Breaking: Investment Opportunity

We just received an email from Austrian manufacturer of Saltwater power storage technology Bluesky Energy: https://www.bluesky-energy.eu/en

Participation in the company’s success – profit participation rights

A year ago we offered the opportunity to participate in the company’s success through profit participation rights. The issuance of the green battery 2020 participation rights (round A) was a complete success. The great interest of our partners and customers confirmed our activities. The funding target of 1.5 million euros was achieved.

For all investors from the very beginning, we are pleased to announce that the goals set for the first year have been achieved. The company’s success is even above our forecast. This means that all investors receive an above-planned return on their investment.

New opportunity to participate

Due to the strong demand and the great success of the profit participation rights, we will again offer the opportunity to participate in the company’s success in 2021. With round B for sustainable and safe battery technologies, you have the opportunity to acquire participation rights (nominal value 1,000 euros) again.

Your advantages

Participation in the company’s success

200 euros shopping voucher per profit participation right for those who decide quickly – up to April 15, 2021.

You are committed to the energy transition and set a sustainable example.

The BlueSky Energy participation model and profit participation rights

Sustainable and Safe Battery Technologies – Expansion Financing

Green batteries produced regionally – that was our first issue of profit participation rights in 2020. We are building on the successes of Austrian cell production for saltwater batteries and are issuing profit participation rights for expansion financing and product development.

In terms of development, we are working on connecting our saltwater electricity storage system with our Carbocap product line. The focus is on the development of a hybrid electricity storage system that combines the best of both technological worlds. We also want to grow successfully based on the technologies we have developed. We are pushing international sales and distribution as well as developing strategic future markets such as Africa.

Since we as a private company want to remain independent and do not want any dependencies on investment funds, the global capital market system or large corporations, we have decided to invite you to establish financing with us with profit participation rights.

The key data

The salt water battery is the most environmentally friendly and safest battery. We manufacture in Austria.

We are working on a technological combination (= hybrid storage) with our newly developed Carbocap storage and salt water batteries

Our know-how and our goal: The expansion of our position as the only marketable provider of complete power storage systems with clean and safe battery technologies.

Your opportunity: participation in an economically successful company

Subscription period from March 15, 2021 to June 30, 2021

The goal

Building on our successful project to establish saltwater battery cell production in Austria and the successful development of the complementary Carbocap battery technology, we want to take further expansion steps.

In terms of development, we are working on successfully and cost-effectively marrying both technologies (salt water, Carbocap) into a hybrid electricity storage system. With the great chance to pick the cherry on the cake between the two technologies, for the benefit of the customers and as a clear unique selling point on the market.

On the other hand, we want to grow successfully based on the technologies we have developed. Promote international sales and distribution, as well as actively address future strategic markets such as Africa with a targeted product portfolio and organization. We want to further expand our pioneering role in the area of environmentally friendly and safe battery technology. We will continue to develop our technology solutions in order to be able to sell improved and more cost-effective products.

“We look forward to starting a future with clean and safe batteries together.” Thomas Krausse and Ing.Helmut Mayer

We invite you!

Go the way with us. With the participation rights (round B) for sustainable and safe battery technologies, you can invest in a successful company with promising technology with a deposit of 1,000 euros or more (issue period from March 15 to June 30, 2021).

We offer a total of 2,000 profit participation rights with a nominal value of 1,000 euros each. Several profit participation rights can be given per person.

The remuneration depends on the company’s profit.

Using the example of the 2019 profit of 200,000 euros, the interest rate is 0.5% p.a. of the invested capital. For 2024 we are planning an annual profit of more than 6 million euros. The interest rate would then be 15.7 percent p.a.

Additional bonus: We offer an additional benefit for the first 500 participation rights subscribed. In addition to the agreed interest gain, you have the option of purchasing our products with a one-time special discount of 200 euros per profit participation right. We offer this additional special discount for the first 500 profit participation rights, but no later than April 15, 2021.

The idea – profit participation rights

With the help of convinced partners to a balanced financing base.

Invest your money in a forward-looking company instead of taking it to the bank where you can hardly get any interest.

Solid development since 2014

We have seen good growth since our foundation in 2014.

BlueSky Energy is a private, Austrian GmbH with branches in the USA and Belgium. We want to be independent of large corporations in the future as well.

We’re not a start-up that raises money from individuals before value is even created. We have had a positive balance sheet since 2019 and will generate a profit for the year even in the challenging year 2020.

In hundreds of electricity storage projects worldwide, we have proven that our safe and sustainable electricity storage solutions are a high-quality alternative to conventional technologies.

Energy for new projects

Our goal is to promote the established market positioning as the only marketable provider of complete power storage systems with clean and safe battery technology worldwide. The first step is to set up a regional battery cell production facility.

With the establishment of the local saltwater battery cell production in Austria, which will go into operation in Q2 2021, and the development of our complementary Carbocap technology for the products VIGOS and Cel-3050, we have achieved two major milestones.

We are now working on marrying both technologies in a hybrid power storage system, successfully selling our products internationally and further developing both technologies in a qualitative and cost-effective manner.

Profit participation rights – a new way to participate

BlueSky Energy Entwicklungs- und ProduktionsGmbH has been proving since 2014 that sustainable and safe batteries are in demand on the market. The distribution of our electricity storage products is organized in a lean and effective manner.

We work with freelance sales representatives and employed sales staff. The distribution channel is structured in two stages and we sell our products to certified partners. These are electrical or photovoltaic installers who have completed training on our electricity storage products. This guarantees a professional installation on site at the end customer.

The overwhelming demand (order backlog as of December 31, 2020: 5.1 million euros), numerous projects and orders worldwide confirm us.

BlueSky Energy participation rights for sustainable and safe battery technologies

With the participation rights (round B) for sustainable and safe battery technologies from BlueSky Energy, you can invest in a successful company with promising technology with a deposit of 1,000 euros or more. The issue period from March 15, 2021 to June 30, 2021.

We offer a total of 2,000 profit participation rights with a nominal value of 1,000 euros each. Several profit participation rights can be given per person. We can surrender further profit participation rights over an amount of 5,000 euros if you declare in writing on a sheet provided by us that you are investing a maximum of twice your average monthly net income (calculated over twelve months) or that you are investing a maximum of 10% of your financial assets .

A profit participation right makes it possible to participate in the profits of a company, but without getting voting rights or a say in the company. In contrast to loans, profit participation rights enable higher interest rates if the business trend is positive. However, in the event of a poor corporate development, no return is guaranteed; it is qualified subordinated capital.

Sources: email from Bluesky Energy dated 26.03.2021, translated from the German original https://www.bluesky-energy.eu/beteiligungsmodell loaded 26.03.2021

How Much Do I Need for Retirement?

The 4% Rule: The Easy Answer to “How Much Do I Need for Retirement?”

In the world of early retirees, we have a concept that goes by names like “The 4% rule”, or “The 4% Safe Withdrawal Rate”, or simply “The SWR.”

As with all things financial, it’s the subject of plenty of controversy, and we’ll get to that (and then punch it flat) later. But for now, for those new to the concept, let’s define the Safe Withdrawal Rate:The Safe Withdrawal Rate is the maximum rate at which you can spend your retirement savings, such that you don’t run out in your lifetime.

That sounds nice and simple, but many people consider it an unpredictable thing to nail down.

After all, you don’t know what sort of rollercoaster rides the economy will take your retirement savings on, and you also don’t know what rate of inflation will persist through your lifetime. Will a box of eggs cost $6.00 a dozen when you’re 65, or will it be closer to $60? So how can we possibly know how much money we will need to live on in retirement?

The answers you get to this question vary widely.

Financial beginners (about 95% of the population) tend to randomly just throw out a number between 5-100 million dollars.

Financial advisers who aren’t Mustachians will tell you that it depends on your pre-retirement income, (with the implicit assumption that you are spending most of what you earn) and the end answer will be somewhere between 2 and 10 million.

Financial Independence enthusiasts will have the closest-to-correct answer: Take your annual spending, and multiply it by somewhere between 20 and 30. That’s your retirement number.

If you use the number 25, you’re implicitly using a 4% Safe Withdrawal Rate, which is my own personal favorite number.

So where does this magic number come from?

At the most basic level, you can think of it like this: imagine you have your ‘stash of retirement savings invested in stocks or other assets. They pay dividends and appreciate in price at a total rate of 7% per year, before inflation. Inflation eats 3% on average, leaving you with 4% to spend reliably, forever.

I can already hear a chorus of whines and rattling keyboards starting up, so let’s qualify that statement. I admit it: that is the idealized and simplified version.

In reality, stocks go up and down every year, and so does inflation. Over a long multi-decade period like the gigantic retirement you and I will be enjoying, enormous things have happened in the past. The Great Depression. The World Wars, Vietnam, and the Cold War. The abandonment of the gold standard for US currency and years of 10%+ inflation and 20%+ interest rates. More recently, the great financial crash and a slicing in half of of real estate and stock values.

If you happened to retire in 1921 on a mostly-stock nest egg, you would have experienced an enormous stock run-up for the first eight years of your retirement. You’d be so rich by the time the 1929 crash and the Great Depression hit, that you’d barely notice the trouble in the streets from your rosewood-paneled tea room.

On the other hand, if you retired in early 2000 while holding stocks, you saw an immediate and huge drop in your savings along with low dividend yields – and your ‘stash may be have had some scary times in the early days, and again around 2009. Would you still have any money left today?

In other words – the sequencing of booms and crashes matters. Ideally, you want to reach your magic retirement number in a time of nice, reasonable stock prices, just before the start of another long boom so that your retirement starts off on a good foot. But you can’t predict these things in advance. So again, how do we find the right answer?

Luckily, various Early Retirement Ninjas have done the work for us. They analyzed what would have happened for a hypothetical person who spent 30 years in retirement between the years 1925-1955. then 1926-1956, 1927-1957, and so on.

They gave this imaginary retiree a mixture of 50% stocks and 50% 5-year US government bonds, a fairly sensible asset allocation. Then they forced the retiree to spend an ever-increasing amount of his portfolio each year, starting with an initial percentage, then indexed automatically to inflation as defined by the Consumer Price Index (CPI).

This simple but important series of calculations was called the Trinity Study, and since then it has been updated, tweaked, and reported on, and it’s still the subject of lots of debate today. Wade Pfau is one reasonable voice in the industry, and he created the following useful chart showing what the maximum safe withdrawal rate would have been for various retirement years:

As you can see, the 4% value is actually somewhat of a worst-case scenario in the 65 year period covered in the study. In many years, retirees could have spent 5% or more of their savings each year, and still ended up with a growing surplus.

This brings me to a critical point: this study defines “success” as not going broke during a 30-year test period. To people like you and me who will enjoy 60-year retirements, that would not be successful – we want our money to last much longer than 30 years.

Luckily, the math in this case is pretty interesting: there is very little difference between a 30-year period, and an infinite year period, when determining how long your money will last. It’s much like a 30-year mortgage, where almost all of your payment is interest. Drop your payment by just $199 per month, and suddenly you’ve got a thousand-year mortgage that will literally take you 1000 years to pay off. Increase the payment by a few hundred, and you have a fifteen year payoff!

In other words, above 30 years, the length of your retirement barely affects the safe withdrawal rate calculations.

So far, we’re liking the 4% rule quite a bit, right? But yet whenever I mention it, I get complaints. Let’s review a few of them:

- The trinity study is based on a prosperity anomaly: the United States during its boom years. You can’t project good times like that into the future, because we’re just about to enter the Doom Years!

- Economic growth and stock appreciation was all based on cheap fossil fuels. How will this all look after Peak Oil hits us!?

- You can’t take a one-size-fits-all rule and apply it to something as varied as an economy and an individual’s life! My health care costs could go up! Hyperinflation could strike!

- Even at a 4% withdrawal rate, there’s still a chance of portfolio failure. That means I’ll be flat broke and out on the street in my old age. I recommend doubling your savings, and going for a 2% SWR instead because there’s never been a failure in that scenario!

- This is all wrong! Waaah, waaah!

That’s all well and good. While there are solid economic analyses that I believe can out-argue the points above, I’m not patient or clever enough to re-create them here. Pessimists are free to enjoy their pessimism and even write about it on their own blogs.

Instead of debating unprovable points like those above, we can completely squash them with our own much more powerful list of points:

The trinity study assumes a retiree will:

- never earn any more money through part-time work or self-employment projects

- never collect a single dollar from social security or any other pension plan

- never adjust spending to account for economic reality like a huge recession

- never substitute goods to compensate for inflation or price fluctuation (vacation in a closer place one year during an oil price spike, or switch to almond milk in the event of a dairy milk embargo).

- never collect any inheritance from the passing of parents or other family members

- and never do what most old people tend to do according to studies – spend less as they age

In short, they are assuming a bunch of drooling Complete Antimustachians. You and I are Mustachians, meaning we have far more flexibility in our lifestyles. In short, we have designed a Safety Margin into our lives that is wider than the average person’s entire retirement plan.

So now that we’re feeling good about the 4% rule again, let’s bring the point home:

Far from being a risky proposition, planning for 4% Safe Withdrawal rate is actually the most conservative method of retirement saving I could possibly recommend.

To apply it in real life, just take your annual spending level, and multiply it by 25. That’s how much you need to retire, at the most. A $25,000 spender like me needs $625,000. I’ve got more than that, plus various safety margins in the lifestyle, so all is good.

Without undue risk, and as long as you have skills that can be used to earn money eventually in the future (hint: you do), I can even advocate an SWR of 5%. In other words, get your expenses down to $25k, and you can quit your job on $500k or less. Then you can use the methods described in First Retire, then Get Rich to gradually increase your safety margin (and effectively decrease your withdrawal rate) as you age.

So there’s no need to debate. 4% is a perfectly good answer, which means 25 times your annual expenses is a perfectly good goal to save for. Along the way, you might find your annual expenses melting away, which makes things ever-more-attainable (as shown in the shockingly simple math behind early retirement post). But worry, you must not.

And if you’re ready to play with the numbers even further, check out the FIREcalc website. It’s basically like owning your own Trinity Study machine, except you can tweak variables (look at the tabs at the top of the page). In the link provided, I used this data:

- 500,000 portfolio

- 25,000 annual spending (5% withdrawal rate).

All alone, a plan like that over 60 years of retirement only has a 45% success rate, historically speaking.

But if you make adjustments which include:

- $8,000 per year of social security starting about 25 years from now

- “Bernicke’s Reality Retirement plan” of dropping spending slightly with age

- Just $3,000 per year in fooling-around income

You’re already at an over 90% success rate. Another hundred or two dollars per month and you have a 100% chance of success, even without invoking many of my other bullet points above.

So that, at last is the long-awaited Safe Withdrawal Rate article.

In the hands of financial infants, the rule is dangerous and scary. But in the hands of Mustachians, nothing is scary. Planning for a 4% withdrawal rate is a shiny, bulletproof limousine of a retirement plan and you can ride it all the way to the party at Mr. Money Mustache’s house.

Source: https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement loaded 22.03.2021

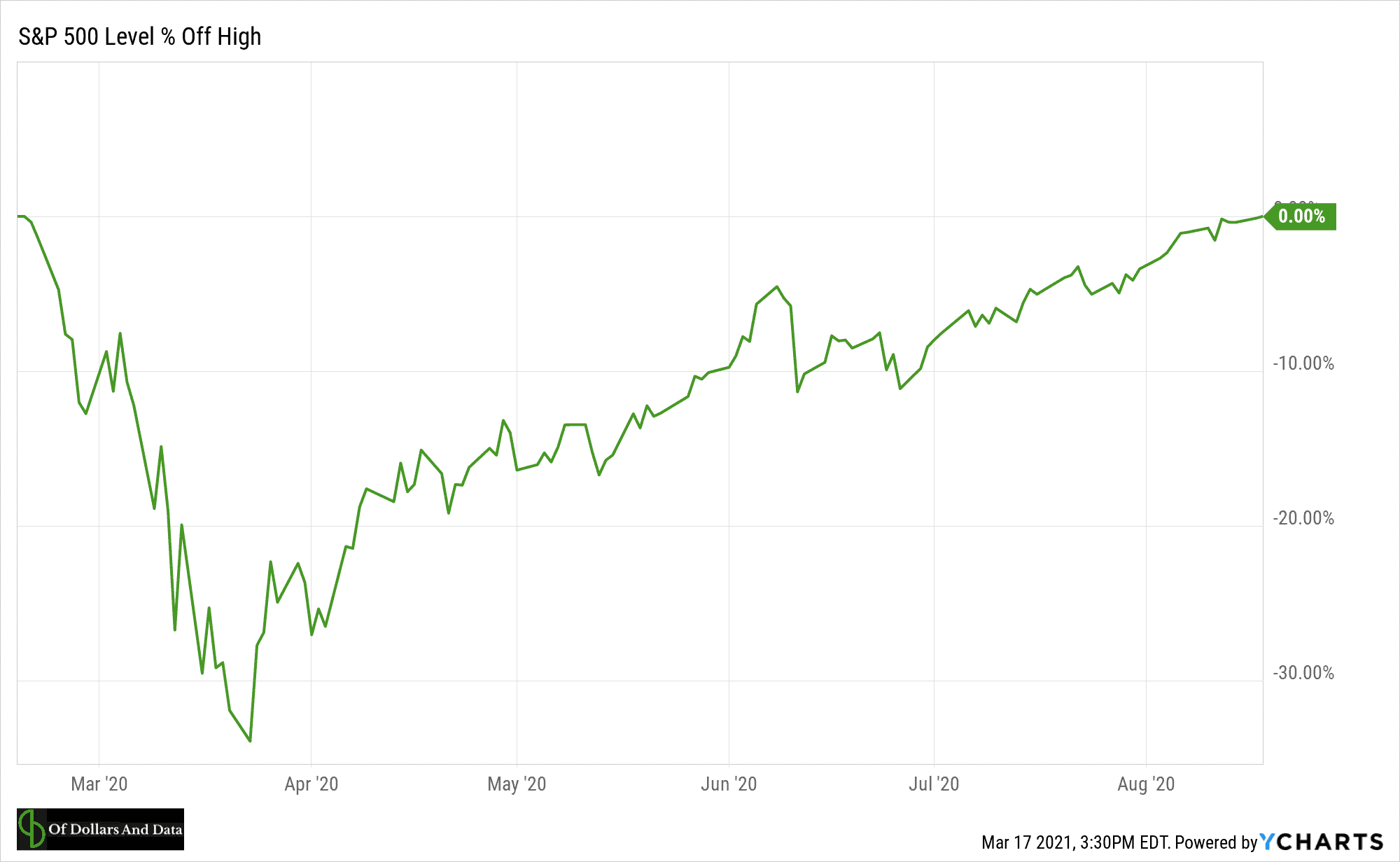

Started From the Bottom

Posted March 23, 2021 by Nick Maggiulli

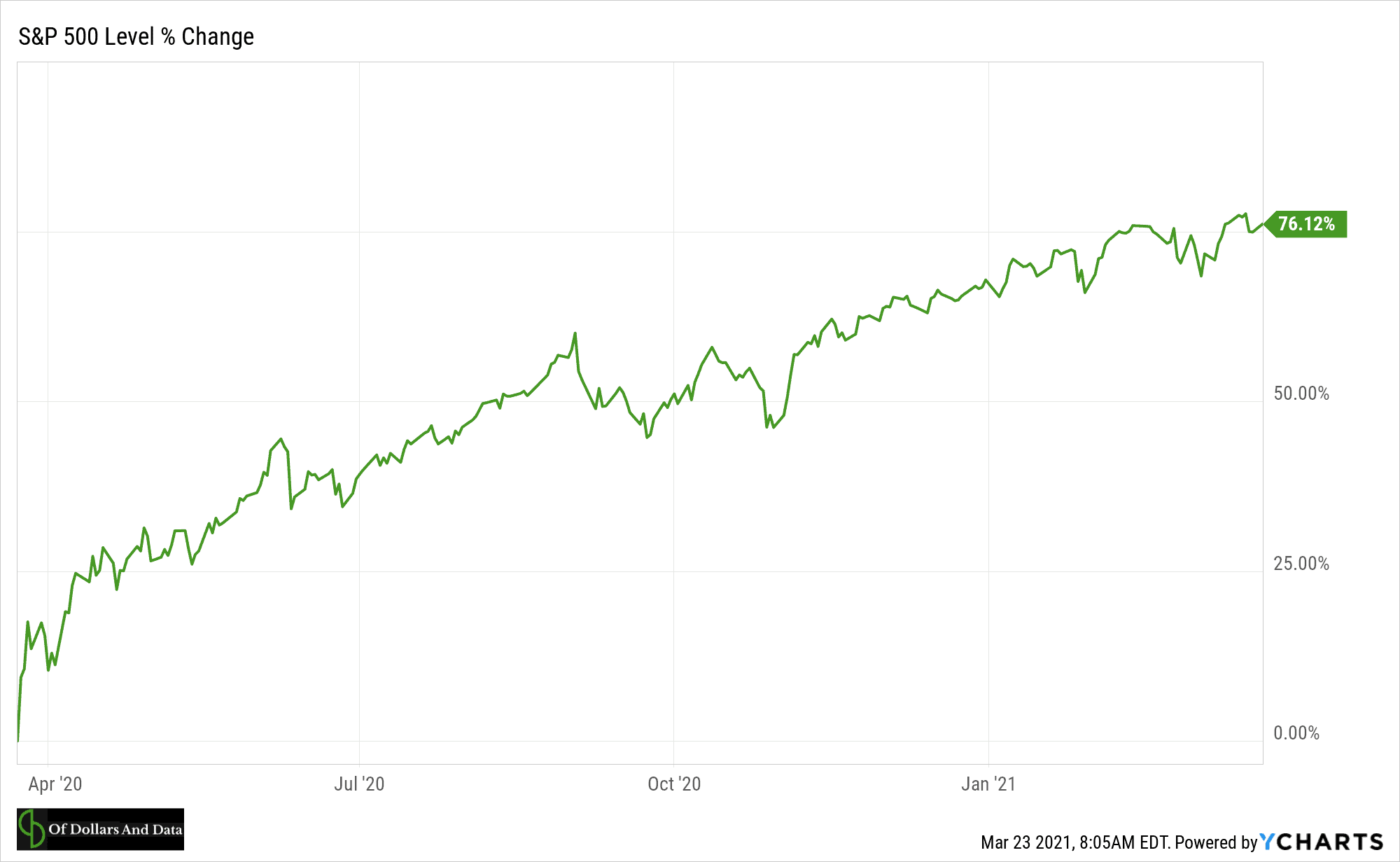

It’s been one year since the market bottomed during the coronavirus crash on March 23, 2020. I remember that day well because it was the same day I published this blog post explaining why it can be so lucrative to buy during a crisis. Yes, publishing this on the day of the bottom was pure luck, but my bullish stance wasn’t.

Since then I have received comments from many readers about how much this post helped them when times looked the toughest. As a result, I want to revisit the prior year and some of the lessons I have learned since the bottom.

We May Never See a Better 1-Year Rally

If you had bought the S&P 500 on March 23, 2020, you would now be up by 76% (excluding dividends):https://tpc.googlesyndication.com/safeframe/1-0-38/html/container.html

{kind=link}

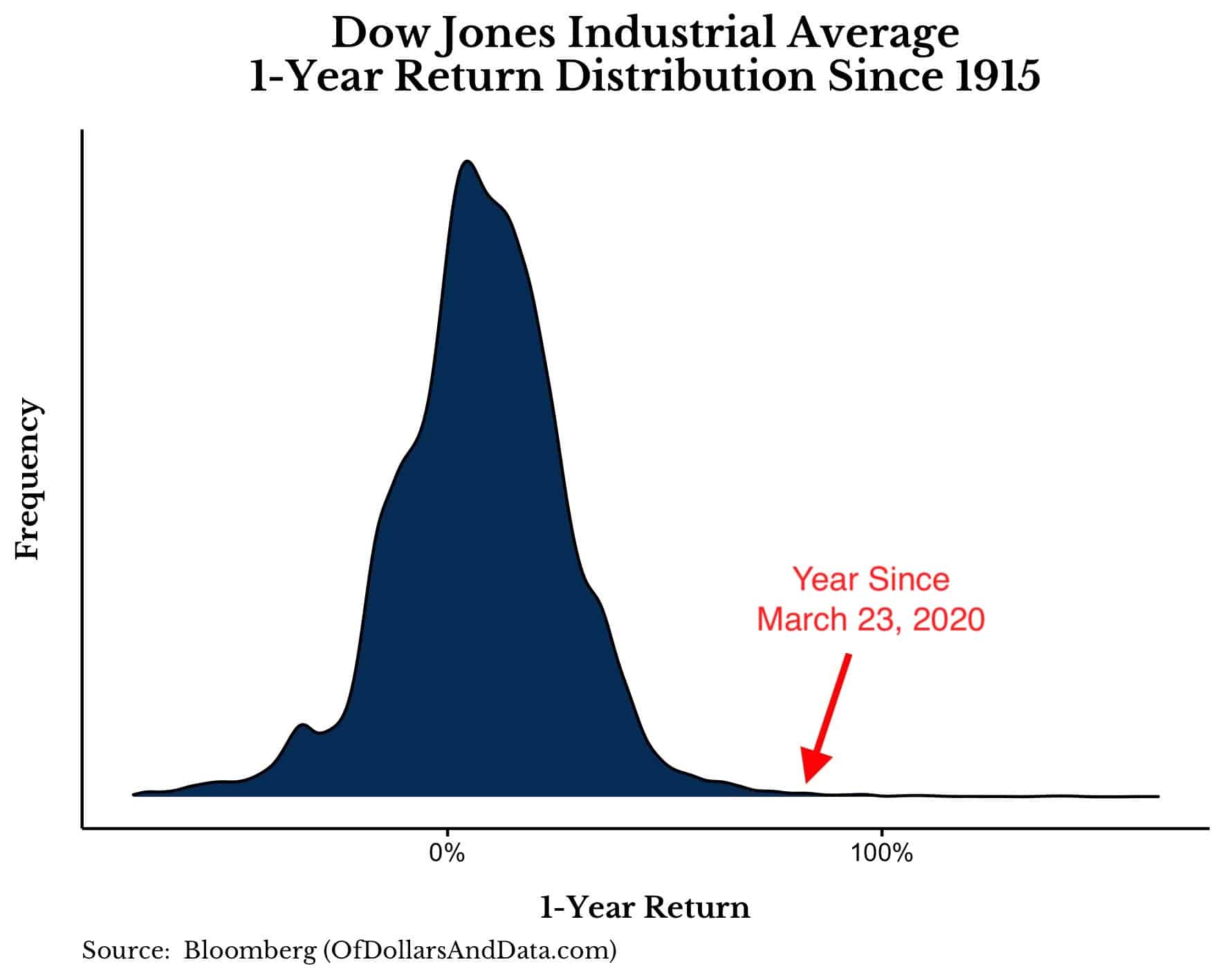

76% in a single year! Returns like that don’t come often. In fact, if you look at the distribution of 1-year returns for the Dow since 1915, you will see how much of an outlier the prior year has been:

{kind=link}

Since 1915 there have only been two periods that had higher returns over the prior year:https://tpc.googlesyndication.com/safeframe/1-0-38/html/container.html

- July 1933

- March 1934

Both of these periods occurred during the recovery from The Great Depression.

Therefore, without a doubt March 23, 2020 was a generational buying opportunity. In fact, it may have been a lifetime buying opportunity. If these kinds of crashes (and their subsequent recoveries) continue to be as rare as they have been throughout history, then we may not see a higher 1-year return in U.S. stocks for the rest of our lives.

It seems hard to believe, but we just lived through the stock market equivalent of Halley’s comet. However, unlike Halley’s comet, whose future path is known, we have no idea when another market rally of this magnitude will occur.

It’s Easy to Feel Like an Investment Genius Right Now

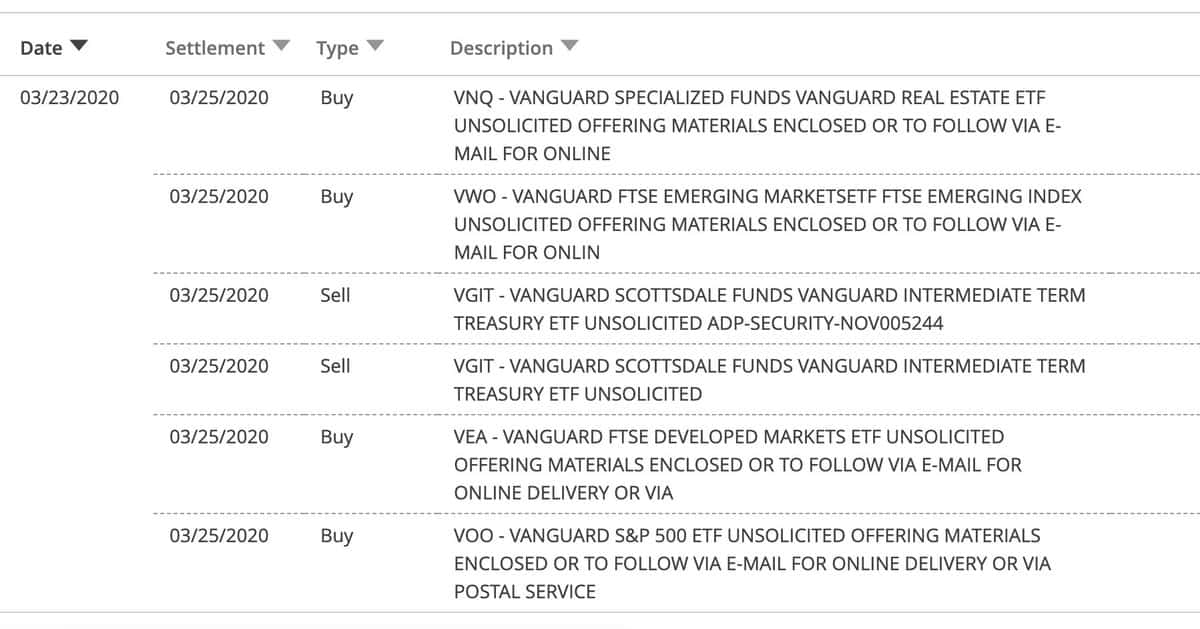

Due to the strong returns over the prior year, it’s very easy to feel like an investment genius right now. As Michael Batnick recently highlighted, regardless of size or valuation decile, anyone who bought in March 2020 is up between 60%-150% as of today. With such high returns, almost everyone can feel like they saw it coming. But, I promise you that this is mostly hindsight bias.

How do I know? Because even I called (and traded) the bottom. In addition to my bullish post on March 23, 2020, I also sold all of the bonds in my retirement accounts and rebalanced into equities/REITs on the same day. I have trade confirms to prove it too:https://8fd564891193bef04a18dab3d5aaa9d6.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

{kind=link}

Should I sell a course on market timing? How about a book on predicting market sentiment? No thanks.

Why not capitalize on my tactical skills? Because I know they don’t exist. Trading the bottom was 99% luck. Anyone who says differently is lying to themselves. Because, at the time, no one knew what would come next. On March 24, 2020, the market could’ve easily continued its downward trajectory. But…it didn’t.

Looking back now it’s tempting to see yourself as an investment guru, but the real guru would recognize the difference between their abilities and a rising tide lifting all boats.

Most People Got the Recovery Wrong

If you needed more proof that most people have no idea what comes next, consider how well they predicted the recovery.

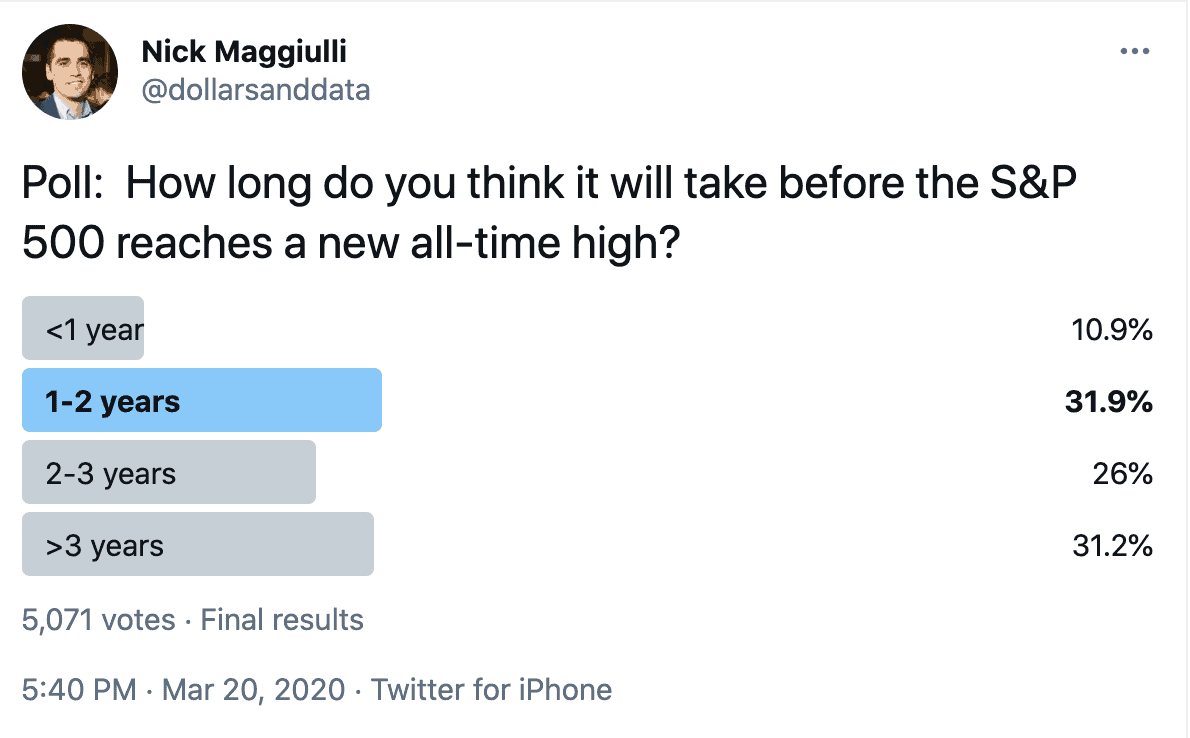

On March 20, 2020 (a few days before the bottom), I asked Twitter how long it would take for the S&P 500 to make new all-time highs. The majority voted for a recovery time of greater than two years:

{kind=link}

As we all know now, they were wrong. Very wrong. In fact, only 11% of my Twitter audience voted for the correct answer “<1 year”. Unfortunately, I wasn’t a part of this 11%.

Despite my bullishness at the time, I thought that the recovery would take at least a year (even in the best case scenario). But I wasn’t even close. As a surprise to almost everyone, within six months of the March 23 bottom we were hitting all-time highs once again:

{kind=link}

The quickness of the recovery popularized the talking point “the stock market is not the economy.” And since then, this idea has come to dominate the financial conversation. Unfortunately, the speedy recovery also seems to have given fuel to the “everything is in a bubble” theory as well.

Regardless of what you believe, the past twelve months have illustrated that predicting the future is always much harder than it seems.

The Triumph of the Optimists

Of all the things that I will take with me from the last year, it’s that the optimists usually win. Yes, there are many things wrong with the world, but the arc of history continues to bend toward progress and a better future for humanity. It’s easy to forget this when things look the bleakest, but it’s true.

For example, a few months before the bottom in March 2020, scientists came up with the COVID-19 vaccine in a matter of days. It took them just a few days to create a vaccine that is now being distributed around the world and saving millions of lives.

How can you be pessimistic in a world like this? How can you be bearish when we have gone through far worse and bounced back time and time again? The Oracle of Omaha said it best:

In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.

So, what’s it gonna be? Do you want to focus on the negative and run at the first sign of panic? Or do you want to focus on the long-term trend and join the optimists?

Of course, no one knows when the next bottom will come or what will cause it, but I’m willing to bet that this future bottom will be higher than the last one. Happy investing and thank you for reading!

Source: https://ofdollarsanddata.com/started-from-the-bottom loaded 25.03.2021

10 Lessons I Learned From Quitting Instagram

How to Nest Pages in WordPress

Published 25.03.2021 by Schmitt Trading Ltd

In WordPress, there are two ways of publishing information: blog posts and pages.

Pages are meant to stay as they are and where they are, while blog posts continuously move in a flow of new blog posts.

To learn more about how to build an internet archive, read my blog post How to Create an Internet Archive.

If you published with WordPress before and missed the latest changes, here is how to nest pages in WordPress:

To create a new page, click My Site, Pages:

Click Add New.

Pick a pre-defined layout or start with a blank page:

Add a title and start writing:

When you enter your title (e.g. Business Ideas), WordPress automatically fills the permanent link URL slug:

In the old days, you only had to add a parent page to nest your new page as child:

Scroll down to Page Attributes and select the Parent Page from the list:

Publish your page. Done.

Nowadays, with the new block style, you need to take some more steps to nest a child page below a parent page:

Go back to My Site.

Scroll down the left menu bar and click Appearance, Customize:

Click the Edit icon in the Primary Menu:

The Primary Menu opens:

Scroll down and click Add Items:

Open the folder pages and click the desired page to be nested:

Grab the newly added page with the Select icon and move it to the desired place in your menu:

When you are done, click Save Changes:

The Lending Club Experiment

Can you Really earn 10% Annual Returns These Days!?!

Find out at the MMM Lending Club Experiment Headquarters.

In September of 2012, I started making a series of investments in the relatively new field of peer-to-peer lending, choosing a company called Lending Club as the destination. The goal is to see if the higher returns really are attainable without luck or amazing analytical powers. It all started with these two articles:

The Lending Club Experiment – Four Months Later

This page will document my ongoing results, with results updated periodically (especially after significant economic events). Since you’re probably a “Show me the Money” type of person, let’s jump right to the results, then do a little analysis afterwards:

| Date | Balance | Interest Received | Annualized Return | Late 16-30 Days | Late 31-120 Days | Default or Charged Off |

|---|---|---|---|---|---|---|

| Sept 24, 2012 | $10,000 | $0 | ~13% (projected rate after defaults) | 0 | 0 | 0 |

| Feb. 3, 2013 | $21,060 (note: I added $10k plus received $300 referral bonus) | $579.53 | 20.12% | $48.46 | $122.77 | 0 |

| March 21, 2013 | $21,516.29 | $1,054.94 | 19.84% | $24.03 | $308.90 | 0 |

| May 13, 2013 | $21,992.96 | $1554.15 | 18.53% | $0 | $214.00 | $73.00 |

| July 13, 2013 | $32,549.52 (note: I manually added $10k of extra principal over the last month) | $2,174.54 | 18.30% | $114 | $302 | $121 |

| October 8, 2013 | $32,478.25 (note: I withdrew $1100 last month for another investment – transfer to bank worked well, about 2 business days) | $3,368.00 | 17.02% | $47 | $518 | $353 |

| December 17, 2013 | $32,959.53 | $4,403.73 | 16.50% | $233 | $613 | $526 |

| February 28, 2014 | $33,568.54 | $5,458.52 | 15.37% | $43 | $802 | $957 |

| May 6, 2014 | $34,131.67 | $6478.23 | 14.48% | $121 | $848 | $1361 |

| July 31, 2014 | $34,837.59 | $7866.18 | 13.52% | $141 | $819 | $2075 |

| Sept 30, 2014 | $35,400.36 | $8,884.05 | 13.34% | $244 | $809 | $2523 |

| Nov. 30, 2014 | $35,968.71 | $9898.79 | 12.97% | $82 | $925 | $3010 |

| Jan 31, 2015 | $36,322.07 | $10,938.74 | 12.28% | $287 | $850 | $3704 |

| April 30, 2015 | $37,298.76 | $12,513.94 | 12.22% | $108 | $933 | $4309 |

| June 30, 2015 | $37,895.42 | $13,611.74 | 12.07% | $80 | $1155 | $4901 |

| August 10, 2015 | $38,255.98 | $14,339.15 | 11.98% | $159 | $1105 | $5355 |

| Sept 30, 2015 | $38,845.55 | $15,224.57 | 11.99% | $293 | $1062 | $5859 |

| Nov. 7, 2015 | $38,998.25 | $15,992.22 | 11.63% | $246 | $1211 | $6214 |

| Jan. 18, 2016 | $39,593.51 | $17,305.76 | 11.66% | $202 | $1202 | $7056 |

| April 17, 2016 | $40,546.48 | $19,160.85 | 11.32% | $318 | $1213 | $8077 |

| May 20, 2016 | $40,927.88 | $19,879.50 | 11.25% | $356 | $1358 | $8355 |

| August 28, 2016 | $41,962.57 | $21,977.20 | 10.99% | $728 | $2049 | $9753 |

| October 19, 2016 | $41,601.03 | $23,030.91 | 10.18% | $668 | $2099 | $10,991 |

| January 2, 2017 | $41,650.97 | $24,665.74 | 9.56% | $499 | $2205 | $12,742 |

| April 16, 2017 | $41,574.38 | $26,880.31 | 8.74% | $641 | $2074 | $15,061 |

| October 24, 2017 | $41,301 | $29835 | 7.72% | $208 | $1499 | $18,323 |

| June 29, 2018 | $40,716 | no longer shown | 6.82% | $92 | $527 | $21,554 |

Key Update:

- In October 2016, I saw my account balance drop for the first time. The balance went down $300, when statistically it should be up about $600 over that time period. With my balance diversified across over 2500 notes, this should be a highly unlikely event.

- By the end of December 2016, I noticed the problem remained – 3 more months had passed, and the balance had barely changed. The default rate seems to have increased enough to eat up most of the incoming interest, which means this is no longer so much as an investment, as a way of redistributing interest payments from responsible borrowers to irresponsible ones.

- Here in October 2017, the balance is still drifting downwards. It has now been over a year of flat or negative performance, a time period which should have brought in about $6000 of net interest according to original estimates. If this were a stock market investment, it would all be part of normal fluctuations. But interest bearing loans aren’t supposed to do this.

- Therefore I have turned off automatic investments and will begin winding down this experiment – cashing out my money as the surviving loans are repaid. I have withdrawn $19000 in cash so far (although leaving it virtually in the table above to keep the month-to-month comparisons meaningful). This will tend to suppress the reported return rate, but the balance should still be rising if the loans were performing properly, which obviously they are not.

Older commentary:

Remember, the whole idea of Lending Club is making higher-risk loans in exchange for interest rates that are far higher than what you get in a guaranteed spot like a savings account. But along with high returns come some financially unstable borrowers, so it is inevitable that a certain percentage of loans will go bad. That’s all factored in to your expected rate of return.. but the million-dollar question is: Will the default rate end up being much higher than what Lending Club predicts?

I have seen many arguments on both side of this issue. In the early days, the more sophisticated ones (in my view) still seem to come down on the side of “projected returns are likely to be accurate”.

However, the company expanded aggressively to earn new borrowers over the years, and some of the marketing was targeted towards buying more shit rather than getting out of debt by refinancing old loans and halting your bad habit of buying shit. Also, I believe the flood of cheap investor capital led to lower interest rates and more lax standards.

In my opinion, this is a recipe for bad lending. Nobody should be borrowing money for consumption – buying a truck, boat, or a kitchen renovation.

The only things worth borrowing for are appreciating assets – a house in a reasonable market, and business and education in certain cases. Since Lending Club’s interest rates are not low enough to be used for mortgage or business lending, I had my account set to only fund debt consolidation loans.

But the good thing about this experiment, is that we get to find out for ourselves.

Here is my allocation across various note grades:

Most of my notes are the volatile but high return D and E grades – this is the key to the above average returns of this experiment.

Now about 4 years into the experiment, we’ve been seeing the expected stream of defaults and chargeoffs for quite a while. I’ve been looking into defaults individually to search for patterns. As a group, new loans seem to experience a wave of defaults, while people who have established a pattern of payment seem to continue paying. After about two years, the return seemed to have stabilized, but more recently they have started dropping again.

After accounting for all defaults so far, the annualized return of 10.18% is about 2% below the forecast.

The next test will be to see how this account survives a stock market crash and a recession (compared to the stock market as tracked in my Betterment experiment), whenever that happens next.

There is a very handy new Rate Adjuster feature on the LC dashboard: click it and it will automatically calculate a more conservative rate of return for you by writing off a portion of your late loans for you based on the percentage of those loans that on average are recovered, versus going bad. Clicking it with today’s results, I get 8.27% – a number which was stable above 10% for some time but has really started dropping in late 2016, so it might be the real answer for our long-term returns.

More conservatively, if you just look at more recent returns, my passively ignored account has grown from about $35,000 to $42,000 over the last two years – a compound annual growth rate of 9%.

After analyzing the early results, I noticed that my manual note selection was not particularly magical at increasing returns or decreasing defaults. So on January 30th, 2014, I switched the account over to their Automated Investing (formerly called ‘Prime’) service, which will handle reinvestments automatically for me. AI will obey your desired allocation across note grades, and you can now even combine it with one of your manual filters. This experiment has been going well, and the reduced amount of idle cash is providing higher returns and lower stress – no more manual fussing around with notes.

Since beginning this experiment, Lending Club itself has grown significantly in scale. This article in the Economist describes the flood of institutional money that is now pouring in to these notes, and the May 2013 Google Investment in Lending Club was a boost to its stability and credibility as well.

May 2016 Update: The company hit the news recently due to some improper handling of loans sold to a large investor. CEO Renaud Laplanche resigned over the issue and their stock price took a plunge. Some details in this NYT article. This has triggered an investigation by the US Department of Justice and SEC.

August 2016 Update: This Bloomberg article revealed some more questionable history in the company: back in 2009, the former CEO and other insiders took out some unneeded loans and rapidly repaid them to juice the company’s early results to impress investors. There were other allegations regarding individuals taking out multiple loans to cheat the risk ratings system, but I feel that this response by the new CEO Scott Sanborn addressed that properly, unless further information comes in.

So while the news certainly isn’t ideal, it sounds like the company is likely to recover in the long run. I’ve halted the reinvestments, but I don’t see a reason to cash out too hastily by selling the notes on the secondary market. If you’re not confident about investing yourself, you can just watch what happens to my investment instead, with no risk.

It will be interesting to see if my loan results keep going downward, or if they flatten out and recover again. Especially if the US economy happens to tip into a recession before they’re all paid off. Fun experiments with real money, in the name of curiosity and science :-).

Source: https://www.mrmoneymustache.com/the-lending-club-experiment loaded 22.03.2021

Boomers, Gen X, Gen Y, and Gen Z Explained

Updated by Kasasa January 13, 2021

What separates Generation Y from X? And hey Gen Z, welcome to the party! What’s the cutoff? How old is each generation? Are they really that different?

It’s easy to see why there is so much confusion about generational cohorts.

If you’ve ever felt muddled by this “alphabet soup” of names — you’re not alone. The real frustration hits when you realize that Millennial consumers represent the highest-spending generation in 2020 — with a projected $1.4 trillion tab.

And though their current wealth has been dragged down by not one but two “once-in-a-lifetime” economic crises during their most impactful career years, Millennials stand to inherit over $68 trillion from Baby Boomer parents by the year 2030, setting them up to potentially be the most wealthy generation in U.S. history.

Generation Z isn’t far behind, projected to hit $33 trillion in income by 2030 — that’s more than a quarter of all global income — and pass Millennials in spending power the year after. 3

No matter how you slice the data, the younger generations have never been more critical to your financial institution’s future.

Unless you understand who they are and what they want, you won’t capture a dollar of their money.

People grow older. Birthdays stay the same.

A common source of confusion when labeling generations is their age. Generational cohorts are defined (loosely) by birth year, not current age. The reason is simple — generations get older in groups. If you think of Millennials as college kids (18 – 22), then not only are you out of date — you’re thinking of a stage in life, not a generation. Millennials are now well out of college, and that life stage is dominated by Gen Z.

Another example, a member of Generation X who turned 18 in 1998 would now be over 40. In that time, he or she cares about vastly different issues and is receptive to a new set of marketing messages. Regardless of your age, you will always belong to the generation you were born into.

The breakdown by age looks like this:

- Baby Boomers: Baby boomers were born between 1946 and 1964. They’re currently between 57-75 years old (71.6 million in the U.S.)

- Gen X: Gen X was born between 1965 and 1979/80 and is currently between 41-56 years old (65.2 million people in the U.S.)

- Gen Y: Gen Y, or Millennials, were born between 1981 and 1994/6. They are currently between 25 and 40 years old (72.1 million in the U.S.)

- Gen Y.1 = 25-29 years old (around 31 million people in the U.S.)

- Gen Y.2 = 29-39 (around 42 million people in the U.S.)

- Gen Z: Gen Z is the newest generation, born between 1997 and 2012/15. They are currently between 6 and 24 years old (nearly 68 million in the U.S.)

The term “Millennial” has become the popular way to reference both segments of Gen Y (more on Y.1 and Y.2 below).

And as for “Zillennials,” those wedged at the tail end of Millennials and the start of Gen Z are sometimes labeled with this moniker — a group made up of people born between 1994 and the year 2000.

Realistically, the name Generation Z is a placeholder for the youngest people on the planet. It’s likely to morph as they leave adolescence and mature into their adult identities.

Why are generations named after letters?

It started with Generation X, people born between 1965-1980. The preceding generation was the Baby Boomers, born 1946-1964. Post World War II, Americans enjoyed new-found prosperity, which resulted in a “baby boom.” The children born as a result were dubbed the Baby Boomers.

But the generation that followed the Boomers didn’t have a blatant cultural identifier. In fact, that’s the anecdotal origin of the term Gen X — illustrating the undetermined characteristics they would come to be known by. Depending on whom you ask, it was either sociologists, a novelist, or Billy Idol who cemented this phrase in our vocabulary.

From there on it was all down-alphabet. The generation following Gen X naturally became Gen Y, born 1981-1996 (give or take a few years on either end). The term “Millennial” is widely credited to Neil Howe, along with William Strauss. The pair coined the term in 1989 when the impending turn of the millennium began to feature heavily in the cultural consciousness.

Generation Z refers to babies born from the late 90s through today. A flurry of potential labels has also appeared, including Gen Tech, post-Millennials, iGeneration, Gen Y-Fi, and Zoomers.

Splitting up Gen Y

Javelin Research noticed that not all Millennials are currently in the same stage of life. While all Millennials were born around the turn of the century, some of them are still in early adulthood, wrestling with new careers and settling down, while the older Millennials have a home and are building a family. You can imagine how having a child might change your interests and priorities, so for marketing purposes, it’s useful to split this generation into Gen Y.1 and Gen Y.2.

Not only are the two groups culturally different, but they’re in vastly different phases of their financial life. The younger group are just now flexing their buying power. The latter group has a more extensive history and may be refinancing their mortgage and raising children. The contrast in priorities and needs is stark.

The same logic can be applied to any generation that is in this stage of life or younger. As we get older, we tend to homogenize and face similar life issues. The younger we are, the more dramatic each stage of life is. Consider the difference between someone in elementary school and high school. While they might be the same generation, they have very different views and needs.

Marketing to young generations as a single cohort will not be nearly as effective as segmenting your strategy and messaging.

Why are generation cohort names important?

Each generation label serves as a short-hand to reference nearly 20 years of attitude, motivations, and historical events. Few individuals self-identify as Gen X, Millennial, or any other name.

They’re useful terms for marketers and tend to trickle down into common usage. Again, it’s important to emphasize that referring to a cohort only by the age range gets complicated quickly. Ten years from now, the priorities of Millennials will have changed — and marketing tactics must adjust instep. There are also other categories of cohorts you can use to better understand consumers going beyond age or generation..

Remember, these arbitrary generational cutoff points are just that. They aren’t an exact science, and are continually evolving.

Whatever terminology or grouping you use, the goal is to reach people with marketing messages relevant to their phase of life. In short, no matter how many letters get added to the alphabet soup, the most important thing you can do is seek to understand the soup du jour for the type of consumer you want to attract.

What makes each generation different?

Before we dive into each generation, remember that the exact years born are in dispute, because there are no comparably definitive thresholds by which the later generations (after Boomers) are defined. But this should give you a general range to help identify what generation you belong in.

The other fact to remember is that new technology is typically first adopted by the youngest generation and then is gradually adopted by the older generations. As an example, 96% of Americans have a smartphone, but Gen Z (the youngest generation) is the highest user.

The Baby Boomer Generation

- Boomer Birth Years: 1946 to 1964

- Current Age: 57 to 75

- Generation Size: 71.6 million

- Media Consumption: Baby boomers are the biggest consumers of traditional media like television, radio, magazines, and newspaper. Despite being so traditional, 90% of baby boomers have a Facebook account. This generation has begun to adopt more technology in order to stay in touch with family members and reconnect with old friends.

- Banking Habits: Boomers prefer to go into a branch to perform transactions. This generational cohort still prefers to use cash, especially for purchases under $5.

- Shaping Events: Post-WWII optimism, the cold war, and the hippie movement.

- What’s next on their financial horizon: This generation is experiencing the highest growth in student loan debt. While this might seem counterintuitive, it can be explained by the fact that this generation has the most wealth and is looking to help their children with their student debt. They have a belief that you should take care of your children enough to set them on the right course and don’t plan on leaving any inheritance. With more Americans outliving their retirement fund, declining pensions, and social security in jeopardy, ensuring you can successfully fund retirement is a major concern for Boomers.

Generation X

- Gen X Birth Years: 1965 to 1979/80

- Current Age: 41 to 56

- Other Nicknames: ”Latchkey” generation, MTV generation

- Generation Size: 65.2 million

- Media Consumption: Gen X still reads newspapers, magazines, listens to the radio, and watches TV (about 165 hours’ worth of TV a month). However, they are also digitally savvy and spend roughly 7 hours a week on Facebook (the highest of any generational cohort).

- Banking Habits: Since they are digitally savvy, Gen X will do some research and financial management online, but still prefer to do transactions in person. They believe banking is a person-to-person business and demonstrate brand loyalty.

- Shaping Events: End of the cold war, the rise of personal computing, and feeling lost between the two huge generations.

- What’s next on Gen X’s financial horizon: Gen X is trying to raise a family, pay off student debt, and take care of aging parents. These demands put a high strain on their resources. The average Gen Xer carries $142,000 in debt, though most of this is in their mortgage. They are looking to reduce their debt while building a stable saving plan for the future.

Millennials (Gen Y)

- Millennial Birth Years: 1981 to 1994/6

- Current Age: 25 to 40

- Other Nicknames: Gen Y, Gen Me, Gen We, Echo Boomers

- Generation Size: 72.1 million

- Media Consumption: 95% still watch TV, but Netflix edges out traditional cable as the preferred provider. Cord-cutting in favor of streaming services is the popular choice. This generation is extremely comfortable with mobile devices, but 32% will still use a computer for purchases. They typically have multiple social media accounts.

- Banking Habits: Millennials have less brand loyalty than previous generations. They prefer to shop product and features first, and have little patience for inefficient or poor service. Because of this, Millennials place their trust in brands with superior product history such as Apple and Google. They seek digital tools to help manage their debt and see their banks as transactional as opposed to relational.

- Shaping Events: The Great Recession, the technological explosion of the internet and social media, and 9/11

- What’s next on their financial horizon: Millennials are powering the workforce, but with huge amounts of student debt. This is delaying major purchases like weddings and homes. Because of this financial instability, Millennials choose access over ownership, which can be seen through their preference for on-demand services. They want partners that will help guide them to their big purchases.

Gen Z

- Gen Z Birth Years: 1997 to 2012/15

- Currently Aged: 6 to 24

- Other Nicknames: iGeneration, Post-millennials, Homeland Generation

- Generation Size: 68 million

- Media Consumption: The average Gen Zer received their first mobile phone at age 10.3 years. Many of them grew up playing with their parents’ mobile phones or tablets. They have grown up in a hyper-connected world and the smartphone is their preferred method of communication. On average, they spend 3 hours a day on their mobile device.

- Banking Habits: This generation has seen the struggle of Millennials and has adopted a more fiscally conservative approach. They want to avoid debt and appreciate accounts or services that aid in that endeavor. Debit cards top their priority list, followed by mobile banking.

- Shaping Events: Smartphones, social media, never knowing a country not at war, and seeing the financial struggles of their parents (Gen X).

- What’s next on Gen Z’s financial horizon: Learning about personal finance. They have a strong appetite for financial education and are opening savings accounts at younger ages than prior generations.

If you want to know more about Gen Z, check out this deep dive into their media consumption and banking habits.

Do generations use technology differently?

Younger generations have often led older Americans in their adoption and use of technology, and this largely holds true today.

Although Baby Boomers may trail Gen X and Millennials on native technology usage, the rate at which Boomers expand their use of technology is accelerated.

In fact, Boomers are far more likely to own a smartphone than they were in 2011 (68% in 2019 vs. 25% then).

Are generations the best way to categorize consumer behavior?

Knowing generational trends is important, as they can unveil similar attitudes and behaviors among consumers who experienced world events at the same life stage as their cohorts. And it doesn’t hurt to understand these age groups since marketing tools and audience segmentations generally include age as a factor.

But the generations don’t tell the whole story and their behaviors can be hard to lock down. After all, every generation grows up. So. can you rely on age ranges alone? Here’s what we think.

Do generations bank differently?

Absolutely, and for several reasons.

- Each generation has been in the workforce for different lengths of time and accumulated varying degrees of wealth.

- Baby Boomers have an average net worth of $1,066,000 and a median net worth of $224,000.

- Gen Xers average net worth is around $288,700, but the median is $59,800.

- Millennials have an average net worth around $76,200, but their median net worth is only $11,100.

- Gen Z’s average net worth is difficult to report on since so much of the generation has no net worth or career as of yet.

- Each generation is preparing and saving for different life stages; be that retirement, children’s college tuition, or buying a first car.

- Each generation grew up in evolving technological worlds and has unique preferences in regard to managing financial relationships.

- Each generation grew up in different financial climates, which has informed their financial attitudes and opinions of institutions. However, in the past year, the COVID-19 pandemic has become the great equalizer, as all generations have had to adapt to a new way of banking and living.

How are these banking differences appearing in the marketplace?

Ease of use vs. personal service.

If you think bots are taking over the world, you might be right. But for Millennial and Gen Z consumers, this isn’t necessarily a bad thing. In fact, according to a recent Adobe Analytics study, 44% of Gen Z and 31% of Millennials have used a banking chatbot to answer their questions. And before you think that must be a terrible user experience, over half of both groups who actually used a chatbot said the experience was better than talking to a real person.

However, for more complicated banking tasks, even the younger generations prefer the added assistance of a human representative.

Security still comes first, always. But each generation has their own priorities.

When choosing a new place to bank, “security” was the top-rated concern across Gen Z, Millennials, Gen X, and Boomers. “Reputation” (also known as your brand) finished second for both Gen Z and Millennial consumers.

However, for Gen Z and Boomer consumers, branch locations was the second most popular result, with “reputation” close behind. Younger consumers still care about branch locations, but weight it around the same level as an institution’s digital and app services.

For Generation X, digital and app services were edged out by in-person support. For Baby Boomers, banking local was more important.4 However, before you write off the importance of your online and mobile banking for these consumers…

Technology isn’t just for younger generations anymore.

The trend has long been for each new generation to adopt digital and mobile banking services more readily. But the COVID-19 pandemic has turned on a new wave of late-adopters who now bank digitally, too.

According to a recent Zelle survey, now 82% of seniors age 55+ are banking online more frequently — with 61% and 55% turning to social media and mobile banking more frequently too.5

That lines up closely with the start of the Baby Boomer demographic (currently ages 57 to 75). And while only time will tell how lasting this shift to digital tools and services will be, the more positive your digital experience, the more likely you are to extend your digital reach with this generation.

Today, older generations are behaving more like younger generations. And if you want to succeed in tomorrow’s market, you already need to meet these younger generations where they are. Now is the time to extend your brand of great service beyond the branch.

Tags: Research

Source: https://www.kasasa.com/articles/generations/gen-x-gen-y-gen-z loaded 23.03.2021

Why You Must Get Out of the System; The Fed’s Master Plan – Lynette Zang

The 9 Best Income Producing Assets to Grow Your Wealth

Posted September 15, 2020 by Nick Maggiulli

Want to get rich?

Then you should just keep buying a diverse set of income-producing assets.

While this advice sounds easy enough, the hard part comes when deciding what kind of income-producing assets to own.

Most investors rarely venture past stocks and bonds when creating an investment portfolio. And I don’t blame them. These two asset classes are quite popular and are great candidates for building wealth. However, stocks and bonds are just the tip of the investment iceberg. If you are really serious about growing your wealth, you should consider everything that the investing world has to offer.https://tpc.googlesyndication.com/safeframe/1-0-37/html/container.html

To this end, I have compiled a list of the 9 best income-producing assets that you can use to grow your wealth. Note that this list isn’t a recommendation, but a starting point for further research. Because I don’t know your current circumstances, I can’t say which, if any, of the following assets would be a good fit for you.

Personally, I only own 4 of the 9 asset classes listed below because some of them don’t make sense for me (at least at this point in time). I advise that you evaluate each asset class fully before adding/removing anything from your portfolio.

With that being said, let’s begin with the grandaddy of them all…

1. Stocks/Equities

If I had to pick one asset class to rule them all, stocks would definitely be it. Stocks, which represent the equity (i.e. ownership) in a business, are great because they are one of the most reliable ways to create wealth over the long run. Just read Triumph of the Optimists: 101 Years of Global Investment Returns or Stocks for the Long Run or Wealth, War, & Wisdom and you will get the same message—equities are an incredible investment.

And I don’t just mean equities in the U.S. either. As I have highlighted before, the record of history shows that stocks all over the world have been able to deliver consistent long-term returns:

{kind=link}

Of course, is it possible that the 20th century was a fluke and future equity returns are doomed? Yes, but I wouldn’t bet on it.https://tpc.googlesyndication.com/safeframe/1-0-37/html/container.html

More importantly, stocks are an amazing investment because they require no ongoing maintenance on your part. You own the business and reap the rewards while someone else (i.e. the management) runs the business for you.

So, how do you buy stocks? Well, you can purchase individual stocks (which I generally don’t recommend) or you can buy a fund that get you broader stock exposure. For example, an S&P 500 index fund will get you U.S. equity exposure while a “Total World Stock Index Fund” will get you worldwide equity exposure.

Of course, opinions differ on which kinds of stocks you should own. Some argue that you should focus on size (i.e. smaller stocks), some argue that you should focus on valuations (i.e. value stocks), and some argue that you should focus on price trends (i.e. momentum stocks). There are even others that suggest that owning stocks that pay frequent dividends is the surefire way to wealth. As a reminder, dividends are just profits from a business that are paid out to its shareholders (i.e. you). So if you own 5% of a business that pays out a total of $1M in dividends, you would receive $50,000. Pretty nice, huh?

Regardless of what stock strategy you choose, having some exposure to this asset class is the most important part. Personally, I own U.S. stocks, developed market stocks, and emerging market stocks from three different equity ETFs along with a handful of positions tilted toward smaller, value stocks. Is this the optimal way to invest in stocks? Probably not. But it works for me and should do well over the long run.https://88c512a0cd91ef779a6acc685dc95be9.safeframe.googlesyndication.com/safeframe/1-0-37/html/container.html

However, despite all the praise that I have just given to stocks, they are not for the faint of heart. As I once stated:

For equities, you should expect to see a 50%+ price decline a couple times a century, a 30% decline once every 4-5 years, and a 10% price decline at least every other year.

It is this highly volatile nature of stocks that makes them difficult to hold during turbulent times. Seeing a decade’s worth of growth disappear in a matter of days can be gut-wrenching even for the most seasoned investors. But what makes these declines especially troubling is when they are based on shifting sentiment rather than changes in underlying fundamentals.

The best way to combat such emotional volatility is to focus on the long-term. While this does not guarantee returns (i.e. see Japan), the evidence of history suggests that time is a stock investor’s friend, not foe.

Stocks/Equities Summary

- Average compounded annual return: 8%-10%

- Pros: High historic returns. Easy to own and trade. Low maintenance (i.e. someone else runs the business).

- Cons: High volatility. Valuations can change quickly based on sentiment rather than fundamentals.

2. Bonds

Now that we have discussed the high-flying world of stocks, let’s discuss the much calmer world of bonds.

Bonds are merely loans made from an investor to a borrower to be paid back over a certain period of time (i.e. the term/tenor/maturity). Many bonds require periodic payments (i.e. coupons) paid to the investor over the term of the loan before the full principal balance is paid back at end of the term.

The borrower can either be an individual, a business, or a government. Most of the time when investors discuss bonds they are referring to U.S. Treasury bonds, or bonds where the U.S. government is the borrower. U.S. Treasury bonds come in various maturities/terms and have different names based on the length of those terms:

- Treasury bills mature in 1-12 months

- Treasury notes mature in 2-10 years

- Treasury bonds mature in 10-30 years

You can find the interest rates paid on U.S. Treasury bonds for each of these terms online here.

In addition to U.S. Treasury bonds, you can also purchase foreign government bonds, corporate bonds (loans to businesses), and municipal bonds (loans to local/state governments). Though these kinds of bonds generally pay more interest than U.S. Treasury bonds, they also tend to be riskier.

Why are they riskier than U.S. Treasury bonds? Because the U.S. Treasury is the most creditworthy borrower on the planet. Since the U.S. government can just print any dollars they owe at will, anyone who lends to them is virtually guaranteed to get their money back. This is not necessarily true when it comes to foreign governments, local governments, or corporations.

This is why I tend to only invest in U.S. Treasury bonds. If I wanted to take more risk in my portfolio, I wouldn’t take it with my bonds. I understand that with current yields as low as they are (i.e. 10-year Treasuries are paying ~0.7% annually) there is a case to be made for owning higher yielding bonds, but I don’t think yield is the only thing that matters.

In fact, I recommend bonds as an income-producing asset because of the other properties that they exhibit. In particular, bonds:

1. Tend to rise when stocks (and other risky assets) fall.

2. Can provide “dry powder” when rebalancing your portfolio.

3. Have a more consistent income stream than other assets.

Unlike stocks and other risky assets, bonds have lower volatility which makes them more consistent and dependable even during the toughest of times. As I recently illustrated, those portfolios with more bonds (i.e. Treasuries) performed better during the 2020 coronavirus crash:

{kind=link}

More importantly, those that had bonds and were able to rebalance during the crash saw an even bigger benefit during the recovery that followed. Because of my Treasury bonds I was lucky enough to rebalance on the day of the recent market bottom. Yes, this timing was luck, but owning bonds in the first place was not.

So how can you buy bonds? You can choose to buy individual bonds directly, but I recommend buying them through bond funds because it’s much easier. If you think that owning individual bonds is somehow different from owning bonds in a fund, please read this and this to convince yourself otherwise.

Regardless of the kinds of bonds you consider buying, they can play an important role in your portfolio beyond providing growth. As the old saying goes:

We buy stocks so we can eat well, but we buy bonds so we can sleep well.

Bonds Summary

- Average compounded annual return: 2%-4% (likely lower in today’s low-rate environment)

- Pros: Lower volatility. Good for rebalancing. Safety in principal.

- Cons: Low returns, especially after inflation. Not great for income in a low-rate environment.

3. Investment/Vacation Properties

Outside of the realm of stocks and bonds, one of the next most popular income-producing assets is an investment/vacation property.

Owning an investment property can be great because not only does it provide you with a place to relax, but it can also earn you extra income. If you manage the property correctly, you will have other people (i.e. renters) helping you to pay off the mortgage while you enjoy the long-term price appreciation on the property. Additionally, if you were able to borrow money when acquiring the property, your return will be a bit higher due to the added leverage.

If this sounds too good to be true, it’s because it is. While there are many upsides to owning a vacation rental, it also requires far more work than many other assets that you can “set and forget.” Owning an investment/vacation property requires the ability to deal with people (i.e. renters), list the property, provide ongoing maintenance, and much more. While doing all of this, you also have to deal with the added stress of having another liability on your balance sheet.

When this goes right, owning an investment property can be wonderful, especially when you have borrowed most of the money to finance the purchase. However, when things go wrong, like they did in 2020, they can go really wrong. As many AirBnb entrepreneurs learned this year, vacation rentals aren’t always so easy.

While the returns on investment properties can be much higher than stocks/bonds, these returns also require far more work to earn them. If you are someone that wants to have more control over their investments and like the tangibility of real estate, then you should consider an investment/vacation property as a part of your portfolio.

Investment/Vacation Property Summary

- Average compounded annual return: 12%-15% (can be much higher/lower depending on specific circumstances)

- Pros: Bigger returns than other more traditional asset classes, especially when using leverage.

- Cons: Managing the property and tenants can be a headache. Less diversified.

4. Real Estate Investment Trusts (REITs)

If you like the idea of owning real estate, but hate the idea of managing it yourself, then the real estate investment trust (REIT) might be right for you. A REIT is a business that owns and manages real estate properties and pays out the income from those properties to its owners. In fact, REITs are legally required to pay out a minimum of 90% of their taxable income as dividends to their shareholders. This requirement makes REITs one of the most reliable income-producing assets on the market.

However, not all REITs are the same. There are residential REITs that can own apartment buildings, student housing, manufactured homes, and single-family homes, and commercial REITs that can own office buildings, warehouses, retail spaces, and other commercial properties. In addition, REITs can be offered as publicly-traded, private, or publicly non-traded:

- Publicly-traded REITs: Trade on a stock exchange like any other public company and available to all investors.

- Anyone who owns a broad stock index fund already has some exposure to publicly-traded REITs, so buying additional REITs is only necessary if you want to increase your exposure to real estate.

- Instead of buying many individual publicly-traded REITs, there are publicly-traded REIT index funds you can buy instead.

- Private REITs: Not traded on a stock exchange and only available to accredited investors (i.e. people with a net worth >$1M or annual income >$200,000 for the last 3 years).

- Requires a broker, which may result in high fees.

- Has less regulatory oversight.

- Less liquid due to longer required holding period.

- May generate higher returns than public market offerings.

- Publicly non-traded REITs: Not traded on a stock exchange, but available to all public investors.

- More regulatory oversight than private REITs.

- Minimum investment requirements.

- Less liquid due to longer required holding period.

- May generate higher returns than public market offerings.

Though I have only ever invested in publicly-traded REIT index funds, real estate crowdsourcing firms like Fundrise are a non-traded alternative that could offer higher long-term returns. If you want to dig deeper into the publicly-traded vs. non-traded REIT discussion, I recommend reading this article from Fundrise, Investopedia, and Millionacres, a Motley Fool service for more information.

No matter how you decide to invest in REITs, they generally have stock-like returns (or better) with a slightly lower correlation (0.5-0.7) during good times. Like most other risky assets, public-traded REITs tend to sell off during stock market crashes. Therefore, don’t expect many diversification benefits on the downside when owning them.

REITs Summary

- Average compounded annual return: 10%-12%

- Pros: Real estate exposure that you don’t have to manage.

- Cons: Higher volatility. Less liquidity for non-traded REITs. Highly correlated with stocks and other risk assets during stock market crashes.

5. Farmland

Outside of real estate, farmland is another great income-producing asset that has been a major source of wealth throughout history. Today, one of the best reasons to invest in farmland is its low correlation with stocks and bonds since farm income tends to be uncorrelated with what is happening in financial markets.

In addition, farmland has lower volatility than stocks while also providing inflation protection. Because of this asymmetric risk profile, farmland is also unlikely to “go to zero” unlike an individual stock/bond. Of course, the effects of climate change may alter this in the future.

What kind of returns can you expect from farmland? According to Jay Girotto on the Capital Allocators Podcast with Ted Seides, farmland is modeled to return in the “high single digits” with roughly half of the return coming from farm yields and half coming from land appreciation.

How do you invest in farmland? While buying individual farmland is no small undertaking, the most common way for investors to own farmland is through a publicly-traded REIT or a crowdsourced solution like FarmTogether or FarmFundr. The crowdsourced solution can be nice because you have more control over which farmland properties you specifically invest in.

The downside of crowdsourced solutions like FarmTogether and FarmFundr is that they are only available to accredited investors (i.e. people with a net worth >$1M or annual income >$200,000 for the last 3 years). In addition, the fees for these crowdsourced platforms can be a bit higher than with other public investments. For example, FarmTogether charges a 1% fee on all initial investments along with an ongoing 1% management fee, while FarmFundr structures deals to either own 15% of the equity or impose a 0.75%-1% management fee along with a 3% sponsor fee. I don’t think these fees are predatory given the amount of work that goes into structuring these deals, but if you hate the idea of fees, this is something to keep in mind.

Farmland Summary

- Average compounded annual return: 7%-9%

- Pros: Not as correlated with stocks. Good inflation hedge. Lower downside potential (land less likely to “go to zero” than other assets)

- Cons: Less liquidity (harder to buy/sell). Higher fees. Requires “accredited investor” status to participate.

6. Small Businesses/Franchise/Angel Investing

If farmland isn’t for you, maybe you should consider owning a small business or part of a small business. This is where angel investing and small business investing come in. However, before you embark on this journey you have to decide whether you will operate the business or just provide investment capital and expertise.

Owner + Operator

If you want to be an owner + operator of a small business/franchise, just remember that as much work as you think it will take, it will likely take more. As Brent Beshore, an expert on small business investing, once tweeted:

Here’s what it takes to run a Subway restaurant.

[links to 800 page operator’s manual]

Now imagine trying to run a $50M manufacturer.

I don’t mention Brent’s comments to discourage you from starting a small business, only to provide a realistic expectation for how much work they require. Owning and operating a small business can generate much higher returns than many of the other income-producing assets on this list, but you have to work for them.

Owner Only

Assuming you don’t want to go down the operator route, being an angel investor or passive owner of a small business can earn you very outsized returns. In fact, according to multiple studies (see here and here), the internal rate of return on angel investments is in the 20%-25% range.

However, these returns aren’t without a very large skew. An Angel Capital Association study found that just 1 in 9 angel investments (11%) yielded a positive return. This goes to show that though some small businesses may become the next Apple, most never make it far past the garage. As Sam Altman, famed investor and President of YCombinator, once wrote:

It’s common to make more money from your single best angel investment than all the rest put together. The consequence of this is that the real risk is missing out on that outstanding investment, and not failing to get your money back (or, as some people ask for, a guaranteed 2x) on all of your other companies.

This is why small business investing can be so tough, yet also so rewarding.

However, before you decide to go all-in, you should know that small business investing can be a huge time commitment. This is why Tucker Max gave up on angel investing and why he thinks most people shouldn’t even start. Max’s argument is quite clear—if you want access to the best angel investments (i.e. big, outsized returns) then you have to be deeply embedded in that community. Therefore, you can’t do angel/small business investing as a side thing and expect big results.

While firms like Microventures allow retail investors to invest in small businesses (with other opportunities for accredited investors), it is highly unlikely Microventures is going to have early access to the next big thing. I don’t say this to discourage you, but to reiterate that the most successful small business investors commit more than just capital to this pursuit.

So if you want to be a small business investor, keep in mind that a larger lifestyle change may be warranted in order to see significant results.

Small Business Summary

- Average compounded annual return: 20%-25%, but expect lots of losers.

- Pros: Can have extremely out-sized returns. The more involved you are, the more future opportunities you will see.

- Cons: Huge time commitment. Lots of failures can be discouraging.

7. Peer-to-Peer Lending

Like a bond, peer-to-peer lending is fixed-income investment where you lend money to individuals that (hopefully) pay you back over time. Given that individuals are, generally, less creditworthy than governments or businesses, the interest rates charged on these loans are typically much higher. However, higher interest rates don’t necessarily mean higher returns. As this graphic from LendingClub (an online peer-to-peer lending platform) illustrates, the interest rate charged for a loan is not predictive of its future return:

The reason for this is that those loans with higher rates are riskier, and, thus, more likely to default (i.e. not pay you back) than loans with lower rates. When you balance these higher interest rates against the expected increase in defaults from borrowers over the long run, you get the returns shown in the far right column. And note that these returns are across all the loans for a given loan grade. If you only lend to a few people, your results can vary drastically. This is why platforms like LendingClub make it easy to diversify by lending to hundreds of people at once.

The biggest downsides I see to peer-to-peer lending are the lower returns compared to other risk assets and the hidden risks that may exist within these assets. I only say hidden risks because we don’t have all that much historical data for peer-to-peer lending. This means that during unprecedented times, these loans may not perform as suggested.

For example, I looked through LendingClub’s recent August 2020 update and if the loss rate goes up more than expected, returns will fall well below their historical range. Fellow financial blogger Mr. Money Mustache experienced something similar after defaults lowered his long-term returns enough to make him pull his money from the platform. I don’t think this is the fault of LendingClub, but it is a possible risk you should consider before investing.

Peer-to-Peer Lending Summary

- Average compounded annual return: 4%-6% (based on Lending Club data)

- Pros: Easy to setup. Easy to diversify.

- Cons: Lower returns than many other risk assets. Less historical data for peer-to-peer lending, so possible hidden risks.

8. Royalties

If you aren’t a fan of lending, maybe you need to invest in something with a bit more…culture. This is where royalties come in. On sites like RoyaltyExchange you can buy and sell the royalties to music, film, and trademarks. Royalties can be a good investment because they generate steady income that is uncorrelated with financial markets.