathematicians like Alan Turing and Polish cryptologist Marian Rejewski out-math’ed the Germans. It was an inspiration to math nerds like me everywhere that they too could change the course of history.

Never in a million years did I think cryptography would take over the financial world the way it did.

So you’d figure that combining two of my loves (math and money) would turn me into a crypto fanboy, right? Well, yes and no. I mean, I’m still fascinated seeing how the crypto space is evolving, but once the Reddit maniacs jumped in, crypto lost most of its appeal to me as a financial investment. In order to buy Bitcoin on an exchange, I’d have to buy from one of them, and who knows what kind of pump-and-dump BS those guys are running on any given day.

So how do I plan on getting Bitcoin if I refuse to buy it on an exchange? Simple: Create them myself.

OK, a brief primer on how Bitcoin works. You’ve undoubtedly heard of the term block-chain by now. Here’s what it means.

When people make transactions using Bitcoin, their transaction details (sender, receiver, amount, etc.) are put into a ledger that tracks everyone’s activity. These ledgers are split into chunks called blocks. These blocks are then chained together to form a chain of blocks, or a block-chain.

The block-chain is not owned by any one entity, government, or financial institution. This quality is why people keep referring to Bitcoin as a decentralized currency. Anyone can download it, host it, or make changes to it.

But what’s keeping me from downloading the block-chain and altering it to give myself a bajillion Bitcoins? Well, I can’t because each block is validated and digitally signed. If I were to alter a transaction on a signed block, it would be immediately obvious that the block had been tampered with (since the signature would no longer be valid), the block, and my fake transaction, would be rejected by the network.

So, you might be wondering, who is doing the validation for each block? That’s where the miners come into play.

Validating a block is a very computationally expensive task. It involves solving a series of complicated math puzzles that takes even very powerful computers a long time to do. Theoretically, anyone with a computer can do it (since the block-chain is de-centralized), but it’s going to take time and computing power. So why would anyone do it?

Simple. If they solve the puzzle, they get rewarded with Bitcoins.

The Bitcoin protocol is designed so that when someone successfully validates a block, new Bitcoins are created and awarded to that person. This is how new Bitcoins are added to the system, and is referred to as “mining.”

That’s how I’m planning to acquire Bitcoins.

Altcoins

Now, as you might expect, generating Bitcoins via mining is a little more complicated than I made it appear. In fact, if you’re a regular person like me without access to custom-built mining hardware, mining Bitcoins no longer works.

This is because the Bitcoin protocol is designed so that mining becomes progressively more difficult the more blocks get added to the block-chain. Why would they do this? Because they knew that computers get faster over time. If mining the first block was the same amount of effort as the bajillionth block, after a while validating each successive block would become faster and faster, which would result in more Bitcoins flooding the market, which would devalue existing Bitcoins and render the whole ecosystem worthless. Gold is valuable because getting the first nugget out of the ground is relatively easy, while getting the last nugget out of the ground is insanely hard. That’s where the inspiration for the block-chain validation protocol came from.

Clever, right?

So here’s the problem. So much attention and computing power has been focused on Bitcoin that the mining difficulty is completely out of reach for average computer owners like you and me. At this point, you need specialized computer equipment plugged into geothermal power sources to profitably mine Bitcoin.

That’s why I’m not going to mine Bitcoin. I’m going to mine an altcoin.

Altcoins are one the many, many cryptocurrencies out there that were created after Bitcoin. You may have heard of Ripple, Ethereum, or (sigh) Dogecoin. All these are altcoins.

The advantage of mining a less popular altcoin is that the difficulty of mining is way lower. Not everyone has jumped on the bandwagon yet, so you have less competition. However, it’s important that whatever altcoin you pick is popular enough that enough people use it, and most importantly, a relatively stable exchange rate exists between that altcoin and Bitcoin. Collecting altcons is worthless if you can’t exchange it.

For that reason, I’ve chosen Monero as my altcoin of choice. In my mind, Monero is what Bitcoin should have been. Bitcoin prides itself on being de-centralized, private, and that no government can decode how you spend your crypto. Except that governments absolutely can decode how you spend your crypto. The block-chain, ironically by nature of being de-centralized, is downloadable by anyone without a court order, and because Bitcoin made the mistake of leaving everyone’s Bitcoin wallet addresses unencrypted, they can trace any transaction ever done in the in Bitcoin ecosystem.

Monero fixes that flaw by encrypting everyone’s wallet addresses in the block-chain (among other security measures like ring-based transactions, which I won’t get into in this article). As a result, I believe Monero fulfills the original intent of Bitcoin, but for now is relatively unpopular, yet still exchangeable for Bitcoin via an exchange like Binance.

How To Mine

To start, I got me some mining software. The most popular Monero miner right now is XMRig. It supports all sorts of hardware, including PCs, Macs, and even Nvidia-based GPU’s (graphics cards).

Next, I needed to create a Monero wallet. After all, if I’m going to mine Monero, where should that Monero go? I got mine from the official Monero site, and installed it on my computer.

Once I had my miner and my wallet, it’s time to start mining, right? Well, not quite. First, you need to join a mining pool.

Mining is a very computationally intensive job. So most people don’t mine themselves since they don’t have a bank of servers at their disposal. Instead, they join mining pools, which are groups of miners that all collectively pool their resources and work together on a block. If that block gets solved, the reward is split among the miners in the pool according to how much work they each put into it.

The most popular Monero mining pool at the moment is MineXMR, so we’re going to join that.

That page directs you to download and install the mining software onto your computer.

Now, in order to perform any actual mining, we need to configure our mining software. Fortunately, there’s a handy wizard to help us do this. So we will start it up by clicking here…

We pick the pool that we want to join in the drop-down…

Then we put in our Monero wallet address, so the miner knows where to send our Monero…

We enable whatever features we have available on our machine…

We set how much we want to donate to the mining pool (1% is standard)…

And finally the wizard spits us out a command to run!

We start up this command on our computer…

And we are off and to the races!

Results

Let me make this clear: mining is not exciting. Your computer may be chugging away at full speed, but all you actually see is a black or white screen with scrolling status messages. Whoop-de-freaking-do.

What’s much more interesting is the dashboard from your mining pool. If you go to your mining pool’s website and enter in your wallet address, you can see the work that your computer is doing and contributing towards the pool’s mining efforts. For nerdy reasons, the computational steps towards validating a block is referred to as a “hash.” Here’s my current MineXMR dashboard.

Right now, I’m mining on FIRECracker’s Macbook Air, my Macbook Air, and my desktop machine. Combined, that’s a respectable 2.3 kHash/s.

And after a couple hours, you can already see Monero rolling in…

There are a couple ways to play this. I could keep accumulating Monero in the hopes that Elon Musk mentions it on another SNL episode and its price skyrockets. I could also exchange it for a more popular crypto like Bitcoin. I could also sell it directly.

I haven’t decided yet. But the important thing is that whatever I end up doing, I did it for free.

So there you have it. I now own cryptocurrency.

But the big question is, how much money will I make with this experiment? Who knows? But I’m sure it will make another interesting article when we find out.

How much do you think this experiment will make? Vote below!

This overhasty and ideologically charged energy policy is clearly reflected above all in the rapidly rising electricity prices. In parallel, the price of gas has quadrupled and German gas storage facilities are at an all-time low.

This is not only what I say, but also what the Wall Street Journal says. This overhasty and ideologically charged energy policy is clearly reflected in the rapidly rising electricity prices. Currently, we consumers pay 0.346 Euros per kWh, which is the highest electricity price in the world. And the trend is still rising, because at the end of 2021, three of the last six nuclear power plants and several coal-fired power plants in Germany will also be shut down as part of the hasty energy turnaround, further exacerbating the overall situation. In parallel, the price of gas has quadrupled and German gas storage facilities are at a low. In addition, the North Stream 2 gas pipeline has been put on hold for the time being and the country is engaged in dangerous verbal sparring with Russia, on which it is largely dependent. So all in one suboptimal.

The head of the Kiel Institute for the World Economy, Prof. Dr. Stefan Kooths, also attests to the failure of politics and that it is lying into its own pocket – all this at our expense. Not only are we endangering the country’s security of supply, but also our competitiveness.

The energy turnaround – a costly wrong decision

The stupidity of governments should never be underestimated”—Helmut Schmidt, former German Chancellor.

The red-green government under Gerhard Schröder decided to phase out nuclear power in 2000. Merkel revised this in 2010 and extended the operating lives of nuclear power plants, thus initially sealing the phase-out. After the Fukushima nuclear power plant in Japan was partially destroyed by an earthquake and a tsunami on March 11, 2011, resulting in a nuclear disaster, the entire world questioned nuclear energy. Many reactors were temporarily shut down. In Germany, too, the question of a nuclear phase-out was now increasingly being asked again.

Two weeks after the accident, state elections were held in my home state of Baden-Württemberg and the topic of nuclear phase-out was, along with Stuttgart 21, the defining issue par excellence. When there was a historic change of government in Baden-Württemberg to a red-green coalition, the Green Party nominated the prime minister and, contrary to all expectations, the CDU did not remain the strongest party in the state, the federal government was in a state of pure panic. In a hasty move, Merkel announced on June 30, 2011, that she was pulling out of the exit from the exit from the exit. Yes, I feel the same as you: I dropped out …

It is already a fact that this was another historic wrong decision by our professional politicians. Criticism is growing louder and louder from all sides – citizens, companies and associations, but even the Federal Audit Office is not hiding behind clear words: The energy turnaround is poorly coordinated and managed, decisive improvements are “unavoidable,” it says in an audit report of the financial control. In the last five years, at least 160 billion euros were spent on this. “If the costs of the energy turnaround continue to rise and its goals continue to be missed, there is a risk of loss of confidence in the ability of government action.”

According to the Institute for Competition Economics at the University of Düsseldorf, the chaotic energy turnaround will cost us citizens 520 billion Euros by 2025 – for now! Economics Minister Peter Altmaier assumes total costs of one trillion Euros by the end of 2030! That’s about 10,000 Euros per German citizen. We, the electricity consumers, are paying for the energy transition chaos:

Added to this are the constantly rising energy costs – already the highest in the world! Electricity prices in France, our nuclear neighbor, are 50 percent cheaper. In return, we have become more dependent on Russian gas – and now hold on: on French electricity (lol).

The energy turnaround is pure actionism, it is completely chaotic, it is expensive for everyone and it is becoming more and more apparent that it is not sustainable as well as even endangering our energy supply: Grid failures are occurring more and more often and the risk of a blackout is increasing. The same can be observed in other countries, and the first measures to counteract this are already taking place. It is doubtful that the “traffic light” government will do a U-turn now. People have become too committed to the new narrative. How could it come to this?

The energetic turn of the times

Worldwide, countries and even central banks have committed to a shift away from fossil fuels and a massive reduction of greenhouse gases in order to stop global warming. To this end, a total of 195 countries agreed at the Paris Climate Agreement of 2015 that global warming should be stopped at below 2 degrees by 2050, and if possible even at 1.5 degrees, measured in each case against the conditions in pre-industrial times. This treaty is to be readjusted every five years. The EU has set itself particularly ambitious targets. Although it has failed in almost every crisis to date, it is now setting out to save the climate. Under EU Commission President Ursula von der Leyen, who was not nominated for election and was not elected, but was appointed nonetheless, the alliance of states wants to reduce net emissions of greenhouse gases to zero with the Green Deal and thus become the first climate-neutral continent. Most recently, the EU has even further tightened its climate targets. It wants to reduce greenhouse gases by 55 percent by 2030 instead of the previous 40 percent (compared to 1990). Money from the 750 billion Euro Corona reconstruction fund will also be used for this purpose. 30 percent of the pot is to be spent to achieve the climate targets.

In order to reduce the CO2 emissions and meet the Paris climate targets by 2050, the world needs clean energy. When we think of clean energy, the first thing that comes to mind is climate-neutral, renewable energy (hydro, wind, solar and geothermal). But even for this, fossil energies and climate-damaging resources are needed and used first. This must be taken into account in the carbon footprint. Photovoltaic systems, for example, have a balanced energy balance after about three years, and wind power plants with an energy payback time (as the technical term goes) after up to a maximum of 2-6 months.

The share of renewable energies in the electricity mix in Germany continues to rise. In the first half of 2020, the share in Germany was a record 55.8 percent. In windy February 2020, it was even 61.8 percent! However, for the year as a whole, the figure was 47 percent. 2021 was extremely wind-poor and the ratio fell back to 43 percent.

However, the disadvantage of alternative energy sources is obvious: The amounts of energy generated with them depend on sunshine and wind conditions and can hardly be stored to meet demand. While the supply is reasonably predictable in the short term, it cannot be controlled at will.

The storage problem

So what to do at night and during a lull – when the sun is not shining and the wind is not blowing? Germany currently has about 30,000 wind turbines. But they do not supply electricity when there is no wind! Even if the number of wind turbines were to double or triple, nothing would change. 90,000 wind turbines with zero wind result in zero electricity yield. The same is true for solar power. No sun, no power!

Unfortunately, buffer capacities are not possible. Again: Renewable energies cannot be produced arbitrarily according to demand at any time of the day or night. Solar power is available when the sun is shining, wind power is not available when there is a lull. How can excess energy be stored temporarily on sunny days or when the wind is blowing hard? A sustainable solution is still missing here. On windy days, Germany has to give away excess capacity to foreign countries or even pay the buyer to take the power, otherwise the grid would collapse. Of course, this is completely irrational. Because when there is a lull, Germany has to buy expensive electricity, often from fossil or nuclear energy sources, from abroad (Poland, the Czech Republic, France) in order to maintain its base load capability. This is not taken into account in the life cycle assessment.

Info box:

Base load capability is the minimum amount of electricity needed to provide a continuous and reliable supply of electricity. The lowest daily load of an electricity grid is used for this purpose. The technologies used to cover the base load are those that can supply the power in question on a constant basis. These are primarily nuclear, coal, gas and oil-fired power plants. Photovoltaic and wind power plants are not base-load capable because of their fluctuating production volumes. The only base-load capable power generation from renewable energies is a hydroelectric power plant – but hydroelectric power is not available everywhere, and the construction of such a power plant involves a gross interference with nature.

Currently, there is only one economical solution to store electricity from sun and wind: pumped storage. However, there is only limited potential for expansion here. For this reason, research is being conducted into alternative storage technologies, such as compressed air storage, power-to-gas technology, in which water is converted into hydrogen by means of electrolysis, and batteries as storage media. However, there is still a considerable need for research and development in all these approaches before they can be used on a larger scale in practice. This may still take years or even decades.

The electric wave

Electrification of the automobile is adding to the demand for electricity, and more and more states are banning the internal combustion engine. Sales are to be banned in order to meet strict climate targets.

The car country Japan also wants to ban all “stinkers” from the road by 2035 and ban the gasoline engine. [1]

The electric car seems to be the answer at the moment when it comes to the mobility of the future. In my opinion, however, the end is still open. Neither the infrastructure nor enough electricity (especially sustainable electricity) is available to move the world electrically. Building and operating an ecologically correct car requires a lot of rare earth, which not only spoil the eco-balance but are also finite and thus more or less quickly depleted. The e-car must be driven for at least eight years until it is climate-neutral. Market leader and pioneer is Elon Musk’s company “Tesla” which is currently worth more on the stock exchange than all other car companies together!

All these developments have also led to a rethinking of the long-established car manufacturers and show the enormous transformation in which one of the most important German key industries and thus also Germany as a business location finds itself. Daimler, Porsche, Opel, Audi and Volkswagen are in the process of completely transforming their product range in a multi-billion dollar effort. VW, for example, wants to switch completely to electric motors by 2025. [2] Whether these efforts will be rewarded with success remains to be seen.

Germany switches off – everyone else switches on

To secure the energy supply and produce emission-free and clean electricity, more and more nuclear power plants are being built and reactivated elsewhere. Worldwide, 54 nuclear power plants are currently under construction. Over 200 more are planned. In addition, more and more countries are reactivating their decommissioned nuclear power plants and/or even building new ones:

Sweden, in an emergency, had to reconnect a nuclear power plant that had already been shut down in order to secure its power supply. [3] Something similar could threaten Germany.

The Netherlands also had to reactivate a nuclear power plant. They are now even planning to build ten new power plants, putting pressure on their neighbor Germany. 4],[5]

A new nuclear power plant is also being built in Great Britain – with German help, by the way. [6]

Coal-fed Poland is planning to build several nuclear power plants for the first time. [7]

Hungary, Romania, the Czech Republic, Bulgaria, and Slovakia want to turn their backs on coal and are relying on nuclear energy, among other things. [8]

Even the oil-rich United Arab Emirates recognizes that oil reserves will run out and inaugurated its first nuclear power plant in August 2020 – also a first for the entire Arab world. [9] Three more will follow in the next few years.

Egypt plans to turn on its first nuclear power plant in 2026.

U.S. President Joe Biden is betting on the small and safe fourth-generation mini-nuclear power plants (Small Modular Reactors SMR.) [10]

In summary, no country in the world will follow Germany on its path to radically destroy its secure energy supply.

The world needs clean energy – the world needs nuclear power

Energy consumption has continued to double in recent decades. A large part still comes from fossil fuels such as gas, coal and oil. About 11 percent currently comes from nuclear power. Due to the demand to become climate-neutral and to generate clean electricity, the need for emission-free alternatives that are also reliable is growing. In parallel, the demand will continue to increase due to digitalization and the electro revolution.

In addition, research has not taken a break, and so the next generation of nuclear power plants will be even more efficient and safer. Even earthquake-stricken Japan has revived shutdown reactors and is planning new nuclear power plants. [11]

The trend to ban fossil fuels and promote pollution-free solutions will bring nuclear power further into the spotlight. After all, nuclear energy is currently the only base-load capable energy source that can perform the balancing act between increasing electricity consumption and emission-free energy production, and uranium is irreplaceable for this purpose.

All this leads to one conclusion: There is currently no way around uranium.

Even if “irradiated” and unworldly experts and politicians have proclaimed the end of nuclear power – they were once again completely wrong. The opposite is true: The nuclear age seems to be just beginning.

Globally, there are 442 reactors in 31 countries (as of February 2021).

Seventeen more countries will join them in the next few years (Egypt, Jordan, Turkey, Indonesia).

The U.S. operates the most nuclear power plants, with 95. China has 49, but is currently building 54 more reactors to satisfy its immense hunger for energy as the world’s workbench. By 2050, the government in China wants to build no less than 230 more nuclear power plants.

Worldwide, 112 nuclear power plants are currently under construction and 330 are planned (as of December 2021). [12]

Fact:

Without nuclear power it is impossible to reach the Paris climate goals! One may be curious, when the German policy of its expensive special way comes off. Until then we, the citizens, have to pay the bill by rising electricity prices and decreasing competitiveness.

{kind=link}

{kind=link}